- United States

- /

- Medical Equipment

- /

- NYSE:PEN

Penumbra, Inc.'s (NYSE:PEN) Earnings Haven't Escaped The Attention Of Investors

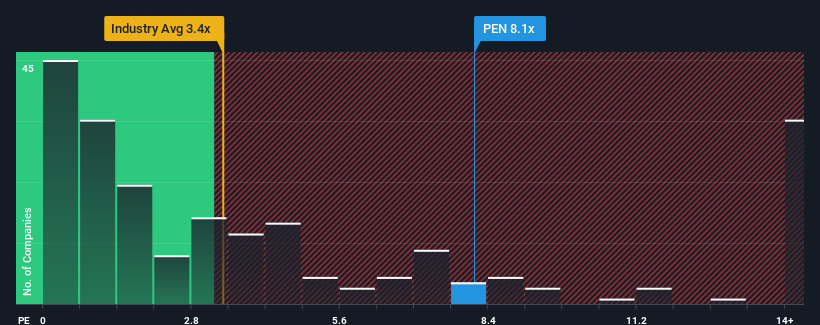

Penumbra, Inc.'s (NYSE:PEN) price-to-sales (or "P/S") ratio of 8.1x might make it look like a strong sell right now compared to the Medical Equipment industry in the United States, where around half of the companies have P/S ratios below 3.4x and even P/S below 1.3x are quite common. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Penumbra

How Penumbra Has Been Performing

Recent times have been advantageous for Penumbra as its revenues have been rising faster than most other companies. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. If not, then existing shareholders might be a little nervous about the viability of the share price.

Keen to find out how analysts think Penumbra's future stacks up against the industry? In that case, our free report is a great place to start.How Is Penumbra's Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Penumbra's to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 25% last year. Pleasingly, revenue has also lifted 89% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

Shifting to the future, estimates from the analysts covering the company suggest revenue should grow by 17% per year over the next three years. With the industry only predicted to deliver 10% per annum, the company is positioned for a stronger revenue result.

With this in mind, it's not hard to understand why Penumbra's P/S is high relative to its industry peers. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our look into Penumbra shows that its P/S ratio remains high on the merit of its strong future revenues. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

The company's balance sheet is another key area for risk analysis. Our free balance sheet analysis for Penumbra with six simple checks will allow you to discover any risks that could be an issue.

If you're unsure about the strength of Penumbra's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:PEN

Penumbra

Designs, develops, manufactures, and markets medical devices in the United States and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives