Advertisement

- United States

- /

- Insurance

- /

- NYSE:CNA

CNA Financial's Valuation: Assessing Renewed Investor Confidence After Strong Q3 Results

Simply Wall St

Reviewed by Simply Wall St

CNA Financial (CNA) posted third quarter results that highlight disciplined underwriting and improved investment income, providing investors with a clearer view of the company's financial standing. Management also noted gains in the International segment and ongoing efficiency efforts.

See our latest analysis for CNA Financial.

After a bumpy spell earlier in the year, CNA Financial’s shares have shown a burst of momentum lately, with a 1-month share price return of 6.5% and a current price of $46.93. The company’s growing track record is hard to ignore, reflected in a 1-year total shareholder return of 0.8% and an impressive 84% over five years. These results may indicate value building over time and renewed investor confidence following strong quarterly results.

If CNA’s recent rebound got your attention, now’s a great time to broaden your search and discover fast growing stocks with high insider ownership

The question for investors now is whether CNA Financial's recent momentum signals a bargain opportunity, or if the market has already recognized its future growth prospects in the current share price. Is there still value to be found here?

Price-to-Earnings of 12.7x: Is it justified?

CNA Financial’s shares currently trade at a price-to-earnings (P/E) ratio of 12.7x, lower than both the US Insurance industry average of 13.2x and the peer average of 13.8x. At the most recent close of $46.93, the market assigns a discount relative to these benchmarks, which may indicate potential undervaluation.

The P/E ratio is a widely used metric that compares a company’s share price to its earnings per share, providing a quick sense of how much investors are willing to pay for each dollar of profit. For insurance companies like CNA Financial, a lower P/E can signal that the market is not fully pricing in current or future earnings strength.

Given that CNA’s P/E is not only beneath the average for its direct peers but also below the broader US Insurance industry, this suggests the market could be overlooking some positive fundamentals. Importantly, our fair P/E ratio analysis points to an estimated fair P/E for CNA of 16.3x, a level the market could move towards as performance and sentiment change.

Explore the SWS fair ratio for CNA Financial

Result: Price-to-Earnings of 12.7x (UNDERVALUED)

However, risks remain, including market volatility and earnings growth uncertainty. Both of these factors could impact CNA Financial’s appeal as an undervalued opportunity.

Find out about the key risks to this CNA Financial narrative.

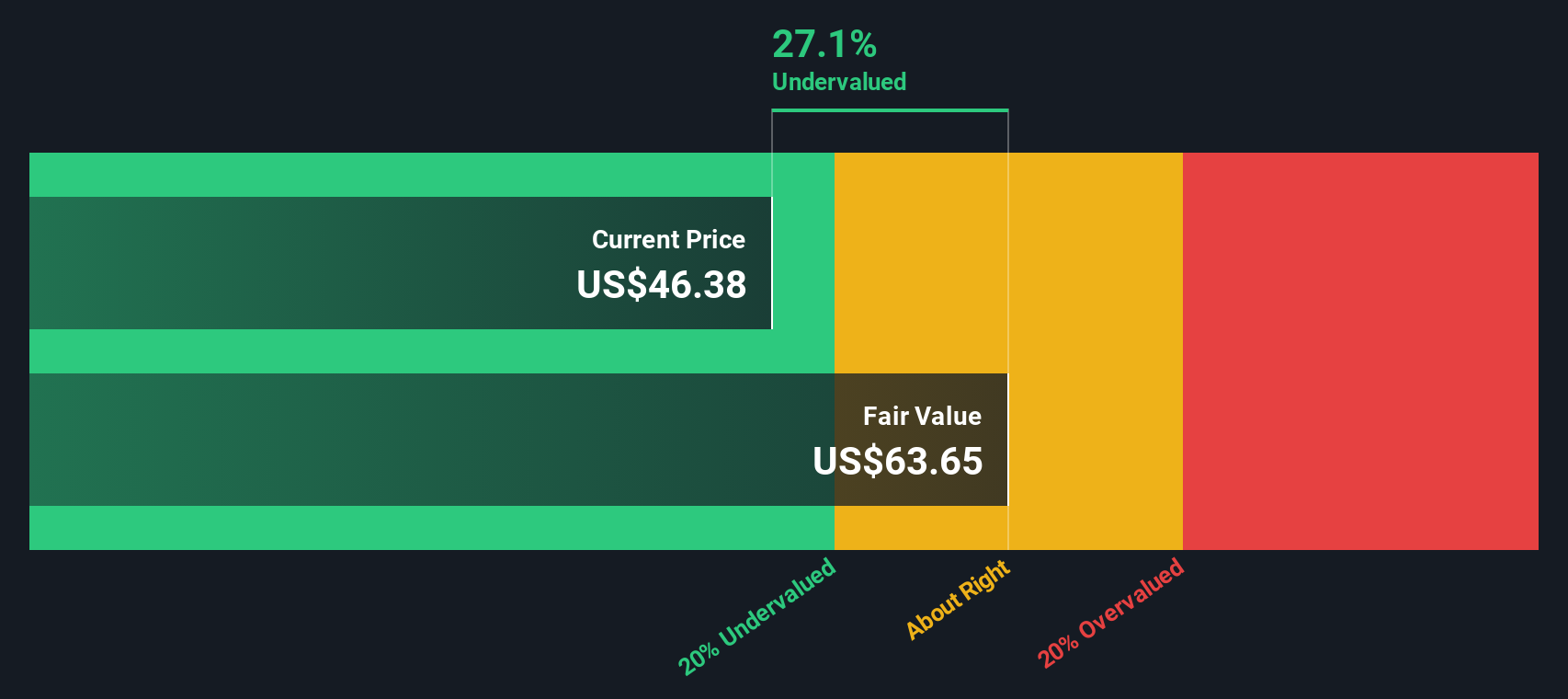

Another View: Our DCF Model Adds Perspective

For a different perspective, our SWS DCF model suggests CNA Financial shares are trading at a 26% discount to fair value, with a calculated fair value of $63.65 compared to the current price of $46.93. This result also indicates potential undervaluation, but questions remain about whether future cash flows could support such potential upside or if the discount signals the need for further analysis.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out CNA Financial for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 923 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own CNA Financial Narrative

If you see the numbers differently, or want to test your own assumptions, you can craft an independent narrative based on your own research in just a few minutes. Do it your way.

A great starting point for your CNA Financial research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors never settle for just one opportunity. Expand your horizons and get ahead of the curve by checking out handpicked stock lists for your next move.

- Maximize your income potential with these 15 dividend stocks with yields > 3%, which features top companies with yields over 3% and strong payout histories.

- Tap into major tech trends by targeting these 25 AI penny stocks, where fast-moving innovators are shaping the landscape of artificial intelligence and automation.

- Position yourself at the forefront of finance by analyzing these 82 cryptocurrency and blockchain stocks; explore businesses powering secure payments, digital assets, and blockchain solutions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CNA

CNA Financial

An insurance holding company, primarily provides commercial property and casualty insurance products in the United States and internationally.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative