- United States

- /

- Insurance

- /

- NYSE:AON

Aon (AON) Valuation Check as Lawsuit Targets Howden Over Alleged Talent Raid and Data Misuse

Reviewed by Simply Wall St

Aon (AON) has escalated its rivalry with Howden into the courts, alleging a coordinated raid on its US brokerage talent and confidential data that pulled more than 45 employees toward the competitor.

See our latest analysis for Aon.

Despite the legal flare up with Howden and a steady drumbeat of operational updates, Aon’s latest share price of $353.79 leaves it roughly flat year to date on a share price return basis. At the same time, a solid five year total shareholder return of about 76 percent suggests the longer term compounding story remains intact even as near term momentum looks subdued.

If this kind of competitive tension has you rethinking your portfolio mix, it could be a good moment to broaden your search and explore fast growing stocks with high insider ownership.

With shares largely treading water this year and analysts still seeing upside to their targets, investors face a familiar dilemma: is Aon quietly undervalued here, or is the market already factoring in its next leg of growth?

Most Popular Narrative: 11.7% Undervalued

With Aon’s shares last closing at $353.79 against a narrative fair value near $400.50, the story leans toward upside if execution holds.

Aon's 3x3 Plan and the deployment of Risk Analyzers have increased new business and improved client retention, strengthening the foundation for ongoing revenue growth and margin expansion.

Investment in priority hires and expanding Aon Business Services (ABS) capabilities are creating capacity to fund growth initiatives and drive operational efficiencies, benefiting net margins and earnings.

Curious how steady mid single digit growth, rising margins and a premium future earnings multiple can still imply upside for a mature broker? The narrative lays out a detailed roadmap of compounding cash flows, capital returns and shrinking share count that must all line up to justify that valuation path.

Result: Fair Value of $400.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, stubborn macro volatility and softer commercial risk pricing could derail those bullish assumptions if client budgets tighten and insurance markets weaken further.

Find out about the key risks to this Aon narrative.

Another Angle on Valuation

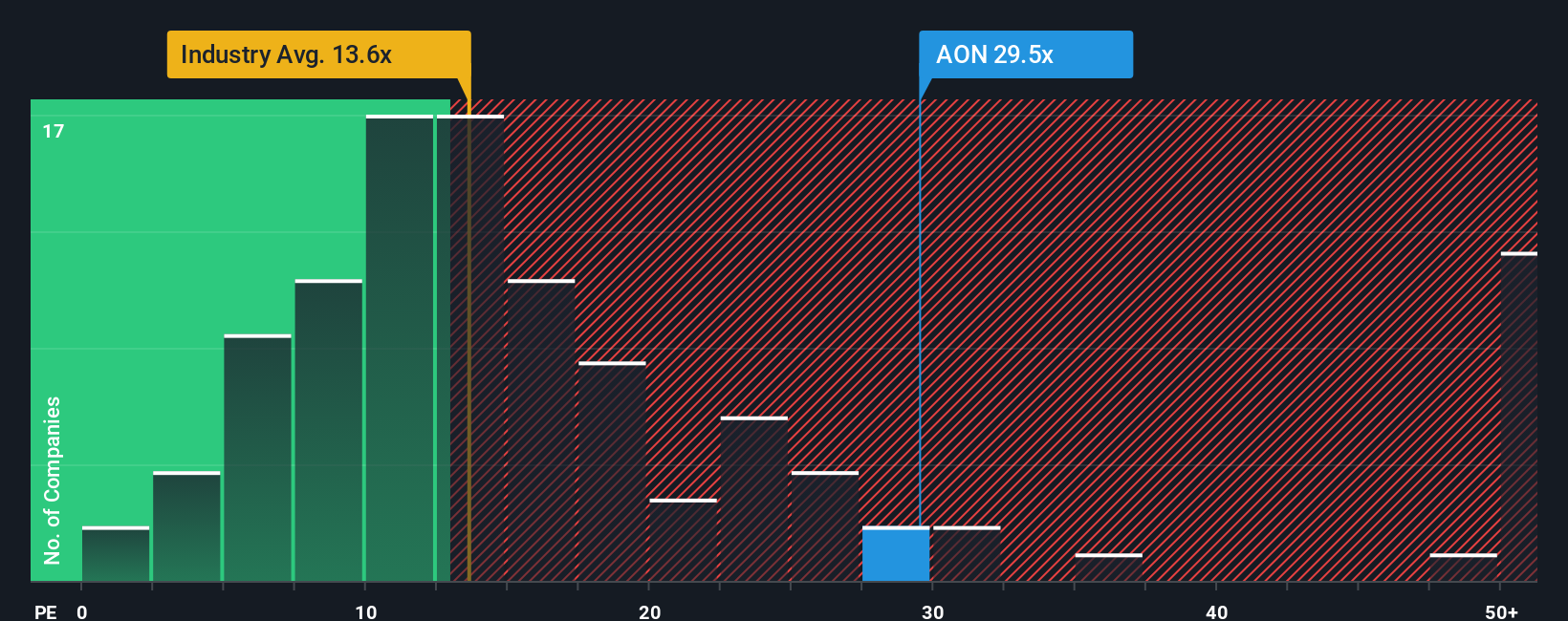

Viewed through its earnings multiple, Aon looks far less forgiving. The stock trades on about 28 times earnings, richer than both the US insurance industry at roughly 13 times and close peers at 26.5 times, and well above a fair ratio near 15.7 times that the market could gravitate toward over time.

That gap suggests less of a bargain and more of a valuation tightrope, where any stumble in growth or margins could trigger a painful reset rather than a gentle de rating. How confident are you that execution will keep justifying this premium?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Aon Narrative

If this framework does not match your own view or you prefer to dig into the numbers yourself, you can build a fresh narrative in minutes, Do it your way.

A great starting point for your Aon research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next smart move by hunting for fresh opportunities that match your style, instead of waiting for the market to surprise you.

- Target consistent income by scanning these 13 dividend stocks with yields > 3% that aim to balance yield with solid fundamentals and resilient cash flows.

- Ride structural growth trends by focusing on these 30 healthcare AI stocks that blend medical innovation with scalable AI driven platforms.

- Position ahead of digital finance shifts by tracking these 80 cryptocurrency and blockchain stocks pushing real world adoption of blockchain and tokenized ecosystems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:AON

Aon

A professional services firm, provides a range of risk and human capital solutions worldwide.

Proven track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)