Advertisement

- United States

- /

- Media

- /

- NYSE:IPG

Why Interpublic Group (IPG) Is Up 6.2% After Q2 Earnings Drop Despite Share Buybacks and What's Next

Simply Wall St

Reviewed by Simply Wall St

- On July 22, 2025, Interpublic Group of Companies reported declines in sales, revenue, and net income for both the second quarter and first half of 2025 compared to the previous year, despite ongoing share buybacks totaling over US$98 million in the quarter.

- Notably, earnings per share from continuing operations were lower than the prior year for both time periods, suggesting operational challenges even as the company continued to return capital to shareholders through repurchases.

- We'll now assess how these recent earnings declines, despite share buybacks, may influence Interpublic Group's investment narrative and outlook.

Interpublic Group of Companies Investment Narrative Recap

Investors who see long-term value in Interpublic Group typically believe in the company's ability to transform through restructuring, adapt to industry changes, and benefit from technology-driven efficiencies, despite short-term hurdles. The recent declines in revenue and earnings reinforce near-term caution and serve as a reminder that macroeconomic factors and client spending remain the most important catalysts and also the biggest short-term risks; the latest results do not materially shift these focal points.

The most relevant recent announcement is the completion of share buybacks worth over US$98 million in the second quarter, which continued despite falling earnings. This signals ongoing capital returns even amid operational challenges, underscoring management's priority to support shareholder value through buybacks alongside its transformation program and restructuring efforts.

However, the ongoing pressure from weaker client budgets in a volatile economy could still limit how quickly performance can improve and, as investors should be aware, real recovery depends on ...

Read the full narrative on Interpublic Group of Companies (it's free!)

Interpublic Group of Companies is projected to reach $9.3 billion in revenue and $992.1 million in earnings by 2028. This forecast implies an annual revenue growth rate of 1.1% and a $498.4 million increase in earnings from the current level of $493.7 million.

Exploring Other Perspectives

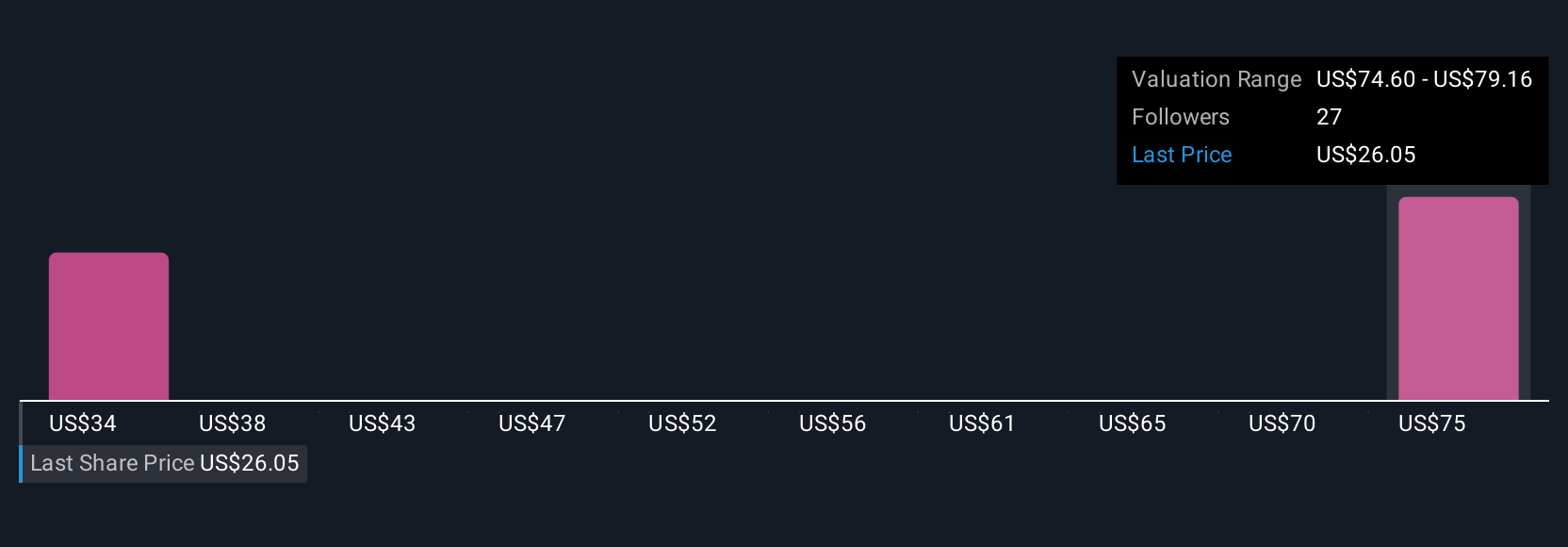

Simply Wall St Community members pegged Interpublic Group's fair value estimates between US$34.28 and US$71.67, with just two viewpoints included. While future earnings growth is a key catalyst, these differences highlight how opinions can vary widely, so consider exploring these alternative perspectives yourself.

Build Your Own Interpublic Group of Companies Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Interpublic Group of Companies research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Interpublic Group of Companies research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Interpublic Group of Companies' overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 19 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:IPG

Interpublic Group of Companies

Provides advertising and marketing services worldwide.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|59.7% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|13.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|2.9% undervalued

RO

Community Contributor