Advertisement

- United States

- /

- Metals and Mining

- /

- NYSE:NEM

How Investors May Respond To Newmont (NEM) Beating Q2 Estimates Amid Efficiency Gains

Simply Wall St

Reviewed by Simply Wall St

- Newmont Corporation’s second-quarter earnings, released in the past week, surpassed analyst estimates for both revenue and earnings per share, following a period of cost-cutting initiatives and operational improvements.

- This performance has sparked optimism among analysts, who raised their consensus earnings forecasts and pointed to Newmont’s focus on efficiency even as the company navigates industry-wide challenges.

- With recent analyst upgrades highlighting robust cost control, we’ll explore how these developments could influence Newmont’s broader investment outlook.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Newmont Investment Narrative Recap

To own Newmont, you need confidence in the company’s ability to manage costs and drive stable returns in a sector shaped by volatile gold prices and operational risks. The recent surge in second-quarter earnings and revenue has brightened the near-term catalyst, effective efficiency gains, with the most significant risk still stemming from planned higher capital expenditures that could strain cash flows if gold prices weaken. While this quarter’s performance boosts sentiment, it does not materially shift these key drivers just yet.

Among recent announcements, Newmont’s new US$3,000 million share repurchase program stands out. By returning more capital to shareholders and efficiently deploying available cash, this move aligns directly with the catalysts driving optimism, especially in light of ongoing cost control and asset divestments to support financial flexibility.

Yet, despite rising earnings and optimism, investors should be aware that higher sustained capital expenditures could pressure returns in future periods if...

Read the full narrative on Newmont (it's free!)

Newmont's narrative projects $21.6 billion revenue and $6.4 billion earnings by 2028. This requires 1.6% yearly revenue growth and a $0.2 billion increase in earnings from $6.2 billion.

Uncover how Newmont's forecasts yield a $72.33 fair value, a 3% downside to its current price.

Exploring Other Perspectives

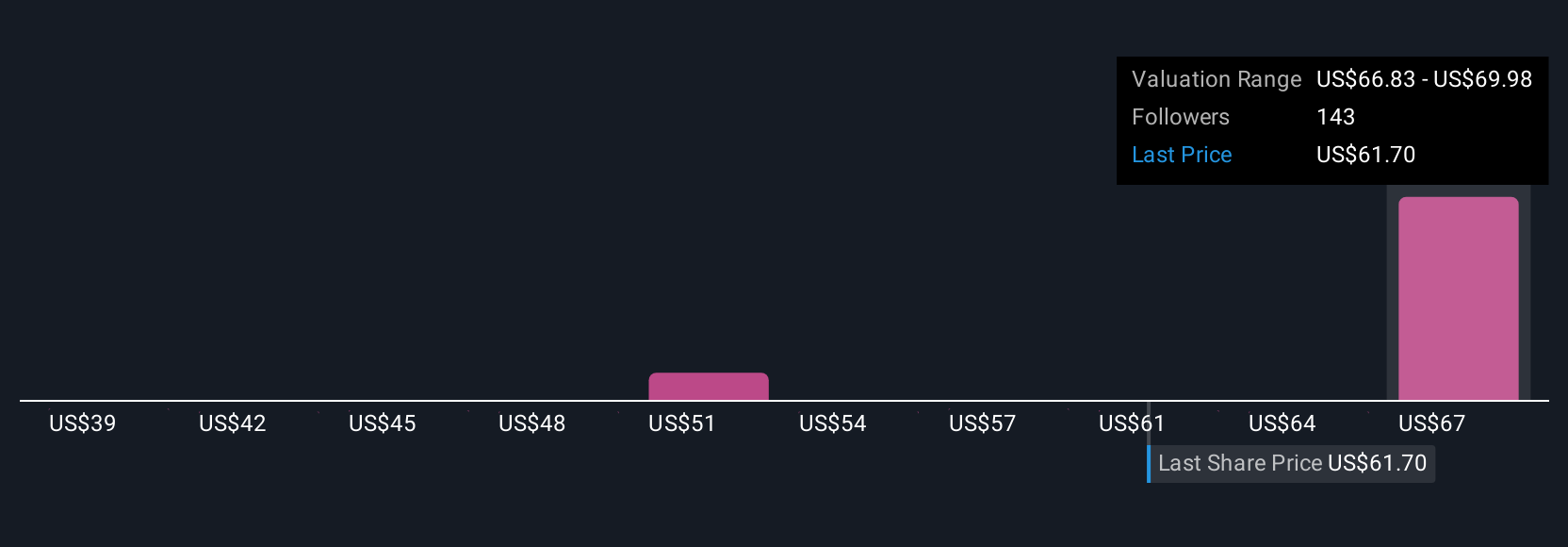

Private investors in the Simply Wall St Community have set fair value estimates ranging from US$40 to US$91.39 across 11 analyses. With many expecting persistent cost discipline to boost margins, it’s clear opinions differ and several viewpoints are available for you to compare.

Explore 11 other fair value estimates on Newmont - why the stock might be worth 46% less than the current price!

Build Your Own Newmont Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Newmont research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Newmont research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Newmont's overall financial health at a glance.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Newmont might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:NEM

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|75.8% undervalued

JO

Community Contributor

PayPal's Future Growth Through Venmo and Merchant Solutions

Fair Value US$105.25|34.2% undervalued

ZW

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$26.54|9.7% overvalued

BL

Community Contributor