Advertisement

- United States

- /

- Chemicals

- /

- NYSE:OLN

Olin (OLN) Valuation in Focus After Citigroup Downgrade on Demand and Debt Concerns

Simply Wall St

Reviewed by Kshitija Bhandaru

Citigroup’s recent downgrade of Olin (OLN) to Neutral has put the spotlight on the company’s outlook. The move was driven by questions about demand in chlorine derivatives and persistent struggles in epoxy.

See our latest analysis for Olin.

Olin’s share price has drifted sideways for much of the year, with a modest pickup in recent weeks not enough to reverse a one-year total shareholder return of -0.45%. The Citigroup downgrade and ongoing sector headwinds appear to be weighing on momentum, leaving investors looking for fresh signs of stability before sentiment turns more positive.

If news like this has you rethinking your watchlist, now is a great moment to discover fast growing stocks with high insider ownership

With Olin shares trading below recent price targets and valuation metrics offering mixed signals, the question for investors is clear: Is the market underestimating a rebound, or is it already factoring in all the potential for future growth?

Most Popular Narrative: 7.3% Overvalued

Analyst consensus pins Olin's fair value at $23.47, which is below the current share price of $25.19. This sets the stage for a debate on whether upside is capped or a turnaround is brewing.

Structural cost reduction initiatives (Beyond250 and Epoxy cost optimization) are expected to deliver significant operational savings, yielding an estimated $70 to $90 million run-rate benefit by the end of 2025 and additional structural cost reductions from the Stade, Germany facility in 2026. This should improve net margins and boost earnings quality.

What’s fueling this controversial price? Analysts are betting on an earnings transformation, with operational shakeups and margin leaps driving their headline projections. Uncover which bold moves and financial shifts anchor this eye-catching valuation.

Result: Fair Value of $23.47 (OVERVALUE D)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing global oversupply and fierce competition from low-cost producers could undermine Olin’s turnaround potential. This could put pressure on revenue and profit margins.

Find out about the key risks to this Olin narrative.

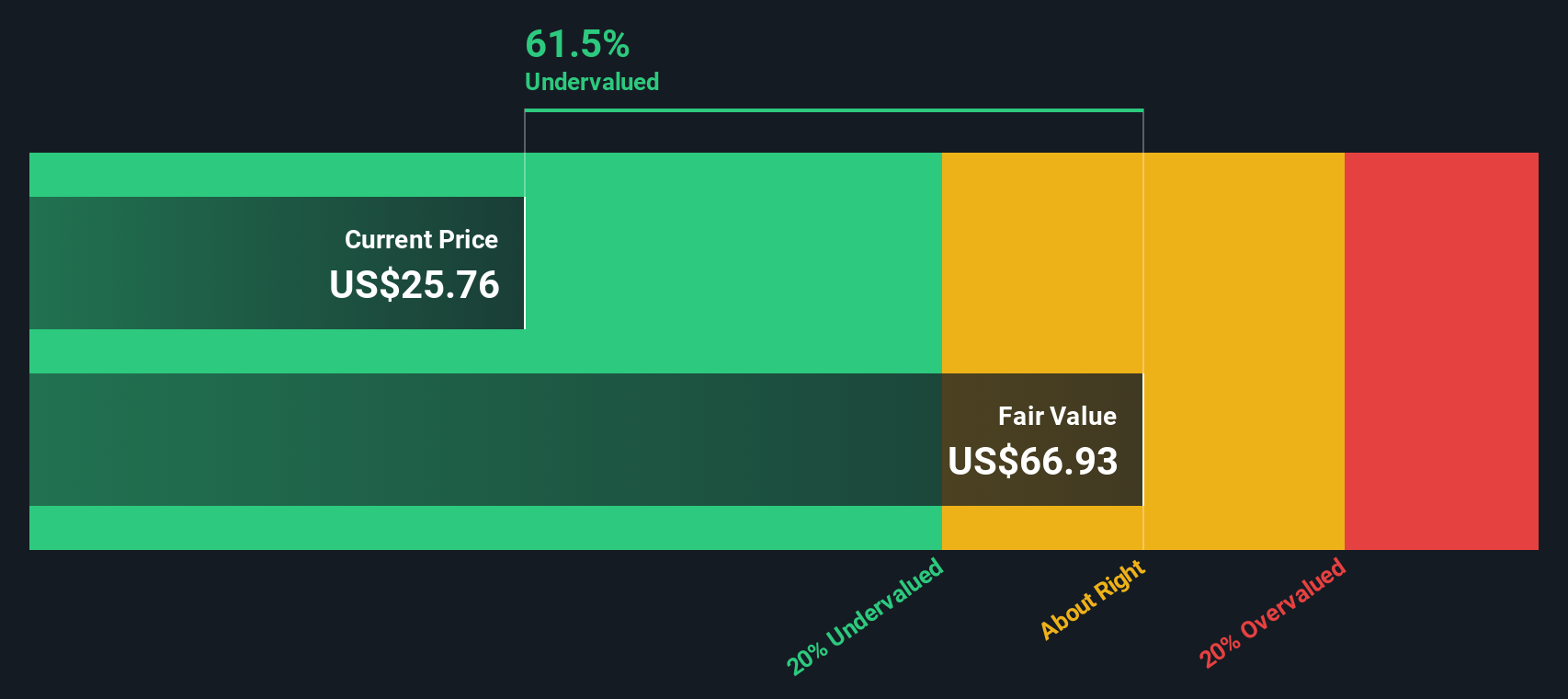

Another View: The DCF Model Shows Major Upside

While the analyst consensus sees Olin as slightly overvalued, our SWS DCF model takes a very different view. According to DCF analysis, Olin’s fair value is $66.94, which is significantly higher than its recent share price. This represents a substantial discount for a stock that many consider troubled. Is the market being overly pessimistic?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Olin Narrative

If you have your own perspective or want to dive deeper into the numbers, the tools are at your fingertips to craft a personal view in minutes. Do it your way

A great starting point for your Olin research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t just wait on the sidelines while others seize hidden opportunities. Use the Simply Wall Street Screener and get ahead on tomorrow’s winners, today.

- Unlock high-potential returns with these 909 undervalued stocks based on cash flows backed by strong cash flows, ideal for value-focused investors seeking overlooked gems.

- Tap into exponential advancement by checking out these 24 AI penny stocks, where leading-edge artificial intelligence companies are pushing boundaries in automation and data science.

- Power up your portfolio with these 19 dividend stocks with yields > 3% if you value reliable income streams and yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:OLN

Olin

Manufactures and distributes chemical products in the United States, Europe, Asia Pacific, Latin America, and Canada.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor