- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:BIDU

Baidu (NASDAQ:BIDU) Offers Upside Potential at a Reasonable Valuation

Baidu, Inc. ( NASDAQ:BIDU ) released a mixed set of third quarter results on Wednesday. While the results were better than expected, net income was sharply lower than a year ago as a result of non-cash earnings in prior periods. The positive takeaway was very strong growth in the AI and cloud segment. Baidu’s share price is still 51% below its February high due to the regulatory pressure facing many Chinese tech companies.

Highlights from Baidu’s third quarter results:

- Non-GAAP EPS RMB14.66, down 28% YoY but RMB1.71 ahead of consensus estimate .

- GAAP loss per share of RMB48.18.

- Revenue RMB31.92 bln up 13% YoY and marginally ahead of consensus estimate.

- Fourth quarter revenue guidance raised to between RMB 31.0 bln and RMB 34.0 bln.

- Baidu Core online marketing revenue up 6% YoY.

- Baidu Core non-online marketing revenue (including cloud and AI) up 76% YoY.

- iQIYI revenue up 6% YoY.

View our latest analysis for Baidu

Is Baidu still cheap?

When we estimated Baidu’s value based on expected future cash flows we came to a value of $357 per share , implying the stock is trading at 52% discount. The price-to-earnings (PE) ratio of 8.7x is a lot lower than comparable US companies which trade on an average P/E ratio of 29.5x, and the broad markets ratio of 18x.

The apparent discount is similar for most Chinese tech stocks and reflects the extra risk now associated with these shares.

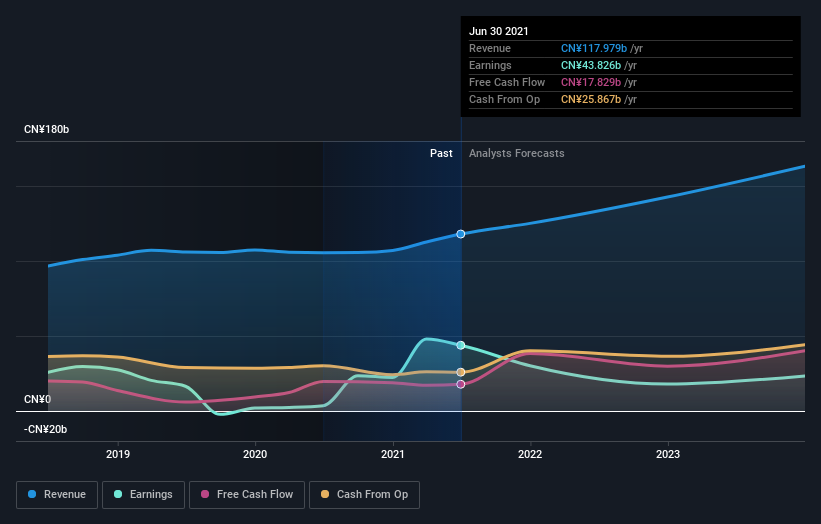

Can we expect growth from Baidu?

This chart reflects the fact that Baidu’s earnings were boosted by non-cash earnings earlier in the year. So while earnings are expected to decline until the end of next year, cash flows are expected to rise.

Most of Baidu’s revenue comes from advertising related to the search products. This revenue is relatively stable and growing slowly. Baidu is facing increased competition in this space, so growth for this segment is likely to remain subdued.

The potential growth engine is the cloud and AI business, which seems to be gaining momentum. This part of the business now accounts for 14% of total revenue which doesn’t move the needle very much. But if the momentum continues it will begin to make a difference in a year or two. Baidu’s autonomous driving technology is another business that offers future optionality.

The bottom line on Baidu

Baidu’s current growth prospects don’t look very exciting, and the remaining regulatory risks are difficult to quantify. But there are several positives to consider:

- Stable cash flows

- Priced at substantial discount to expected cash flows.

- A strong balance sheet.

- Optionality on future growth from cloud, AI and autonomous driving tech.

Earnings growth is expected to remain subdued over the next 12 months - so it may take another catalyst for interest in the stock to pick up again -possibly renewed interest in China’s tech sector.

If you would like to know more about Baidu, have a look at our latest company analysis which also lists other opportunities and risks you will want to be aware of.

If you are no longer interested in Baidu, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

Valuation is complex, but we're here to simplify it.

Discover if Baidu might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.

About NasdaqGS:BIDU

Baidu

Provides online marketing and non-marketing value added services through an internet platform in the People’s Republic of China.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Community Narratives