Advertisement

- United States

- /

- Chemicals

- /

- NYSE:CC

Chemours (CC): How Analyst Optimism and TiO2 Market Shifts Are Shaping the Company's Valuation Outlook

Simply Wall St

Reviewed by Kshitija Bhandaru

If you have been keeping an eye on Chemours (NYSE:CC) lately, you have probably noticed the wave of analyst buzz circling the stock. What is behind this renewed attention? Recent commentary is shining a spotlight on some key tailwinds, such as steady pricing in the titanium dioxide (TiO2) market and the expected impact of anti-dumping duties on Chinese exports. Add in signs of progress addressing litigation risk, and it is no wonder more investors are revisiting their outlook for the chemical maker.

This shift in sentiment comes after a bumpy year. While shares have climbed more than 33% over the past three months, helping to recover from earlier declines, the one-year return still lags in negative territory. The recent rebound follows positive updates on settlements and ongoing optimism about Chemours' earnings potential, which contrasts with the deeper three- and five-year losses. It appears that momentum is starting to build again, but the long-term chart underscores the company’s need to deliver on its turnaround story.

So with fresh optimism from analysts and positive trends taking shape, is Chemours trading at an attractive entry point, or is the market already pricing in all the upside ahead?

Most Popular Narrative: Fairly Valued

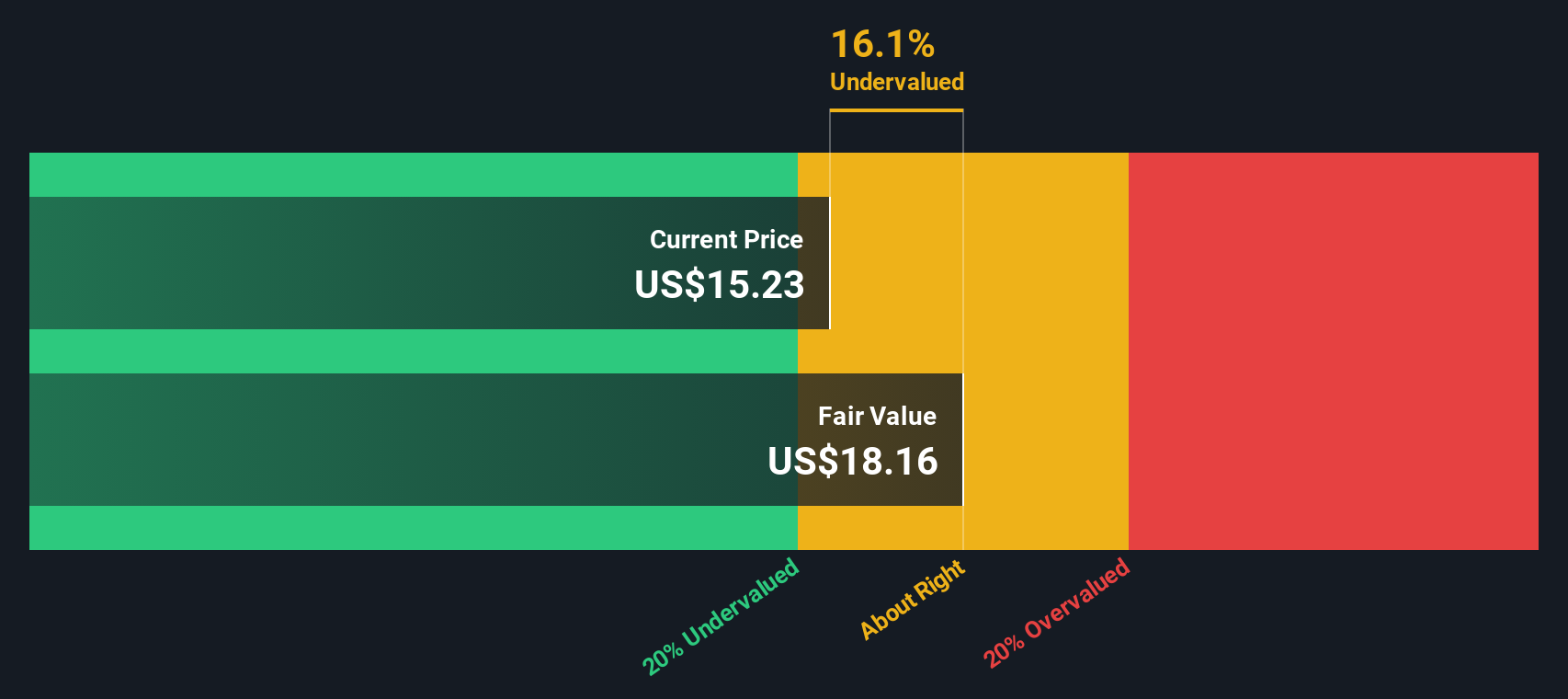

The most widely followed narrative sees Chemours as fairly valued at current prices, with only a minimal 1.4% discount to fair value under the latest analyst consensus and a discount rate of 10.83%.

Acceleration in regulatory-driven adoption of low global warming potential (GWP) refrigerants is boosting sustained demand for Chemours' Opteon franchise. Recent strong net sales and high margins signal that continued market share gains and capacity expansions will drive robust revenue and EBITDA growth through and beyond the 2025 and 2026 transition periods.

Curious what’s fueling Chemours’ turnaround story? This narrative hinges on a bold mix of future profit growth and aggressive margin improvement, driven by bets on next-generation refrigerants and portfolio upgrades. Want to know the precise projections and daring assumptions that underpin this fair valuation? Unlock the details and see which numbers make the difference.

Result: Fair Value of $15.44 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.However, ongoing legal uncertainties and rising regulatory scrutiny related to environmental issues could quickly overturn the narrative driving current optimism for Chemours.

Find out about the key risks to this Chemours narrative.Another View: Discounted Cash Flow Analysis

Taking a different angle, our DCF model suggests Chemours may actually be undervalued compared to the current share price. Could this imply that the recent optimism in the market is still not fully priced in?

Look into how the SWS DCF model arrives at its fair value.

Stay updated when valuation signals shift by adding Chemours to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own Chemours Narrative

If you see things differently or enjoy digging into the numbers on your own, you can craft your own perspective in just a few minutes. Do it your way.

A great starting point for your Chemours research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Investment Ideas?

Don’t limit your strategy to just one stock. Take charge and expand your investing approach with standout opportunities that other investors are watching right now:

- Uncover overlooked potential by scanning undervalued stocks based on cash flows. This is perfect for spotting stocks trading below their true worth before the crowd catches on.

- Tap into game-changing innovation and stay ahead of market trends with AI penny stocks powering the next wave in artificial intelligence.

- Secure reliable income streams when you check out dividend stocks with yields > 3% and find companies rewarding shareholders with healthy yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CC

Chemours

Provides performance chemicals in North America, the Asia Pacific, Europe, the Middle East, Africa, and Latin America.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor