- United States

- /

- Personal Products

- /

- NasdaqCM:UPXI

Why Grove's (NASDAQ:GRVI) Earnings Are Weaker Than They Seem

We didn't see Grove, Inc.'s (NASDAQ:GRVI) stock surge when it reported robust earnings recently. We looked deeper into the numbers and found that shareholders might be concerned with some underlying weaknesses.

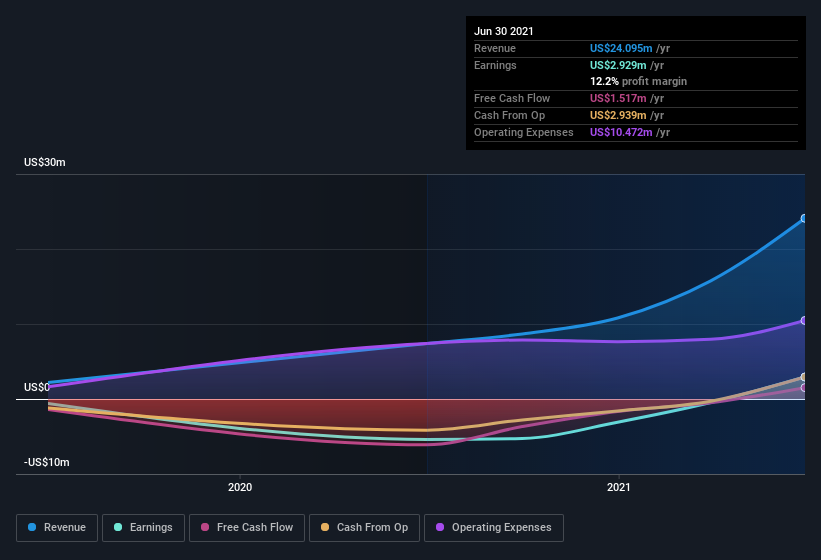

Check out our latest analysis for Grove

Examining Cashflow Against Grove's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. The ratio shows us how much a company's profit exceeds its FCF.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

Over the twelve months to June 2021, Grove recorded an accrual ratio of 0.27. Unfortunately, that means its free cash flow fell significantly short of its reported profits. In fact, it had free cash flow of US$1.5m in the last year, which was a lot less than its statutory profit of US$2.93m. Notably, Grove had negative free cash flow last year, so the US$1.5m it produced this year was a welcome improvement. Having said that it seems that a recent tax benefit and some unusual items have impacted its profit (and this its accrual ratio).

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Grove.

The Impact Of Unusual Items On Profit

Given the accrual ratio, it's not overly surprising that Grove's profit was boosted by unusual items worth US$800k in the last twelve months. We can't deny that higher profits generally leave us optimistic, but we'd prefer it if the profit were to be sustainable. When we crunched the numbers on thousands of publicly listed companies, we found that a boost from unusual items in a given year is often not repeated the next year. And, after all, that's exactly what the accounting terminology implies. Grove had a rather significant contribution from unusual items relative to its profit to June 2021. As a result, we can surmise that the unusual items are making its statutory profit significantly stronger than it would otherwise be.

An Unusual Tax Situation

In addition to the notable accrual ratio, we can see that Grove received a tax benefit of US$1.3m. This is meaningful because companies usually pay tax rather than receive tax benefits. We're sure the company was pleased with its tax benefit. And since it previously lost money, it may well simply indicate the realisation of past tax losses. However, the devil in the detail is that these kind of benefits only impact in the year they are booked, and are often one-off in nature. Assuming the tax benefit is not repeated every year, we could see its profitability drop noticeably, all else being equal.

Our Take On Grove's Profit Performance

In conclusion, Grove's weak accrual ratio suggests its statutory earnings have been inflated by the non-cash tax benefit and the boost it received from unusual items. On reflection, the above-mentioned factors give us the strong impression that Grove'sunderlying earnings power is not as good as it might seem, based on the statutory profit numbers. If you want to do dive deeper into Grove, you'd also look into what risks it is currently facing. For example, Grove has 3 warning signs (and 1 which is concerning) we think you should know about.

Our examination of Grove has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqCM:UPXI

Upexi

A brand owner, engages in the development, manufacturing, and distribution of consumer products in pet, surgery, recovery, skin, beauty, health, and wellness markets.

Mediocre balance sheet low.

Market Insights

Community Narratives