Advertisement

- United States

- /

- Entertainment

- /

- NasdaqGS:TTWO

Take-Two Interactive Software (NASDAQ:TTWO) Is Making Moderate Use Of Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Take-Two Interactive Software, Inc. (NASDAQ:TTWO) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Take-Two Interactive Software

What Is Take-Two Interactive Software's Net Debt?

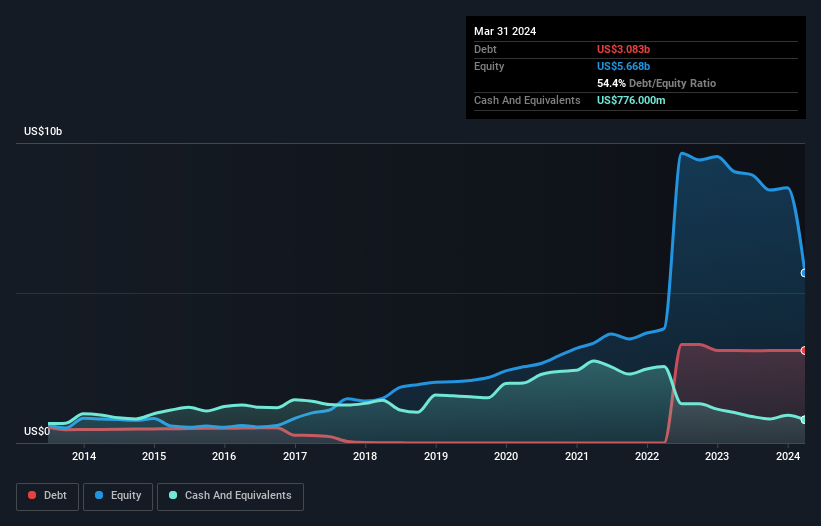

The chart below, which you can click on for greater detail, shows that Take-Two Interactive Software had US$3.08b in debt in March 2024; about the same as the year before. However, because it has a cash reserve of US$776.0m, its net debt is less, at about US$2.31b.

How Healthy Is Take-Two Interactive Software's Balance Sheet?

According to the last reported balance sheet, Take-Two Interactive Software had liabilities of US$2.41b due within 12 months, and liabilities of US$4.14b due beyond 12 months. Offsetting this, it had US$776.0m in cash and US$963.2m in receivables that were due within 12 months. So its liabilities total US$4.81b more than the combination of its cash and short-term receivables.

Since publicly traded Take-Two Interactive Software shares are worth a very impressive total of US$27.5b, it seems unlikely that this level of liabilities would be a major threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Take-Two Interactive Software's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Take-Two Interactive Software saw its revenue hold pretty steady, and it did not report positive earnings before interest and tax. While that hardly impresses, its not too bad either.

Caveat Emptor

Importantly, Take-Two Interactive Software had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost US$470m at the EBIT level. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. Quite frankly we think the balance sheet is far from match-fit, although it could be improved with time. However, it doesn't help that it burned through US$158m of cash over the last year. So to be blunt we think it is risky. For riskier companies like Take-Two Interactive Software I always like to keep an eye on whether insiders are buying or selling. So click here if you want to find out for yourself.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Take-Two Interactive Software might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:TTWO

Take-Two Interactive Software

Develops, publishes, and markets interactive entertainment solutions for consumers worldwide.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.0% undervalued

286 followersusers have followed this narrative

1 commentusers have commented on this narrative

42 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

95 followersusers have followed this narrative

2 commentsusers have commented on this narrative

27 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4524.2% undervalued

8 followersusers have followed this narrative

3 commentsusers have commented on this narrative

3 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2803.2% undervalued

62 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

TR

TravelGuy on Pagaya Technologies ·

PGY may go up in next 6-12 months.

Fair Value:US$11.9829.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SA

SakuraCoffee on S&P Global ·

Guidance Cuts and AI Concerns Shake S&P Global

Fair Value:US$38012.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Esteban on Verisk Analytics ·

VRSK 05-2026

Fair Value:US$69.7150.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

95 followersusers have followed this narrative

2 commentsusers have commented on this narrative

27 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.230.7% undervalued

68 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9325.1% undervalued

1399 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative