Advertisement

- United States

- /

- Chemicals

- /

- NYSE:ECL

Assessing Ecolab (ECL) Valuation After Recent Share Price Weakness And Premium Earnings Multiple

Ecolab stock reacts to recent trading performance

Ecolab (ECL) has drawn attention after the stock declined about 14% over the past 3 months, with a recent 1.6% pullback. This has prompted investors to reassess the water, hygiene, and infection prevention specialist.

See our latest analysis for Ecolab.

That recent 3 month share price decline of about 14% contrasts with a 3 year total shareholder return of 52.35%, suggesting short term momentum has faded even as longer term holders have still seen gains.

If you are reassessing your portfolio after Ecolab’s recent pullback, it could be a good moment to broaden your search with the 20 top founder-led companies

With Ecolab stock down over the past year but still carrying a premium valuation score, investors now have to ask: is this a chance to pick up a quality compounder at a discount, or is the market already pricing in future growth?

Most Popular Narrative: 19.7% Undervalued

At a last close of $256, the most followed narrative places Ecolab’s fair value at $318.95, framing recent share weakness against a higher long term earnings story.

Ecolab digital experienced a 12% sales growth, primarily driven by subscription revenue, and the company aims to capitalize on this high-margin opportunity by expanding digital offerings. This is expected to significantly impact sales growth and operating income margins as these offerings scale.

Want the full picture behind that valuation gap? The narrative focuses on steady top line growth, wider margins and a higher future earnings multiple. Curious which assumptions really move that fair value?

Result: Fair Value of $318.95 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, softer demand in heavy industrial markets and higher costs linked to tariffs and local suppliers could put pressure on the margin improvement that this narrative relies on.

Find out about the key risks to this Ecolab narrative.

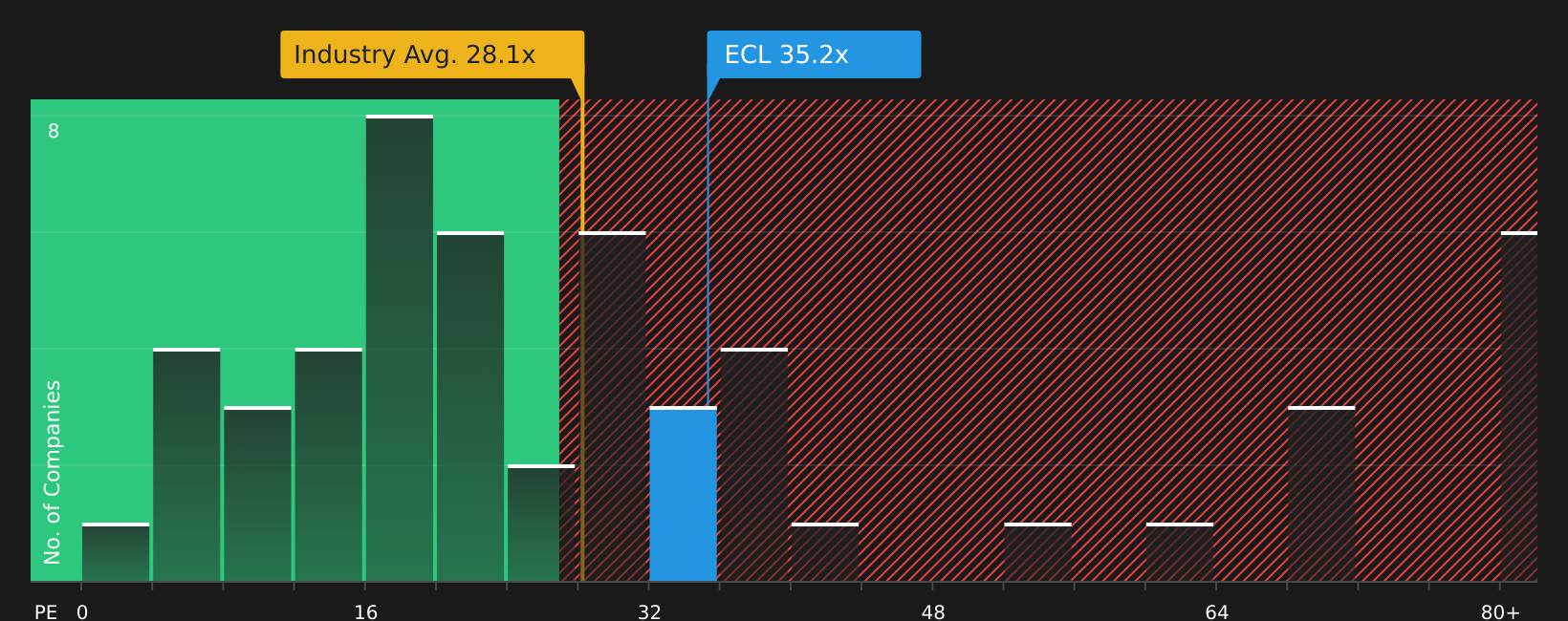

Another View: Valuation Tension From Earnings Multiples

The 19.7% undervaluation from the analyst narrative sits awkwardly beside how the market is actually pricing Ecolab today. The stock trades on a P/E of 34.2x, compared with 22.1x for peers and a fair ratio of 24.5x. This points to a rich earnings multiple and higher valuation risk if sentiment cools.

For a closer look at how this earnings multiple compares with what the fair ratio suggests the market could move toward, have a look at the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Given the mix of optimism and concern through this article, it makes sense to check the underlying data yourself and decide where you stand. To see both sides of the story in one place, review the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If you are reassessing Ecolab today, do not stop at a single stock. Use the Simply Wall Street Screener to surface fresh ideas that fit your style.

- Target higher quality at better prices by scanning for companies flagged as 46 high quality undervalued stocks that might suit a value focused watchlist.

- Strengthen the defensive side of your portfolio by filtering for 64 resilient stocks with low risk scores that aim for steadier returns with fewer surprises.

- Get ahead of the crowd by reviewing a screener containing 22 high quality undiscovered gems before attention and pricing potentially shift.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Ecolab might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ECL

Ecolab

Provides water, hygiene, and infection prevention solutions and services in the United States and internationally.

Average dividend payer with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$470.5% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9719.1% undervalued

55 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1925.7% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$19.251.3% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

KA

kapirey on Hangzhou Oxygen Plant Group ·

The company must capitalize on its R&D&I over the next 10 years; it is still too early to infer the outcome.

Fair Value:CN¥24.481.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Sinopec Shanghai Petrochemical ·

Capital expenditures remain required regardless of profitability

Fair Value:HK$0.32259.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on Catcha Digital Berhad ·

Catcha Digital Q1 FY2026 Analysis - Acquisition-led growth is starting to convert into stronger operating earnings

Fair Value:RM 0.5451.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.4% undervalued

122 followersusers have followed this narrative

2 commentsusers have commented on this narrative

34 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9719.1% undervalued

55 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1925.7% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative