Advertisement

- United States

- /

- Media

- /

- NasdaqGS:SATS

Analysts Have Been Trimming Their EchoStar Corporation (NASDAQ:SATS) Price Target After Its Latest Report

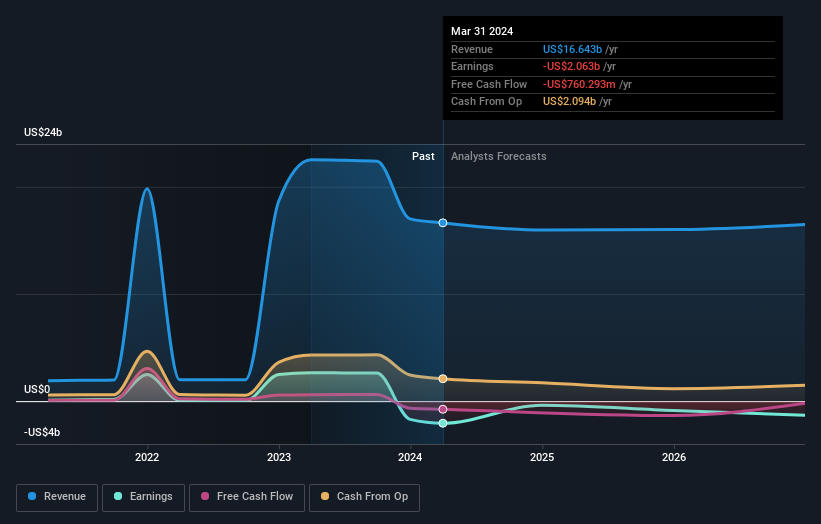

It's been a mediocre week for EchoStar Corporation (NASDAQ:SATS) shareholders, with the stock dropping 12% to US$15.31 in the week since its latest quarterly results. It was a pretty bad result overall; while revenues were in line with expectations at US$4.0b, statutory losses exploded to US$0.40 per share. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

View our latest analysis for EchoStar

Taking into account the latest results, the current consensus, from the eight analysts covering EchoStar, is for revenues of US$16.0b in 2024. This implies a perceptible 4.1% reduction in EchoStar's revenue over the past 12 months. The loss per share is expected to greatly reduce in the near future, narrowing 85% to US$1.17. Yet prior to the latest earnings, the analysts had been forecasting revenues of US$16.2b and losses of US$1.61 per share in 2024. Although the revenue estimates have not really changed EchoStar'sfuture looks a little different to the past, with a considerable decrease in the loss per share forecasts in particular.

The consensus price target fell 6.9% to US$20.13despite the forecast for smaller losses next year. It looks like the ongoing lack of profitability is starting to weigh on valuations. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values EchoStar at US$38.00 per share, while the most bearish prices it at US$12.00. As you can see the range of estimates is wide, with the lowest valuation coming in at less than half the most bullish estimate, suggesting there are some strongly diverging views on how analysts think this business will perform. As a result it might not be a great idea to make decisions based on the consensus price target, which is after all just an average of this wide range of estimates.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that revenue is expected to reverse, with a forecast 5.4% annualised decline to the end of 2024. That is a notable change from historical growth of 54% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 3.3% per year. It's pretty clear that EchoStar's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most obvious conclusion is that the analysts made no changes to their forecasts for a loss next year. On the plus side, there were no major changes to revenue estimates; although forecasts imply they will perform worse than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of EchoStar's future valuation.

With that in mind, we wouldn't be too quick to come to a conclusion on EchoStar. Long-term earnings power is much more important than next year's profits. At Simply Wall St, we have a full range of analyst estimates for EchoStar going out to 2026, and you can see them free on our platform here..

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with EchoStar , and understanding these should be part of your investment process.

Valuation is complex, but we're here to simplify it.

Discover if EchoStar might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:SATS

EchoStar

Provides networking technologies and services in the United States and internationally.

Fair value with worrying balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.8% undervalued

RO

Community Contributor