Advertisement

- United States

- /

- Healthcare Services

- /

- NYSE:UNH

UnitedHealth Group (NYSE:UNH) Eyes Growth with Goodwill Partnership Amidst Cybersecurity and Financial Challenges

UnitedHealth Group(NYSE:UNH) is currently experiencing significant developments that are shaping its business trajectory. Recent news highlights include a robust $14 billion revenue growth in the first half of the year and substantial investments in AI and technology, contrasted by challenges such as a recent cyberattack and foreign currency losses. In the discussion that follows, we will explore UnitedHealth Group's core strengths, critical weaknesses, growth opportunities, and key threats to provide a comprehensive overview of the company's current business situation.

Delve into the full analysis report here for a deeper understanding of UnitedHealth Group

Strengths: Core Advantages Driving Sustained Success For UnitedHealth Group

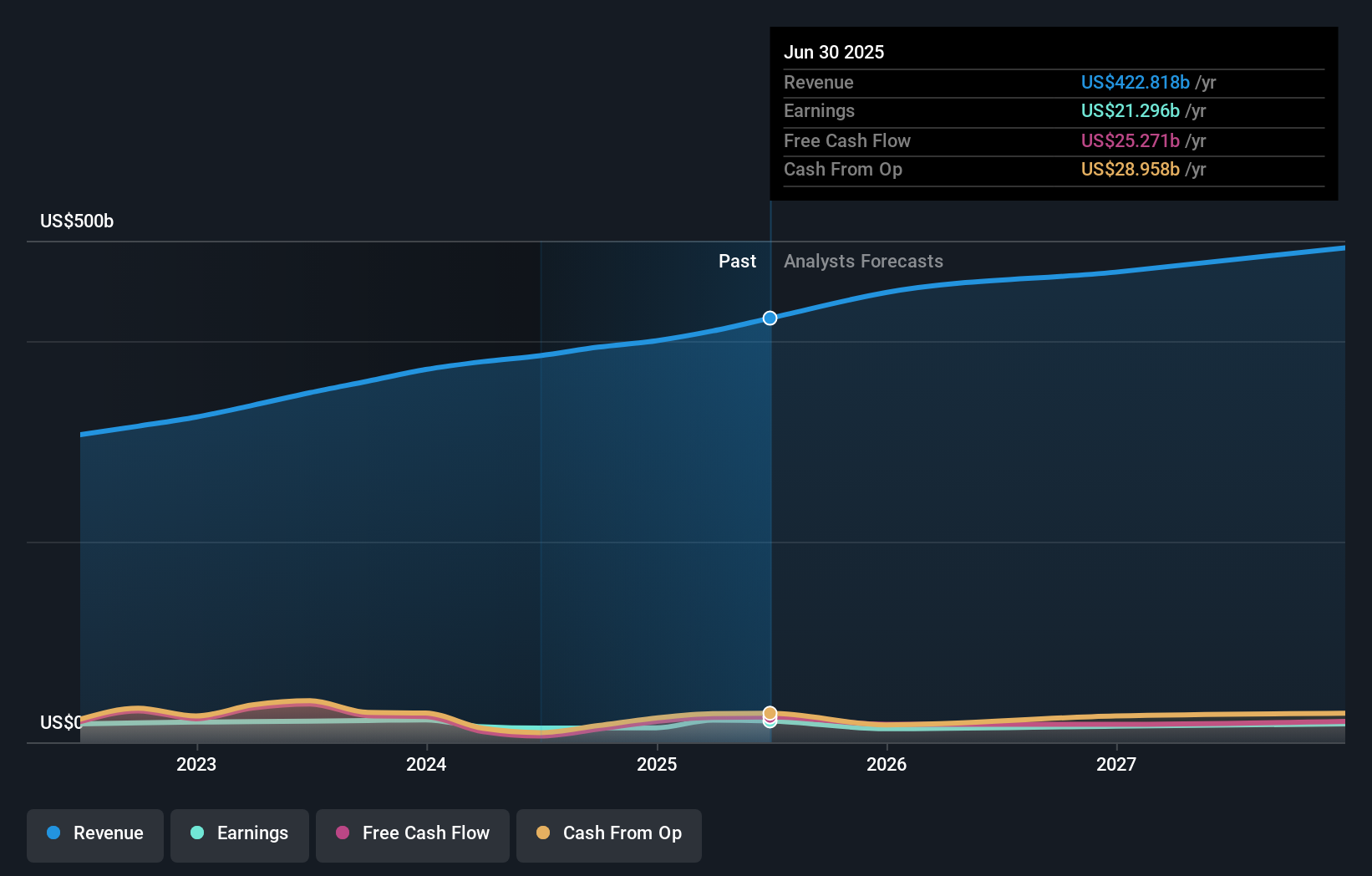

UnitedHealth Group's diversified growth strategy is a significant strength, as highlighted by CEO Andrew Witty, who noted that the company’s second-quarter results reflect durable growth and a commitment to high-quality care. This is further evidenced by a strong revenue increase, with nearly $14 billion growth in the first half of the year, driven by double-digit growth in Optum. The company's investments in AI and technology are expected to generate billions in efficiencies, enhancing operational margins, particularly in OptumHealth, which saw a 13% revenue growth to $27 billion. Additionally, the value of Medicare Advantage, which costs taxpayers 4% less than traditional Medicare, positions UnitedHealth favorably in the market.

Weaknesses: Critical Issues Affecting UnitedHealth Group's Performance and Areas For Growth

It's important to note that UNH is currently considered expensive based on its Price-To-Earnings Ratio (37.8x), significantly higher than both the US Healthcare industry average (27.7x) and the peer average (18.6x). The company faces several critical issues, including the impact of a recent cyberattack, which Witty mentioned resulted in a $0.60 to $0.70 per share business disruption. This incident also modestly affected the medical care ratio due to suspended care management activities. Foreign currency losses, particularly in South America, have also impacted financial results, with CFO John Rex reporting $1.3 billion in noncash losses. Additionally, UnitedHealth's current net profit margins (3.7%) are lower than last year’s (6.1%), reflecting some financial instability. Moreover, the company's dividend payments, although stable over the past 10 years, are not well covered by free cash flows, which could pose sustainability issues. To gain insights into how UNH's dividend policies are impacting shareholder returns, check out our in-depth analysis of the company's Dividend Strategy.

Opportunities: Potential Strategies for Leveraging Growth and Competitive Advantage

UnitedHealth Group is well-positioned for future growth, with Witty expressing optimism for 2025. The company's expansion in value-based care is on track to approach 5 million patients by the end of the year, as noted by Rex. This strategic move could enhance market positioning and capitalize on emerging opportunities. UnitedHealth's focus on innovative products and services, coupled with the use of new technologies to improve operating efficiency, further strengthens its competitive edge. Additionally, increased engagement with members, particularly high-risk ones, as highlighted by Amar Desai of OptumHealth, indicates a proactive approach to customer care. Learn more about how these opportunities could impact UnitedHealth Group's future growth by reviewing our analysis of UnitedHealth Group's Future Performance.

Threats: Key Risks and Challenges That Could Impact UnitedHealth Group's Success

UnitedHealth Group faces several external threats, including regulatory challenges related to industry premium increases dating back to 2020, which the company indicated will be reflected in future consumer premium credits. Competition in the managed care sector is also intense, with sophisticated buyers such as large employers and unions continuing to scrutinize offerings. Economic factors impacting Medicaid could affect membership levels, which are expected to stabilize in the second half of the year. Additionally, operational risks from cybersecurity remain a concern, with cyber impacts in the quarter totaling $0.92 per share and an estimated full-year impact of $1.90 to $2.05 per share. These factors could threaten the company's growth and market share, necessitating a vigilant approach to risk management.

Conclusion

UnitedHealth Group's diversified growth strategy and significant investments in AI and technology are driving substantial revenue increases and operational efficiencies, particularly in OptumHealth. However, critical issues such as the recent cyberattack, foreign currency losses, and lower net profit margins highlight the need for improved financial stability and risk management. While the company's expansion in value-based care and innovative services offers promising growth opportunities, the high Price-To-Earnings Ratio (37.8x), significantly above industry and peer averages, suggests that future performance must justify this premium to sustain investor confidence. Balancing these strengths and weaknesses will be crucial for UnitedHealth Group to navigate competitive pressures and regulatory challenges effectively.

Already own UNH? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About NYSE:UNH

UnitedHealth Group

Operates as a health care company in the United States and internationally.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor