- United States

- /

- Chemicals

- /

- NYSE:SXT

Are Sensient Technologies Corporation's (NYSE:SXT) Fundamentals Good Enough to Warrant Buying Given The Stock's Recent Weakness?

Sensient Technologies (NYSE:SXT) has had a rough month with its share price down 9.4%. But if you pay close attention, you might find that its key financial indicators look quite decent, which could mean that the stock could potentially rise in the long-term given how markets usually reward more resilient long-term fundamentals. Particularly, we will be paying attention to Sensient Technologies' ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

How To Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Sensient Technologies is:

12% = US$135m ÷ US$1.2b (Based on the trailing twelve months to June 2025).

The 'return' is the profit over the last twelve months. That means that for every $1 worth of shareholders' equity, the company generated $0.12 in profit.

Check out our latest analysis for Sensient Technologies

Why Is ROE Important For Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

Sensient Technologies' Earnings Growth And 12% ROE

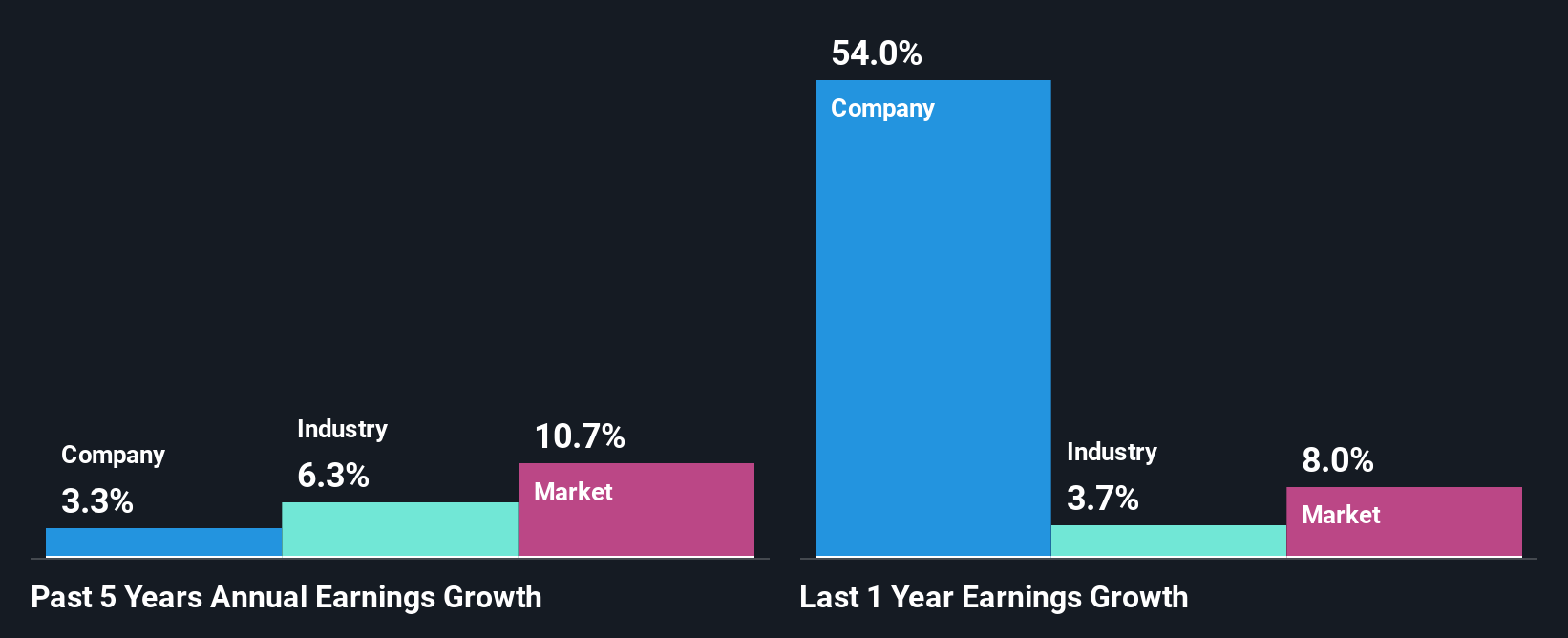

To start with, Sensient Technologies' ROE looks acceptable. Further, the company's ROE compares quite favorably to the industry average of 9.3%. Despite this, Sensient Technologies' five year net income growth was quite low averaging at only 3.3%. That's a bit unexpected from a company which has such a high rate of return. A few likely reasons why this could happen is that the company could have a high payout ratio or the business has allocated capital poorly, for instance.

Next, on comparing with the industry net income growth, we found that Sensient Technologies' reported growth was lower than the industry growth of 6.3% over the last few years, which is not something we like to see.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. If you're wondering about Sensient Technologies''s valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Sensient Technologies Making Efficient Use Of Its Profits?

The high three-year median payout ratio of 54% (that is, the company retains only 46% of its income) over the past three years for Sensient Technologies suggests that the company's earnings growth was lower as a result of paying out a majority of its earnings.

Additionally, Sensient Technologies has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Upon studying the latest analysts' consensus data, we found that the company is expected to keep paying out approximately 43% of its profits over the next three years. Regardless, the future ROE for Sensient Technologies is predicted to rise to 14% despite there being not much change expected in its payout ratio.

Summary

On the whole, we do feel that Sensient Technologies has some positive attributes. Yet, the low earnings growth is a bit concerning, especially given that the company has a high rate of return. Investors could have benefitted from the high ROE, had the company been reinvesting more of its earnings. As discussed earlier, the company is retaining a small portion of its profits. Having said that, looking at the current analyst estimates, we found that the company's earnings are expected to gain momentum. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:SXT

Sensient Technologies

Manufactures and markets colors, flavors, and other specialty ingredients worldwide.

Solid track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)