Advertisement

- United States

- /

- Interactive Media and Services

- /

- NasdaqGM:BLCT

The Consensus EPS Estimates For BlueCity Holdings Limited (NASDAQ:BLCT) Just Fell A Lot

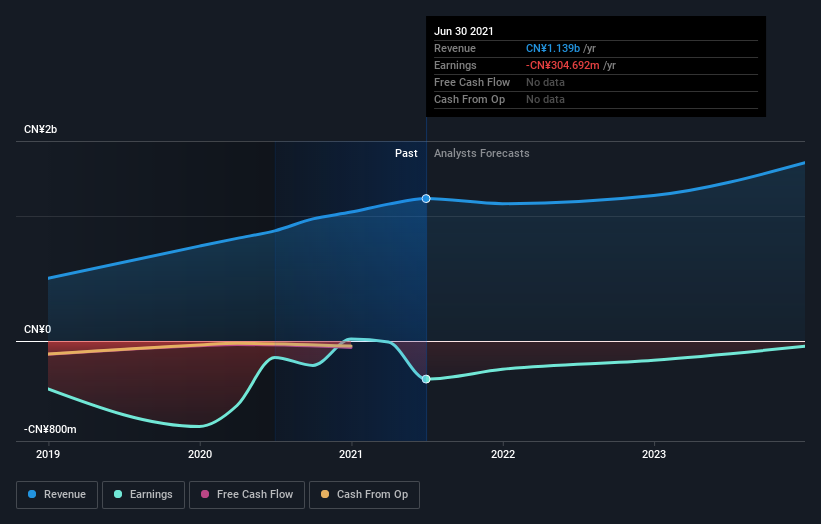

Today is shaping up negative for BlueCity Holdings Limited (NASDAQ:BLCT) shareholders, with the covering analyst delivering a substantial negative revision to next year's forecasts. Revenue and earnings per share (EPS) forecasts were both revised downwards, with the analyst seeing grey clouds on the horizon.

Following the downgrade, the current consensus from BlueCity Holdings' sole analyst is for revenues of CN¥1.2b in 2022 which - if met - would reflect a modest 2.1% increase on its sales over the past 12 months. Losses are predicted to fall substantially, shrinking 48% to CN¥4.32. Yet prior to the latest estimates, the analyst had been forecasting revenues of CN¥1.4b and losses of CN¥1.12 per share in 2022. So there's been quite a change-up of views after the recent consensus updates, with the analyst making a serious cut to their revenue forecasts while also expecting losses per share to increase.

View our latest analysis for BlueCity Holdings

The consensus price target fell 61% to CN¥12.78, with the analyst clearly concerned about the company following the weaker revenue and earnings outlook.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that BlueCity Holdings' revenue growth will slow down substantially, with revenues to the end of 2022 expected to display 1.7% growth on an annualised basis. This is compared to a historical growth rate of 29% over the past year. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 15% annually. Factoring in the forecast slowdown in growth, it seems obvious that BlueCity Holdings is also expected to grow slower than other industry participants.

The Bottom Line

The most important thing to take away is that the analyst increased their loss per share estimates for next year. Unfortunately the analyst also downgraded their revenue estimates, and industry data suggests that BlueCity Holdings' revenues are expected to grow slower than the wider market. After such a stark change in sentiment from the analyst, we'd understand if readers now felt a bit wary of BlueCity Holdings.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for BlueCity Holdings going out as far as 2023, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if BlueCity Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:BLCT

BlueCity Holdings

BlueCity Holdings Limited operates a platform for LGBTQ community primarily under BlueCity brand in the People’s Republic of China, India, South Korea, Thailand, and Vietnam.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor