- United States

- /

- Healthcare Services

- /

- NasdaqGS:PDCO

Patterson Companies, Inc. (NASDAQ:PDCO) Doing What It Can To Lift Shares

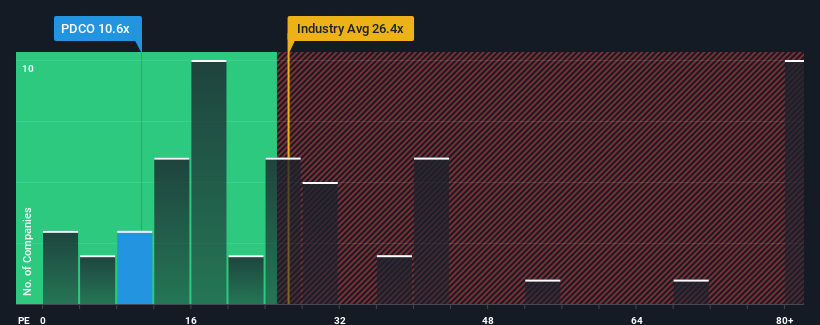

Patterson Companies, Inc.'s (NASDAQ:PDCO) price-to-earnings (or "P/E") ratio of 10.6x might make it look like a buy right now compared to the market in the United States, where around half of the companies have P/E ratios above 17x and even P/E's above 32x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Recent times have been pleasing for Patterson Companies as its earnings have risen in spite of the market's earnings going into reverse. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Patterson Companies

How Is Patterson Companies' Growth Trending?

The only time you'd be truly comfortable seeing a P/E as low as Patterson Companies' is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered virtually the same number to the company's bottom line as the year before. Likewise, not much has changed from three years ago as earnings have been stuck during that whole time. Accordingly, shareholders probably wouldn't have been satisfied with the complete absence of medium-term growth.

Looking ahead now, EPS is anticipated to climb by 8.0% per annum during the coming three years according to the twelve analysts following the company. That's shaping up to be similar to the 10% per annum growth forecast for the broader market.

With this information, we find it odd that Patterson Companies is trading at a P/E lower than the market. It may be that most investors are not convinced the company can achieve future growth expectations.

What We Can Learn From Patterson Companies' P/E?

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Patterson Companies' analyst forecasts revealed that its market-matching earnings outlook isn't contributing to its P/E as much as we would have predicted. There could be some unobserved threats to earnings preventing the P/E ratio from matching the outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide more support to the share price.

Having said that, be aware Patterson Companies is showing 3 warning signs in our investment analysis, and 2 of those are potentially serious.

Of course, you might also be able to find a better stock than Patterson Companies. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:PDCO

Patterson Companies

Engages in the distribution of dental and animal health products in the United States, the United Kingdom, and Canada.

Undervalued average dividend payer.