Something has clearly shifted for Concentra Group Holdings Parent (NYSE:CON), and investors are taking notice. Over the past week, two major investment banks, JPMorgan and Truist, stepped up their endorsements for the company, citing not just the successful acquisition of Pivot On-site Health Clinics but also Concentra’s strong competitive footing in outpatient healthcare. The acquisition doubled the size of Concentra’s on-site health clinic segment, and the firm quickly responded by raising its revenue guidance for next year. For those tracking the stock, these events provide tangible reasons to consider whether Concentra is entering a new growth phase.

Looking at the numbers, Concentra’s shares gained a modest 1% in the past day but slipped around 1.7% over the past week and about 12% for the month. On a year-to-date basis, though, the stock is still up by 8%. Over the full year, shares are down by nearly 9%, suggesting that while momentum picked up with this recent news, longer-term sentiment has been lukewarm. The pivot in analyst coverage and higher guidance could be the jolt needed for renewed interest.

So is this recent string of analyst confidence and strategic growth enough to justify jumping in now, or is the market already anticipating the next level of results from Concentra?

Advertisement

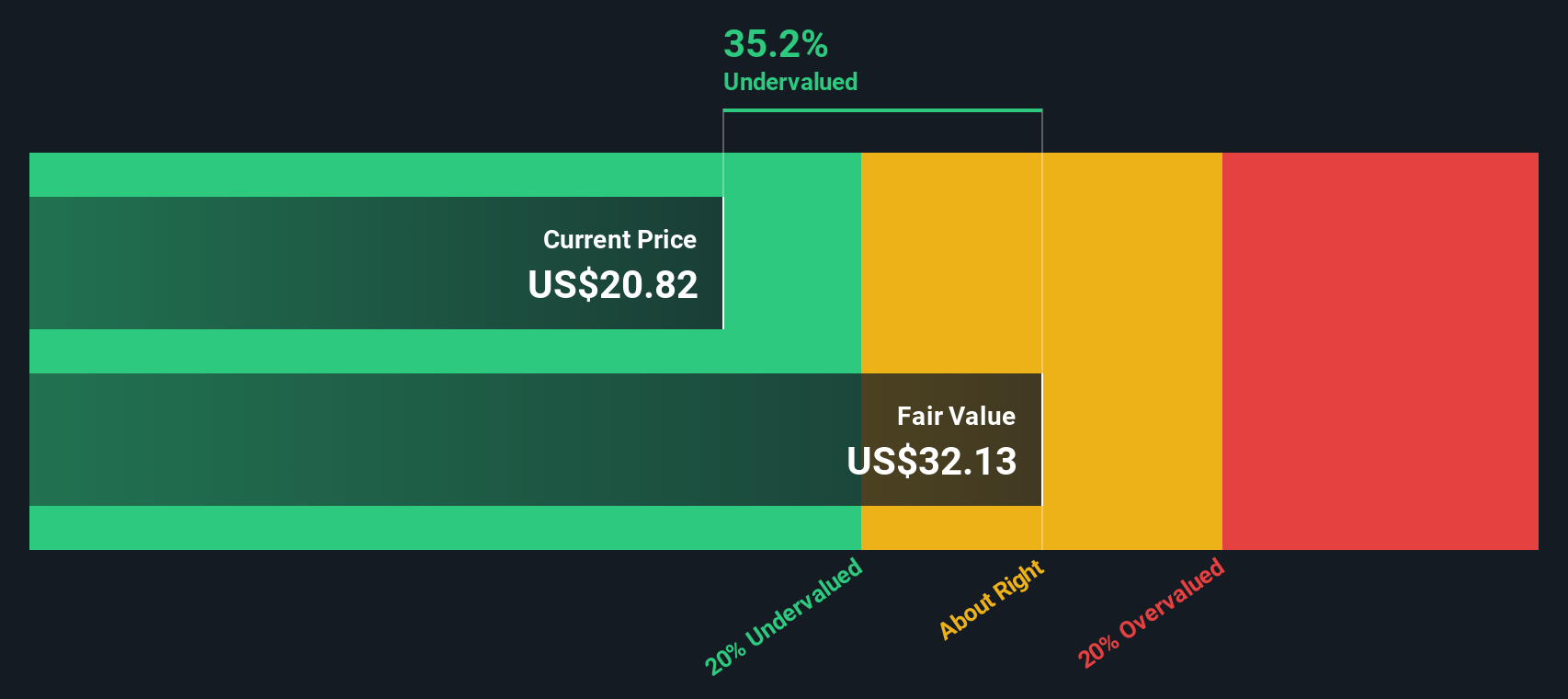

Most Popular Narrative: 25.8% Undervalued

According to the most widely followed narrative, Concentra Group Holdings Parent could be significantly undervalued, with a fair value estimate that is over 25% higher than its current share price. This assessment factors in the company's expected earnings growth, margin improvements, and a discount rate aligned with industry standards.

Strategic acquisitions (Nova and Pivot) and de novo clinic expansion are actively increasing Concentra's national footprint and service capabilities, providing revenue growth through increased volumes and operational leverage. Full integration and synergy realization are expected to further improve EBITDA margins and overall earnings in coming quarters.

Curious about the engine behind this bullish outlook? The analysts are betting big on Concentra’s ability to boost growth, sharpen margins, and bank on multiple expansion. One critical and perhaps surprising assumption lies at the heart of this valuation. Want to see what powers this number?

However, persistent high integration costs or a slowdown in core occupational health demand could quickly change this outlook and temper analyst optimism.

A different lens on valuation comes from applying our SWS DCF model. This approach, which looks at Concentra's forecasted future cash flows, also points to the stock being undervalued at current levels. Does this second method make the case even stronger, or is there something both models could be missing?

Build Your Own Concentra Group Holdings Parent Narrative

If you have a different take on these figures or prefer to analyze the numbers yourself, you can build your own view of Concentra in just a few minutes. Do it your way.

A great starting point for your Concentra Group Holdings Parent research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Angles?

Stay ahead of the curve by tapping into high-potential stock themes. Don’t let opportunities pass by, when tomorrow’s market leaders could be waiting for you right now.

Seize the chance to uncover resilient value with undervalued stocks based on cash flows and see which companies are priced well below their intrinsic worth.

Spot top-tier cash flow from proven business models with dividend stocks with yields > 3% and find income opportunities yielding over 3% in today’s market.

Tap into the future of healthcare by browsing healthcare AI stocks for innovative companies transforming patient care through artificial intelligence.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies