- United States

- /

- Personal Products

- /

- NasdaqCM:FTLF

FitLife Brands' (NASDAQ:FTLF) Earnings Are Weaker Than They Seem

Investors were disappointed with FitLife Brands, Inc.'s (NASDAQ:FTLF) earnings, despite the strong profit numbers. We think that the market might be paying attention to some underlying factors that they find to be concerning.

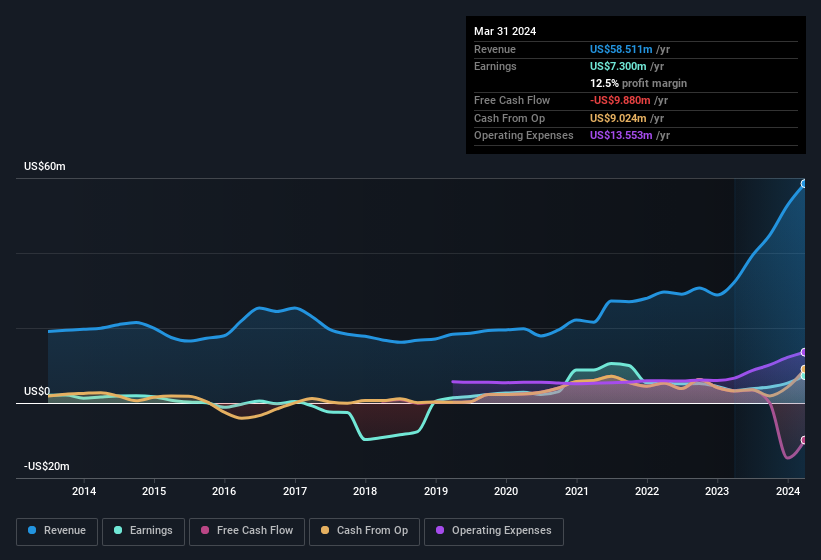

Check out our latest analysis for FitLife Brands

Zooming In On FitLife Brands' Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. This ratio tells us how much of a company's profit is not backed by free cashflow.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

Over the twelve months to March 2024, FitLife Brands recorded an accrual ratio of 0.50. As a general rule, that bodes poorly for future profitability. To wit, the company did not generate one whit of free cashflow in that time. Over the last year it actually had negative free cash flow of US$9.9m, in contrast to the aforementioned profit of US$7.30m. It's worth noting that FitLife Brands generated positive FCF of US$3.2m a year ago, so at least they've done it in the past.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of FitLife Brands.

Our Take On FitLife Brands' Profit Performance

As we discussed above, we think FitLife Brands' earnings were not supported by free cash flow, which might concern some investors. For this reason, we think that FitLife Brands' statutory profits may be a bad guide to its underlying earnings power, and might give investors an overly positive impression of the company. But the happy news is that, while acknowledging we have to look beyond the statutory numbers, those numbers are still improving, with EPS growing at a very high rate over the last year. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. So while earnings quality is important, it's equally important to consider the risks facing FitLife Brands at this point in time. When we did our research, we found 3 warning signs for FitLife Brands (1 doesn't sit too well with us!) that we believe deserve your full attention.

This note has only looked at a single factor that sheds light on the nature of FitLife Brands' profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

If you're looking to trade FitLife Brands, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:FTLF

FitLife Brands

Provides nutritional supplements for health-conscious consumers in the United States and internationally.

Solid track record with excellent balance sheet.