Advertisement

- United States

- /

- Healthcare Services

- /

- NYSE:UNH

How Berkshire Hathaway’s Major Investment at UnitedHealth Group (UNH) Has Changed Its Investment Story

Simply Wall St

Reviewed by Simply Wall St

- During the past quarter, a wide array of institutional investors, including Warren Buffett’s Berkshire Hathaway, disclosed increased or new positions in UnitedHealth Group, highlighting renewed interest from prominent market participants.

- This surge in institutional activity, along with analyst and hedge fund endorsement and continued dividend commitments, underscores the company’s perceived strength despite temporary headwinds.

- We’ll examine how Berkshire Hathaway’s major new stake may influence UnitedHealth Group’s investment narrative and institutional appeal going forward.

AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

UnitedHealth Group Investment Narrative Recap

To be a shareholder in UnitedHealth Group, you need to believe in the long-term value of its diversified healthcare model and the company’s ability to manage care cost pressures, optimize Medicare operations, and adapt to regulatory changes. The recent surge in institutional buying, led by Berkshire Hathaway’s new US$1.6 billion position, reflects strong confidence but does not materially change the immediate catalyst: normalizing care activity and earnings recovery. The biggest risk remains ongoing volatility in Medicare-related costs and member profiles.

Among recent announcements, the board’s decision to maintain its quarterly dividend at US$2.21 per share stands out, underlining a commitment to shareholder returns even as operational headwinds in Medicare persist. This step signals financial resilience and may reassure investors during a period when attention is focused on execution risks related to the CMS risk model transition.

By contrast, beneath the influx of new institutional capital, it’s the interplay between accelerating care costs and shifting Medicare profiles that investors should be aware of…

Read the full narrative on UnitedHealth Group (it's free!)

UnitedHealth Group's outlook projects $501.1 billion in revenue and $20.0 billion in earnings by 2028. This scenario assumes a 5.8% annual revenue growth rate and a $1.3 billion decrease in earnings from the current $21.3 billion.

Uncover how UnitedHealth Group's forecasts yield a $327.29 fair value, a 6% upside to its current price.

Exploring Other Perspectives

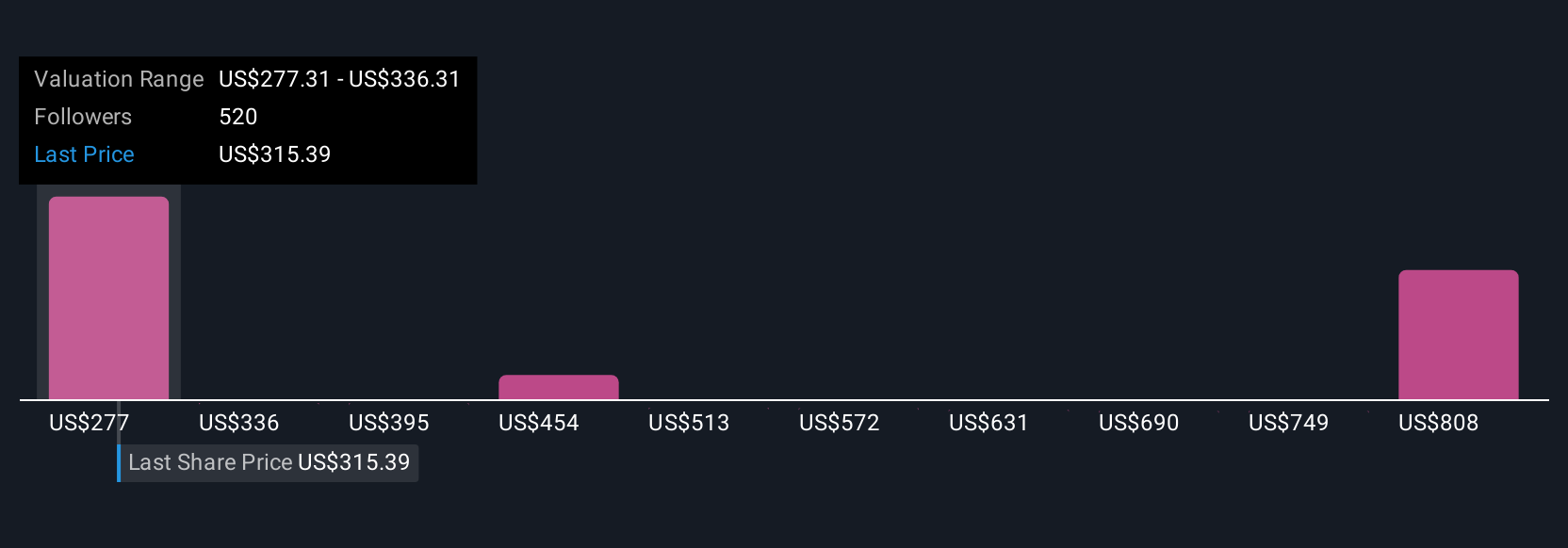

Seventy-nine members of the Simply Wall St Community estimate UnitedHealth Group’s fair value between US$290 and US$867, highlighting diverse outlooks. While many see significant upside, shifting Medicare costs remain a key variable shaping future expectations for returns and stability.

Explore 79 other fair value estimates on UnitedHealth Group - why the stock might be worth 6% less than the current price!

Build Your Own UnitedHealth Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your UnitedHealth Group research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free UnitedHealth Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate UnitedHealth Group's overall financial health at a glance.

Contemplating Other Strategies?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- Find companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are the new gold rush. Find out which 29 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:UNH

UnitedHealth Group

Operates as a health care company in the United States and internationally.

Outstanding track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|74.9% undervalued

JO

Community Contributor

PayPal's Future Growth Through Venmo and Merchant Solutions

Fair Value US$105.25|35.1% undervalued

ZW

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$26.54|1.5% undervalued

BL

Community Contributor