- United States

- /

- Chemicals

- /

- NasdaqGS:SOLS

Is Solstice Advanced Materials Fairly Priced After Recent EV Supply Agreements and Share Price Jump?

Reviewed by Bailey Pemberton

- If you are wondering whether Solstice Advanced Materials is still flying under the radar or already priced for perfection, you are not alone. This stock has quietly moved onto many watchlists.

- In the last week the share price has climbed 4.5%, and over the past 30 days it is up a solid 12.0%, even though year to date it is only slightly ahead at 0.8%.

- Much of that recent momentum has followed upbeat commentary around demand for next generation battery materials and new supply agreements with EV manufacturers, which have sharpened investor focus on Solstice's growth runway. At the same time, sector wide optimism around advanced materials has lifted several peers, giving Solstice both a rising tide and company specific tailwinds.

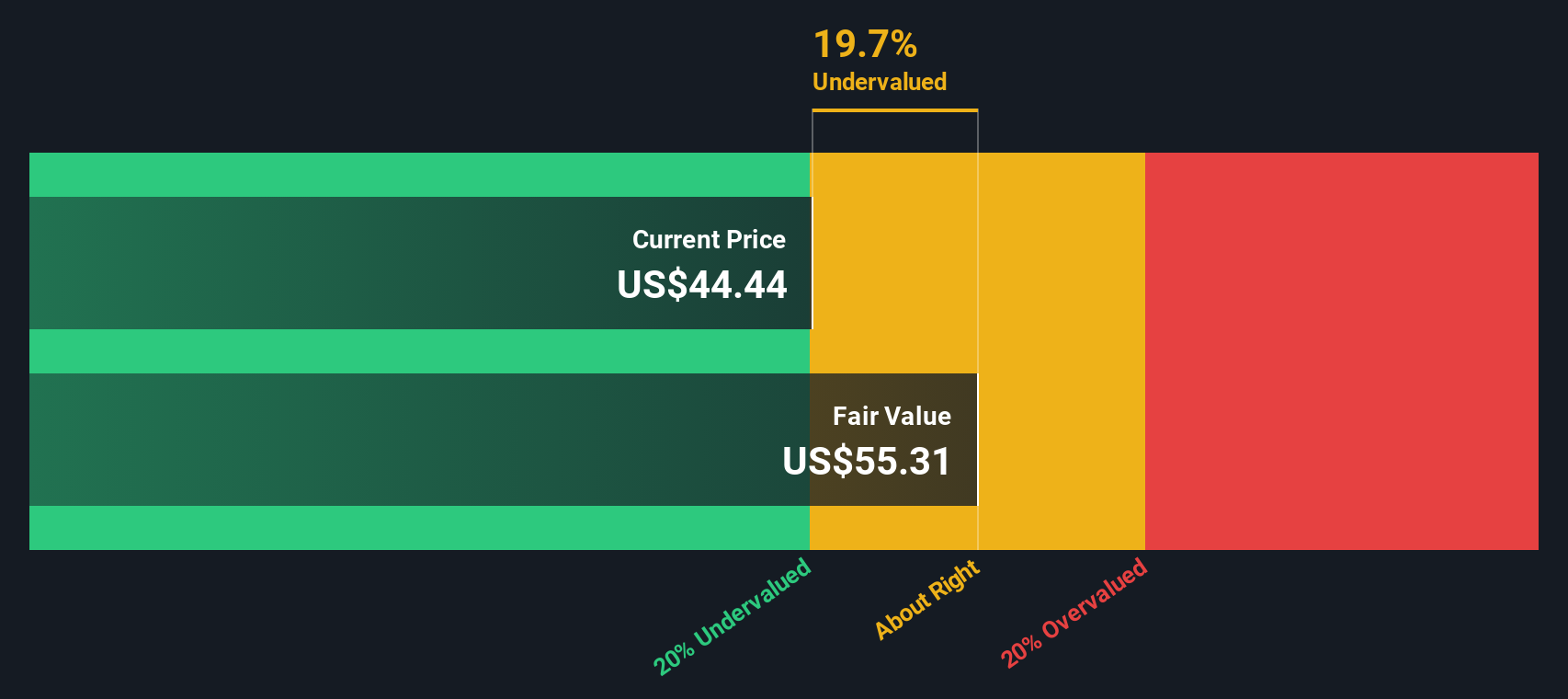

- On our framework the stock earns a valuation score of 2/6, suggesting it screens as undervalued on only a couple of checks. In the sections that follow we will walk through those valuation methods in detail, then finish with a more holistic way to think about what Solstice is really worth.

Solstice Advanced Materials scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Solstice Advanced Materials Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and discounting those cash flows back to their value in today's dollars. For Solstice Advanced Materials, the model starts with last twelve months free cash flow of about $247.9 Million and then applies a two stage Free Cash Flow to Equity approach using analyst forecasts for the next few years, with further years extrapolated by Simply Wall St based on more modest growth assumptions.

Under this framework, Solstice's free cash flow is expected to grow to roughly the mid $400 Million range by 2035, as shown by the ten year projections. When all those future cash flows in dollars are discounted back and combined with an estimate of value beyond the explicit forecast period, the model produces an intrinsic value of about $55.51 per share. Compared with the current share price, this implies the stock trades at roughly a 12.1% discount and appears undervalued on a DCF basis.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Solstice Advanced Materials is undervalued by 12.1%. Track this in your watchlist or portfolio, or discover 908 more undervalued stocks based on cash flows.

Approach 2: Solstice Advanced Materials Price vs Earnings

For profitable businesses like Solstice Advanced Materials, the price to earnings, or PE, ratio is a useful way to gauge whether investors are paying a reasonable price for each dollar of current earnings. In general, companies with faster, more reliable earnings growth and lower perceived risk tend to justify a higher, or more expensive, PE multiple, while slower growth or higher uncertainty usually demands a lower PE to compensate investors.

Solstice currently trades on a PE of about 23.5x, which is broadly in line with the wider Chemicals industry average of roughly 24.0x, but sits well above the peer group average near 16.7x. To move beyond these simple comparisons, Simply Wall St uses a proprietary Fair Ratio, which is the PE multiple that would be expected for Solstice given its specific earnings growth outlook, profitability, industry positioning, size and risk profile. This Fair Ratio is more insightful than raw peer or industry comparisons because it adjusts for fundamentals rather than assuming all companies deserve the same multiple. On this framework, Solstice's current PE is close to its Fair Ratio, suggesting the market price is largely in line with what its earnings profile supports.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Solstice Advanced Materials Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework that lets you attach a clear story to your numbers, including your fair value, and your assumptions for Solstice Advanced Materials future revenue, earnings and margins. A Narrative links what you believe about the company, such as demand for advanced battery materials or competitive pressure, to a concrete financial forecast and then to a fair value estimate that you can easily compare with today’s share price to help inform a decision to buy, hold or sell. On Simply Wall St, millions of investors build and share these Narratives on the Community page, and they update dynamically as fresh news, earnings or guidance change the outlook. For example, one Solstice Narrative might see modest revenue growth and thinner margins leading to a cautious fair value, while another could assume rapid EV adoption, improving profitability and a much higher fair value.

Do you think there's more to the story for Solstice Advanced Materials? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SOLS

Solstice Advanced Materials

Operates as a specialty chemicals and advanced materials company in the United States and internationally.

Excellent balance sheet with reasonable growth potential.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)