Criteo (CRTO) just made headlines with a strategic step that could change its role in the digital ad world. The company has been named Google's first onsite retail media partner, launching a new integration with Google Search Ads 360. For investors, this collaboration is a significant moment, connecting Criteo's broad retail network to Google's advertising platform and opening fresh revenue channels across the Americas, with more global expansion promised.

Over the past year, though, Criteo shareholders have weathered some headwinds, with shares down nearly 48% and momentum lagging the broader market. Even as this news drives conversation and sets Criteo up for greater relevance in a fast-growing $204B industry, the stock’s overall performance still reflects concern about declining annual revenue and muted profit growth. Despite optimism about new market opportunities, the company’s long-term track record remains mixed.

So after a challenging year for the stock and a milestone move with Google, the real question is whether investors have caught the opportunity early or if the market is already pricing in all of Criteo’s future growth.

Advertisement

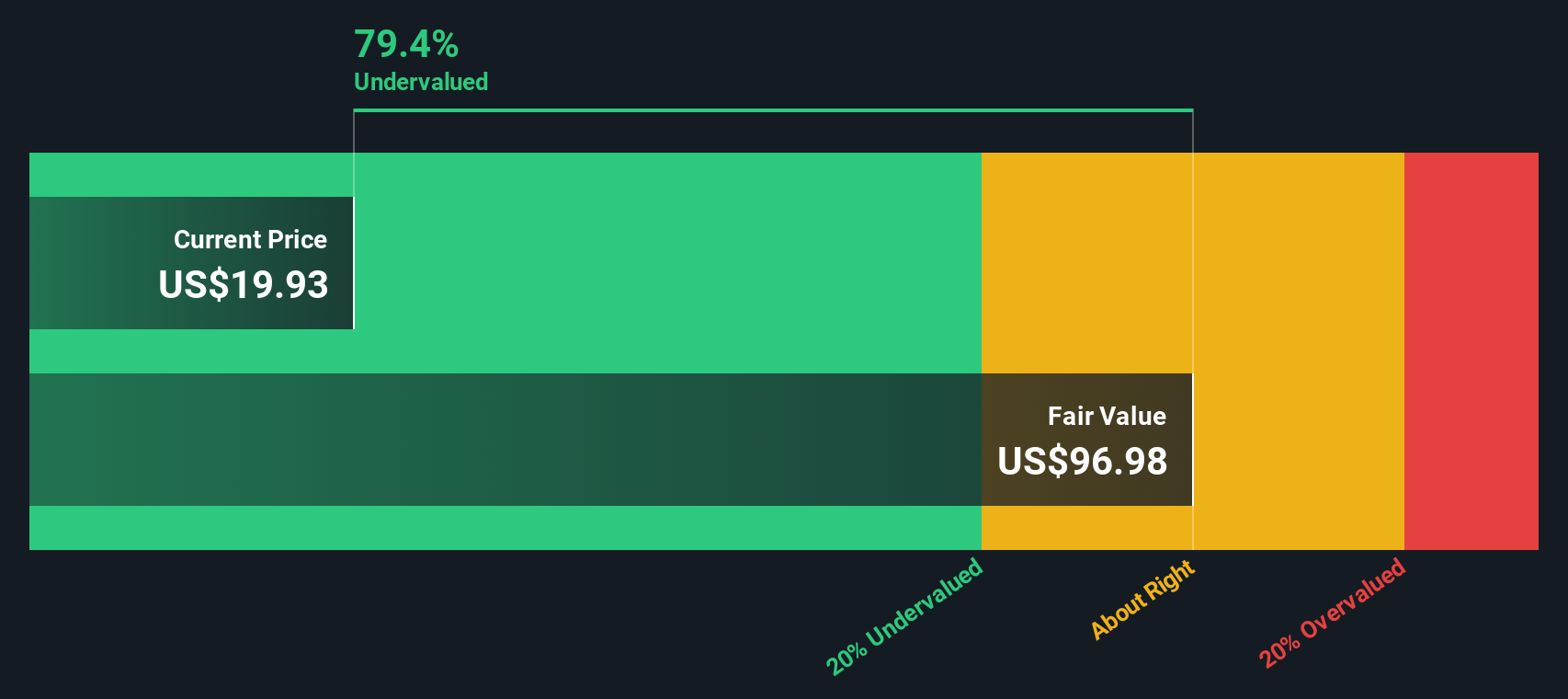

Most Popular Narrative: 42% Undervalued

According to the most widely followed narrative, Criteo is seen as significantly undervalued. This view is based on future earnings growth, margin expansion, and assumed improvements in the company's strategic positioning in digital advertising.

The rapid adoption of AI-powered ad targeting and the development of Agentic AI solutions leveraging Criteo's structured commerce data are expected to boost campaign performance and unlock new monetization channels. This supports both revenue growth and potential margin expansion as productized, automated offerings gain scale.

Curious how a traditional ad-tech player could be priced so far below its potential? There is a surprising catalyst hidden in the key financial assumptions behind this narrative’s fair value, one that could transform Criteo’s earnings trajectory and valuation multiple. Want to see exactly which growth drivers and forecasts justify such a bold upside call? Dive deeper to discover the precise numbers that power this dramatic value gap.

However, uncertainties around AI monetization and intense competition from larger digital platforms could undermine the bullish case for Criteo’s future valuation.

While analysts’ price targets highlight future earnings potential, our SWS DCF model takes a different approach by estimating fair value based on projected cash flows. This method also suggests the stock may be undervalued. Could both views be correct, or is there still an element missing from the story?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Criteo for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Criteo Narrative

If you see things differently, or you want to dive deeper into Criteo’s numbers yourself, you can quickly shape your own narrative and view the data your way by using Do it your way.

Don't let the best stocks slip by while you wait. Let Simply Wall Street's powerful filters help you pinpoint the next standout opportunity in seconds. When it comes to investing, timing and insights are everything.

Capture tomorrow’s most disruptive returns by targeting companies leading breakthroughs in artificial intelligence with our handpicked AI penny stocks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

A technology company, provides marketing and monetization services and infrastructure on the open internet in North and South America, Europe, the Middle East, Africa, and the Asia-Pacific.