Advertisement

- United States

- /

- Auto Components

- /

- NasdaqGS:HSAI

Three Stocks That May Be Undervalued In August 2025

Simply Wall St

Reviewed by Simply Wall St

As of late August 2025, the U.S. stock market is experiencing a period of optimism, with major indices like the S&P 500 and Dow Jones Industrial Average reaching record highs. Amid this bullish environment, identifying undervalued stocks can be challenging yet rewarding for investors seeking opportunities that may not be fully recognized by the market.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Willdan Group (WLDN) | $116.18 | $231.93 | 49.9% |

| Udemy (UDMY) | $6.96 | $13.21 | 47.3% |

| Peapack-Gladstone Financial (PGC) | $28.90 | $56.54 | 48.9% |

| Northwest Bancshares (NWBI) | $12.63 | $24.41 | 48.3% |

| Niagen Bioscience (NAGE) | $9.82 | $18.89 | 48% |

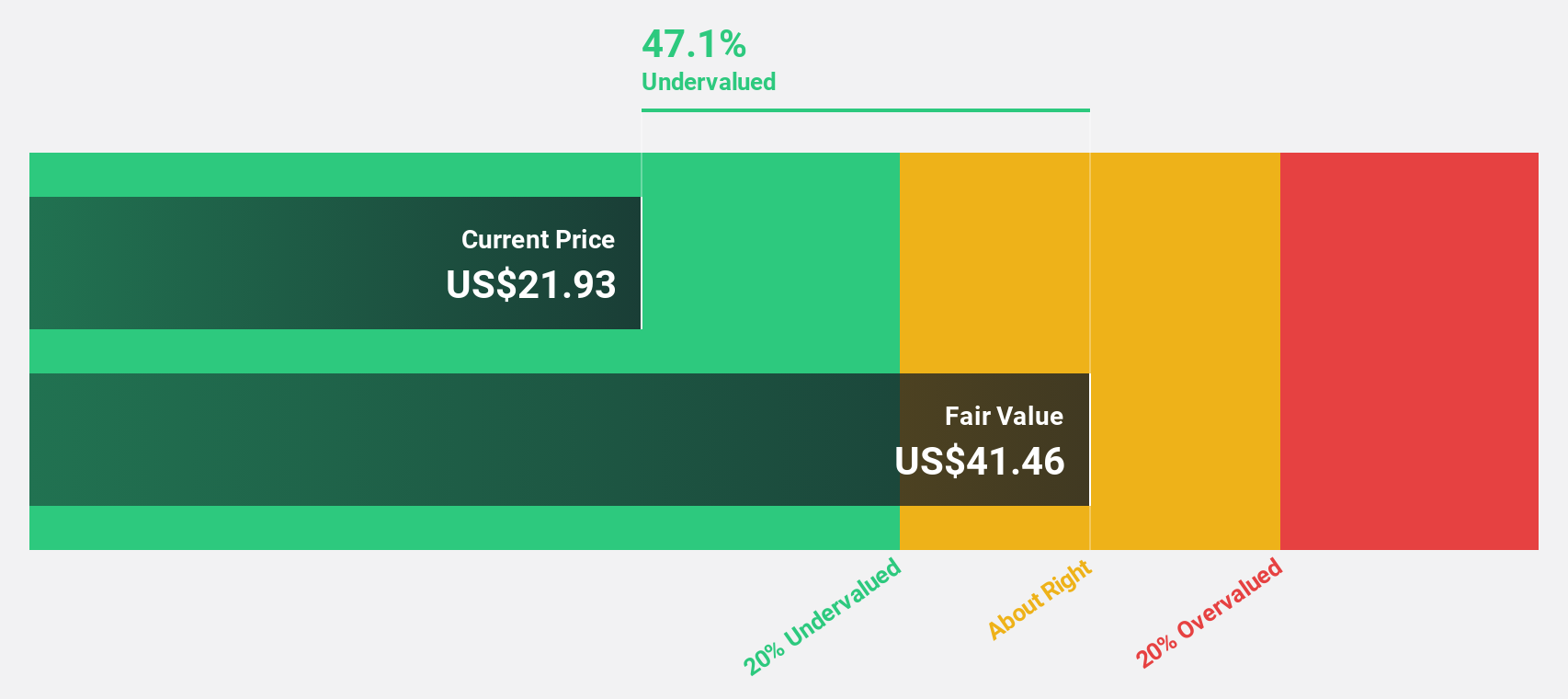

| Lyft (LYFT) | $16.135 | $30.98 | 47.9% |

| Investar Holding (ISTR) | $23.61 | $45.80 | 48.4% |

| Gold Royalty (GROY) | $3.28 | $6.55 | 49.9% |

| Fiverr International (FVRR) | $23.62 | $45.28 | 47.8% |

| AGNC Investment (AGNC) | $9.79 | $18.63 | 47.5% |

Let's explore several standout options from the results in the screener.

Hesai Group (HSAI)

Overview: Hesai Group develops, manufactures, and sells three-dimensional LiDAR solutions across Mainland China, Europe, North America, and other international markets with a market cap of $3.44 billion.

Operations: Hesai Group generates revenue from the development, manufacturing, and sales of three-dimensional LiDAR solutions across various regions including Mainland China, Europe, North America, and other international markets.

Estimated Discount To Fair Value: 25.2%

Hesai Group is trading at a 25.2% discount to its estimated fair value of US$35.86, making it potentially undervalued based on discounted cash flow analysis. The company recently turned profitable, reporting CNY 44.09 million in net income for Q2 2025, and forecasts suggest significant earnings growth of over 40% annually for the next three years. However, investors should note the stock's high volatility and recent plans to raise US$300 million through a Hong Kong listing.

- Our comprehensive growth report raises the possibility that Hesai Group is poised for substantial financial growth.

- Dive into the specifics of Hesai Group here with our thorough financial health report.

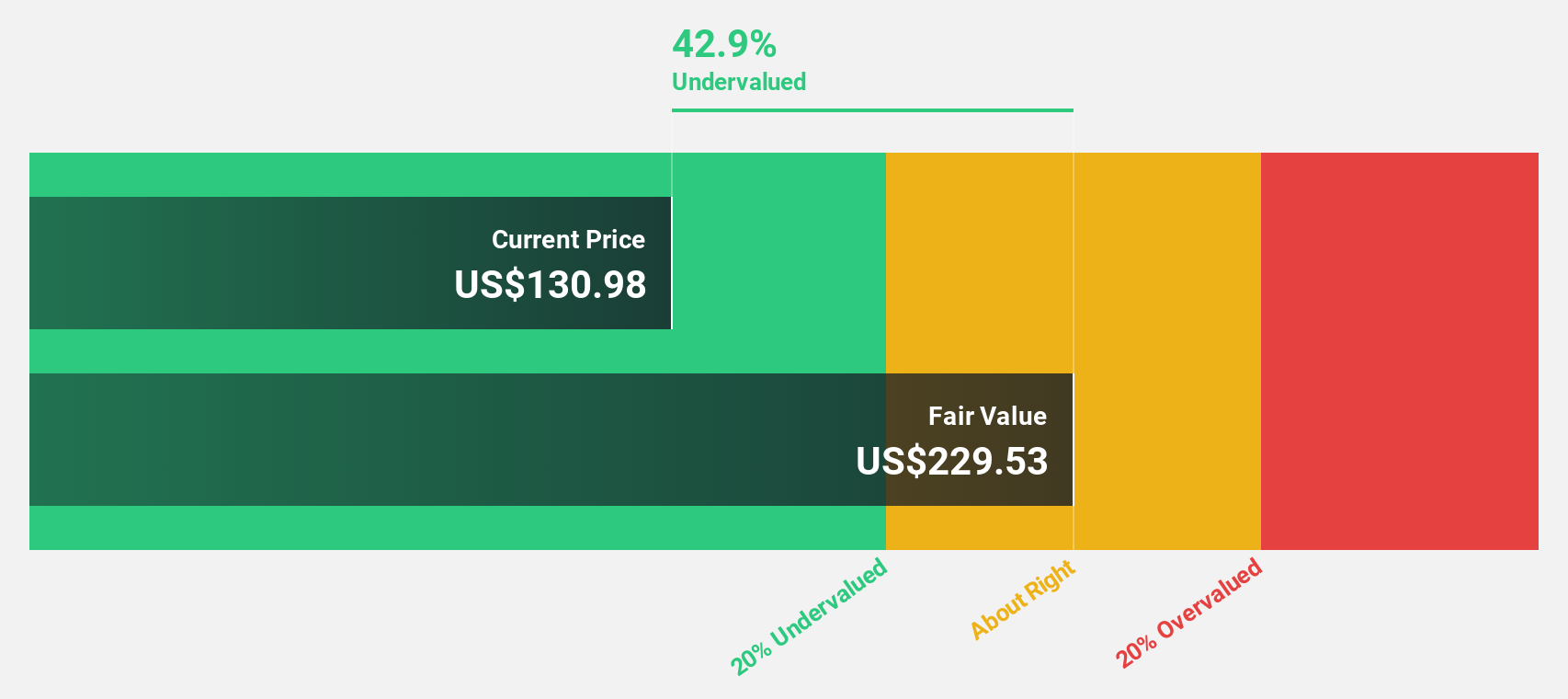

e.l.f. Beauty (ELF)

Overview: e.l.f. Beauty, Inc. is a global beauty company offering cosmetics and skincare products, with a market cap of $7.41 billion.

Operations: The company's revenue is primarily generated from its Personal Products segment, totaling $1.34 billion.

Estimated Discount To Fair Value: 42.2%

e.l.f. Beauty is trading at US$129.35, significantly below its estimated fair value of US$223.88, suggesting it may be undervalued based on discounted cash flow analysis. Despite a decline in profit margins from 10.8% to 7.3%, the company's earnings are expected to grow significantly over the next three years, outpacing the broader U.S. market growth rate of 15.1%. However, recent insider selling could be a concern for potential investors.

- In light of our recent growth report, it seems possible that e.l.f. Beauty's financial performance will exceed current levels.

- Navigate through the intricacies of e.l.f. Beauty with our comprehensive financial health report here.

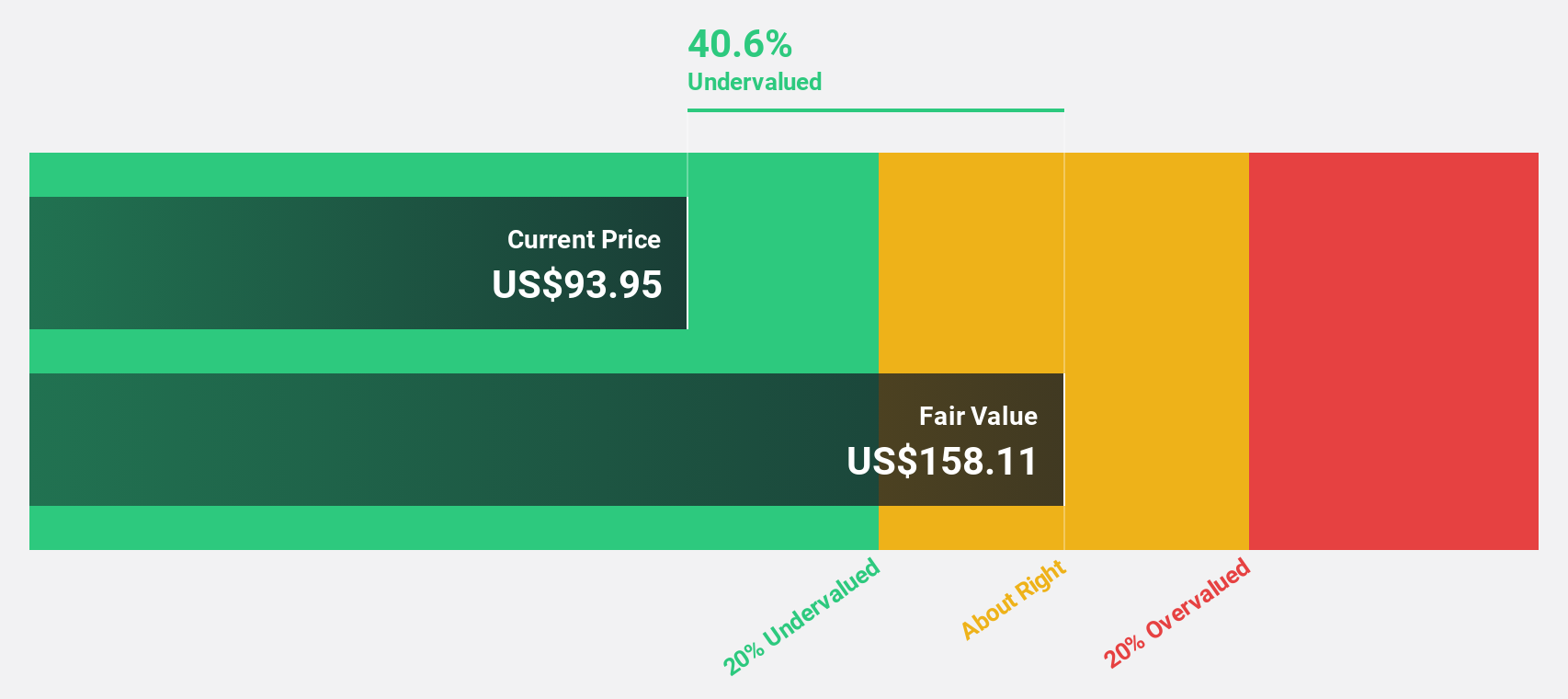

Glaukos (GKOS)

Overview: Glaukos Corporation is an ophthalmic pharmaceutical and medical technology company that develops therapies for glaucoma, corneal disorders, and retinal diseases globally, with a market cap of approximately $5.45 billion.

Operations: The company generates revenue of $432.95 million from the development and commercialization of ophthalmic therapies for glaucoma, corneal disorders, and retinal diseases.

Estimated Discount To Fair Value: 38.9%

Glaukos Corporation is trading at US$96.56, well below its estimated fair value of US$158.10, indicating potential undervaluation based on cash flow analysis. The company has raised its 2025 revenue guidance to US$480 million-US$486 million and reported significant sales growth in Q2 2025 compared to the previous year. While Glaukos is expected to become profitable within three years, its forecasted return on equity remains low at 1.9%.

- Our earnings growth report unveils the potential for significant increases in Glaukos' future results.

- Click to explore a detailed breakdown of our findings in Glaukos' balance sheet health report.

Make It Happen

- Click through to start exploring the rest of the 187 Undervalued US Stocks Based On Cash Flows now.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hesai Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:HSAI

Hesai Group

Through with its subsidiaries, engages in the development, manufacture, and sale of three-dimensional light detection and ranging solutions (LiDAR) in Mainland China, Europe, North America, and internationally.

Exceptional growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|50.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|8.5% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|18.4% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|54.2% overvalued

RO

Community Contributor