Advertisement

- United States

- /

- Interactive Media and Services

- /

- NYSE:SNAP

Dive Into Fundamental Growth - Why Snap (NYSE:SNAP) is Losing Investor Confidence

Snap Inc. (NYSE:SNAP) had a large selloff right after management released new guidance and the last quarter's results. In this article we will look at the fundamentals underlying future growth and when the company is estimated to turn profitable for investors.

The Fundamentals of Growth

Snap's future guidance estimates an increase in revenue and about the same result in adjusted EBITDA. For Q3 the adjusted EBITDA is US$174m and the estimated number (upper bound) US$175m, which indicates that the company will remain at roughly the same level of profitability.

Snap is actually a high-growth company, which assumes that the company is in a phase of maximizing revenues, via their business model and reinvesting. The arguably better metrics to look at in Snap are the amount of funds being invested in the development of the business.

In the near term - next quarter, management estimates to grow revenue to US$1.2b, vs the US$1.1b in the last quarter. Additionally, analysts are still predicting a high growth for Snap, and estimate close to double the revenues at the end of 2023, with US$8.2b. This is the key metric for Snap, because cash flow maximization comes after a business matures.

In order to give Snap some credit and allow the business to mature, we can analyze how much and how well the company reinvests. Finally, we will indeed look at profitability and estimate when the company can reach a key milestone - when will the company breakeven.

See our latest analysis for Snap

Reinvestment & Growth

Unfortunately, even though the company grew revenues in the recent quarter, the growth has underlying low quality. The total World growth in average daily users has been from 293m to 306m, however the U.S. and European DAUs are quite stagnant, and most of the growth comes from the "rest of the world" which grew from 120m to 130m daily active users.

For a company to grow, it must reinvest. Growth can effectively be derived from the amount of money a company reinvests into the business and how smart it reinvests. This is called a fundamental growth rate, and it shows us the maximum % growth that can be sustained in the future according to those two factors.

So how much did Snap reinvest?

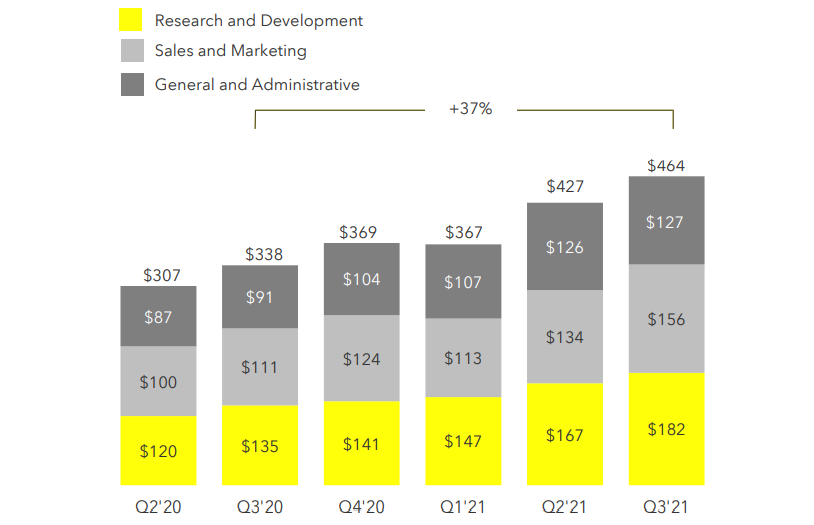

Capital investments are the things that result in long-term growth. The classical definition accounts for Net CapEx (investing more than the required replacement/depreciation expenses for assets) minus change in working capital. However, for technological companies, we would be unfair if we didn't include research & development, as that is one of the key assets for a software - or camera company, like Snap. Additionally, a company can grow via acquisitions, and the cash in acquisitions is also counted as a long-term investment.

The last earnings report shows us a great picture of how Snap allocated capital in investments:

One of the key assets of Snap is the value of their research assets, and while the company invested US$1.5b (GAAP) in R&D in the last 12 months, we can argue that the true value for the research asset of the tech company is accumulated across multiple years. If we go back in the last 3 years (using straight-line depreciation), we can capitalize the value of the research assets at US$1.9b, which gives us a better picture of the technology investments that Snap has.

Note, you will see a difference in the SEC filings and the slides for R&D expenses, this is because the slides use non-GAAP measurements which adjusts for different metrics such as stock based compensation, depreciation etc. However, as investors we should indeed count items that are used to motivate engineers to come up with better product, such as stock-based compensation.

Next are acquisitions. In 2020 and 2021 year to date, Snap invested close to US$1b in acquisitions. The value of every acquisition is hard to estimate, so we will take the investment at face value, and count the amount paid.

Finally, we add net CapEx and subtract change in working capital, leaving us with US$-150m.

If we had used the classic definition and just used Net CapEx as a measure of reinvestment, it would seem that the company is falling behind in reinvesting into growth.

However, by capitalizing R&D and adding the face value of Acquisitions, we get a sum of a US$2.8b value of long-term investments, which will feed the future growth of the company.

Looking at how much the company invested in the last 12 months, we come up with a value of US2b. Most of it being investments in R&D and some acquisitions.

The next part is to see how effectively is the company reinvesting. For that, we use something called the Sales to Capital ratio, which shows us how much revenue the company made for every $1 of invested capital. The Sales to capital ratio for Snap is around 0.7, which means that for every $1 invested, the company gains $0.7 in revenue.

Stemming from this, the next year's fundamental revenue growth rate for Snap is up to 45%, or about US$5.4b, which is fairly close to the US$5.7b expected from analysts at the beginning of 2023.

Unfortunately, management's guidance implies a lesser growth rate than what we computed, hence the reason we saw the recent selloff from investors.

Considering what we discussed here, there are two major implications moving forward.

- One, that management will be less effective at generating future revenues

- Second, that management has fewer avenues for growth, as evident by the stagnation of DAU's in Europe and the U.S.

Having all this in mind, we will now estimate when Snap can turn profitable and start generating free cash flows for investors.

Breakeven Estimates

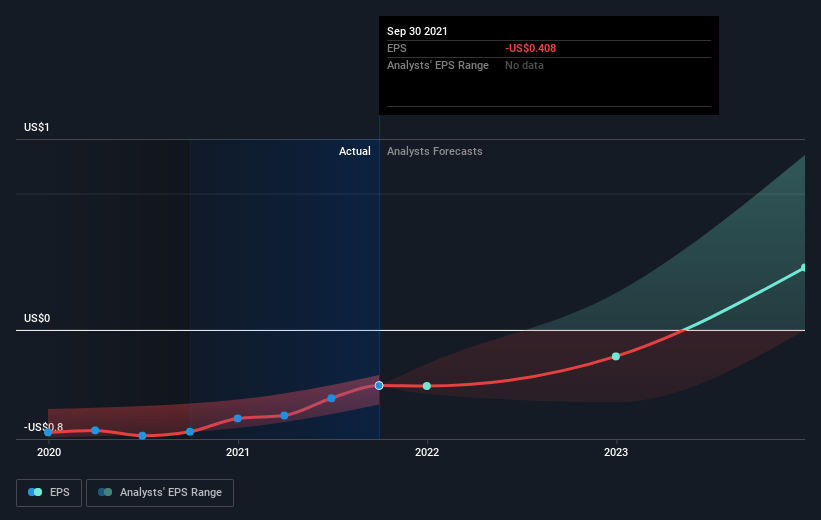

According to the 36 industry analysts covering Snap, the consensus is that breakeven is near. They expect the company to post a final loss in 2022, before turning a profit of US$764m in 2023.

Therefore, the company is expected to breakeven roughly 2 years from now.

Using a line of best fit, we calculated an average annual earnings growth rate of 73%, which signals high confidence from analysts.

Underlying developments driving Snap's growth isn’t the focus of this broad overview, though, take into account that by and large a high-growth rate is not out of the ordinary, particularly when a company is in a period of investment.

Before we wrap up, there’s one issue worth mentioning. Snap currently has a relatively high level of debt. Typically, debt shouldn’t exceed 40% of your equity, which in Snap's case is 65%. Note that a higher debt obligation increases the risk around investing in the loss-making company.

Conclusion & Next Steps:

Snap must go much further than just re-invest in order to post meaningful growth. The company must innovate and create value for their clients - which is arguably much harder than just increasing financing.

With the current re-investment rates and the limiting of possible growth avenues, Snap may experience a volatile period and investors might adjust their valuation of the company to a lower level.

We hope to see some more lasting features from Snap, rather than short-term hype features that lose engagement fairly quickly from clients.

This article is not intended to be a comprehensive analysis on Snap, so if you are interested in understanding the company at a deeper level, take a look at Snap's company page on Simply Wall St. We've also put together a list of pertinent factors you should look at:

- Actions instead of Words - Are insiders buying or selling their own stock.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Snap’s board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NYSE:SNAP

Snap

Operates as a technology company in North America, Europe, and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor