- United States

- /

- Entertainment

- /

- NYSE:DIS

Disney’s (NYSE:DIS) Downside Appears Limited - but Sentiment may Remain Subdued until a Positive Catalyst Develops

Last week The Walt Disney Company ( NYSE:DIS ) released fourth quarter results which disappointed the market. The stock price has been under pressure since March, and has now broken below the $167 level that had previously acted as support. The stocks appear reasonably valued, but sentiment may take time to improve.

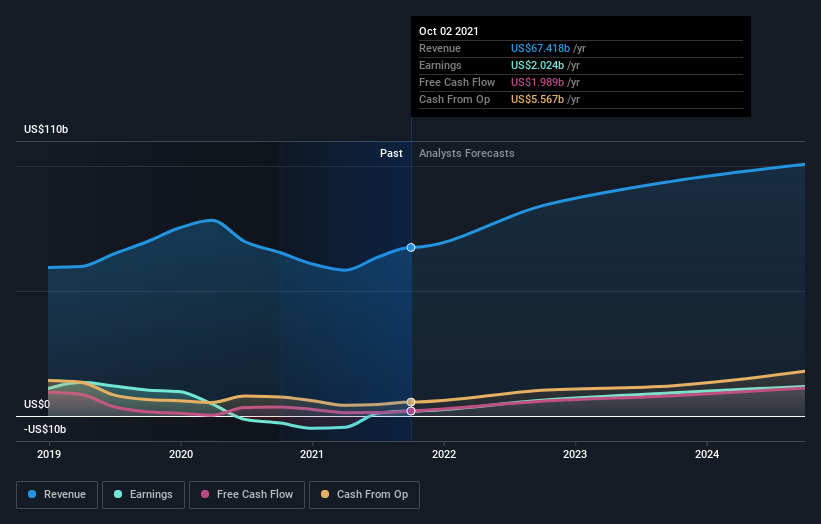

Fourth quarter highlights:

- Quarterly revenue up 26% YoY to $18.53 billion, $240 below consensus estimates

- non-GAAP EPS $0.37 compared to -$0.20, $0.13 below consensus estimates.

- Free cash flow up 62% YoY to $1,522.

- Disney Media and Entertainment Distribution revenue up 9% YoY.

- Disney Parks, Experiences and Products revenue up 99% YoY, and back to profitability.

- Disney + subscribers up 60% YoY.

- Disney + monthly revenue per paid subscriber down 9% YoY.

For the full year:

- Revenue was up 3.1% to $67.4.

- Net Income up $4.86 billion to $2.02 billion.

- Profit margin at 3%.

Overall, Disney’s recovery is on track, but the market appears focussed on the lower than expected and slowing subscriber growth at Disney+. Disney’s management also indicated that the net loss at Disney+ is expected to widen in the coming quarters as the company invests in new content.

View our latest analysis for Walt Disney

What is Walt Disney worth?

According to our estimate of the valuation, the intrinsic value for the stock is $264.01, but it is currently trading 40% below this level at US$160. But, there may be another chance to buy again in the future. This is because Walt Disney’s beta (a measure of share price volatility) is high, meaning its price movements will be exaggerated relative to the rest of the market. If the market is bearish, the company's shares will likely fall by more than the rest of the market, providing a prime buying opportunity.

What kind of growth will Walt Disney generate?

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Although value investors would argue that it’s the intrinsic value relative to the price that matters the most, a more compelling investment thesis would be high growth potential at a cheap price. Walt Disney's earnings over the next few years are expected to double, indicating a very optimistic future ahead. This should lead to stronger cash flows, feeding into a higher share value.

What this means for you:

The addition of new content in 2022 should help the company increase subscriber numbers. In addition, the net loss is expected to peak in 2022. This suggests there should be an inflection point in sentiment in the next year. There is also potential for margin improvements in the rest of the business - the net income margin is now 3% vs a 5 year average of 11.4%.

With the share price below technical support there may be some more downside until a positive catalyst develops. However, the current discount to fair value implies that downside may be limited. $153 is a key level to keep an eye on as it would close the gap formed in December last year and also coincides with a previous high.

We have only touched on a few aspects of Disney’s outlook here. To get a better understanding of the company as well as other risks we have identified take a look at our latest analysis for Walt Disney

If you are no longer interested in Walt Disney, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

If you're looking to trade Walt Disney, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Walt Disney might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.

About NYSE:DIS

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives