Advertisement

- United States

- /

- Healthcare Services

- /

- NYSE:COR

Can Analyst Upgrades Reveal New Strengths in Cencora's (COR) Competitive Positioning?

Simply Wall St

Reviewed by Sasha Jovanovic

- In recent days, Evercore ISI added Cencora to its "Tactical Outperform" list ahead of the third-quarter earnings season, while analysts revised earnings estimates upwards for the company.

- This heightened analyst optimism reflects growing confidence in Cencora’s value proposition and anticipated earnings growth within the U.S. pharmaceutical distribution sector.

- We'll explore how increased analyst coverage and upward earnings estimate revisions may influence Cencora's forward-looking investment narrative.

Find companies with promising cash flow potential yet trading below their fair value.

Cencora Investment Narrative Recap

To believe in Cencora as a shareholder, you need to have confidence in the company’s leadership in pharmaceutical distribution and its ability to capture growth from rising demand for specialty drugs and healthcare solutions. Recent analyst optimism, including upward revisions to earnings estimates and the Evercore ISI “Tactical Outperform” call, may boost sentiment ahead of third-quarter results, though these moves alone do not materially shift the main short-term catalyst: execution in high-margin specialty services. The biggest risk remains pressure on margins from increasing biosimilar and generic adoption, and this risk has not fundamentally changed as a result of the news.

Among recent announcements, Cencora’s revised 2025 revenue growth outlook (from a previous 7% to a new range of 8% to 10%) aligns with the analyst confidence seen in the latest coverage. While this points to management’s positive expectations, actual margin improvement will depend on Cencora’s ability to sustain growth in specialty distribution and value-added services, which are key to mitigating margin compression risks.

However, investors should also consider the ongoing risks posed by shrinking fees from generics and biosimilars...

Read the full narrative on Cencora (it's free!)

Cencora's narrative projects $385.4 billion in revenue and $3.3 billion in earnings by 2028. This requires 6.8% yearly revenue growth and an earnings increase of $1.4 billion from $1.9 billion today.

Uncover how Cencora's forecasts yield a $333.29 fair value, a 5% upside to its current price.

Exploring Other Perspectives

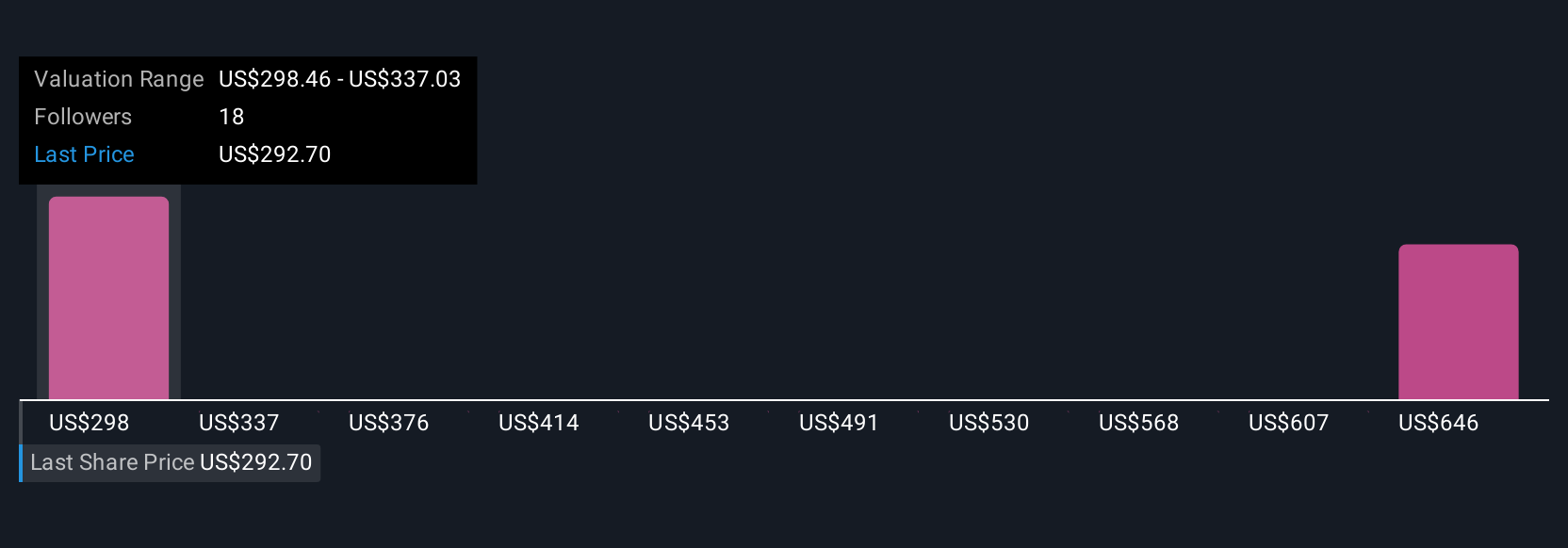

Four different fair value estimates from the Simply Wall St Community span from US$298.46 to US$679.79 per share. As you review these diverse viewpoints, keep in mind that despite optimism around revenue growth, pressure from lower-margin products can shape the company’s future earnings potential.

Explore 4 other fair value estimates on Cencora - why the stock might be worth over 2x more than the current price!

Build Your Own Cencora Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cencora research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Cencora research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cencora's overall financial health at a glance.

Contemplating Other Strategies?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:COR

Cencora

Cencora, Inc. sources and distributes pharmaceutical products in the United States and internationally.

Mediocre balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|37.6% undervalued

TR

Community Contributor