Advertisement

- United States

- /

- Personal Products

- /

- NasdaqCM:SKIN

The Market Doesn't Like What It Sees From The Beauty Health Company's (NASDAQ:SKIN) Revenues Yet As Shares Tumble 40%

The Beauty Health Company (NASDAQ:SKIN) shares have had a horrible month, losing 40% after a relatively good period beforehand. The recent drop has obliterated the annual return, with the share price now down 3.2% over that longer period.

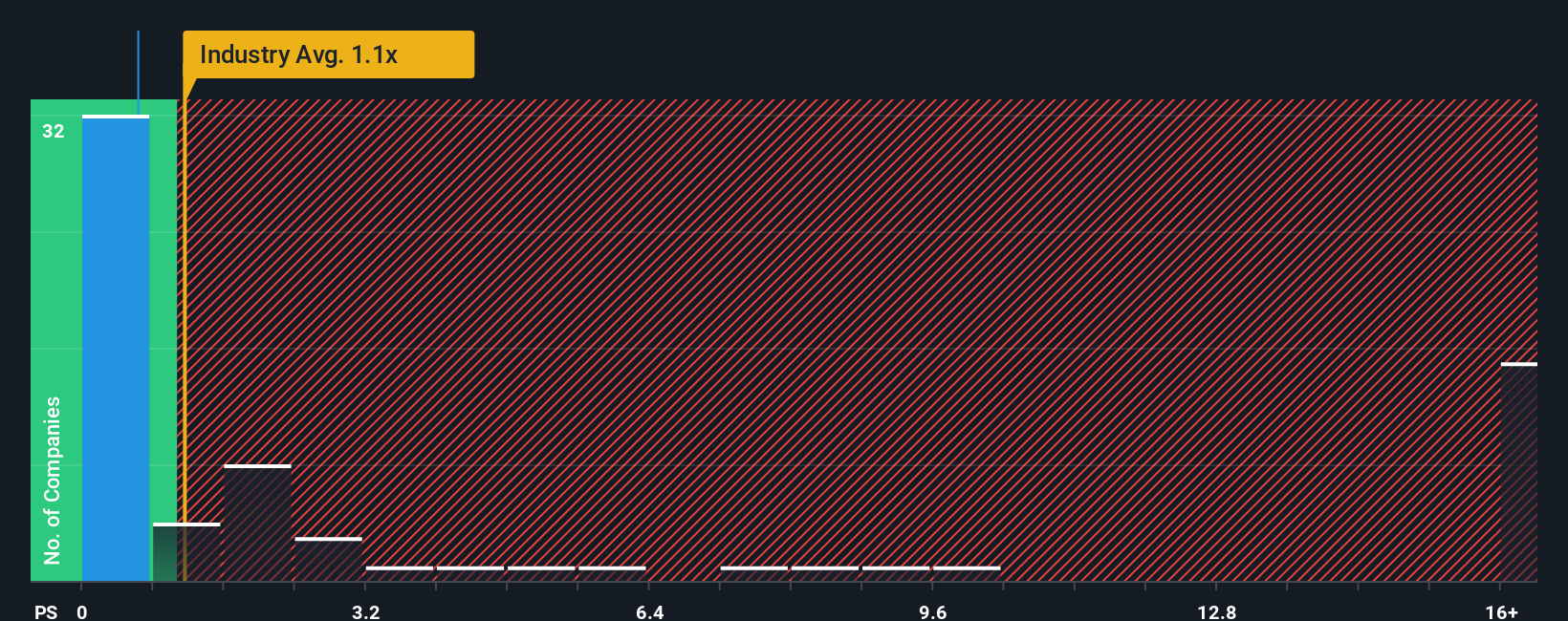

Since its price has dipped substantially, Beauty Health's price-to-sales (or "P/S") ratio of 0.6x might make it look like a buy right now compared to the Personal Products industry in the United States, where around half of the companies have P/S ratios above 1.1x and even P/S above 4x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

Check out our latest analysis for Beauty Health

How Has Beauty Health Performed Recently?

Beauty Health has been struggling lately as its revenue has declined faster than most other companies. The P/S ratio is probably low because investors think this poor revenue performance isn't going to improve at all. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Keen to find out how analysts think Beauty Health's future stacks up against the industry? In that case, our free report is a great place to start.Is There Any Revenue Growth Forecasted For Beauty Health?

In order to justify its P/S ratio, Beauty Health would need to produce sluggish growth that's trailing the industry.

Retrospectively, the last year delivered a frustrating 15% decrease to the company's top line. As a result, revenue from three years ago have also fallen 4.6% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 3.2% each year during the coming three years according to the eight analysts following the company. With the industry predicted to deliver 5.7% growth each year, the company is positioned for a weaker revenue result.

In light of this, it's understandable that Beauty Health's P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

Beauty Health's recently weak share price has pulled its P/S back below other Personal Products companies. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As expected, our analysis of Beauty Health's analyst forecasts confirms that the company's underwhelming revenue outlook is a major contributor to its low P/S. Shareholders' pessimism on the revenue prospects for the company seems to be the main contributor to the depressed P/S. The company will need a change of fortune to justify the P/S rising higher in the future.

You should always think about risks. Case in point, we've spotted 3 warning signs for Beauty Health you should be aware of, and 1 of them is concerning.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Beauty Health might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:SKIN

Beauty Health

Designs, develops, manufactures, markets, and sells esthetic technologies and products in the Americas, the Asia-Pacific, Europe, the Middle East, and Africa.

Adequate balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.1% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|11.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|39.4% undervalued

TR

Community Contributor