- United States

- /

- Healthcare Services

- /

- NasdaqGS:OPCH

With EPS Growth And More, Option Care Health (NASDAQ:OPCH) Makes An Interesting Case

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Option Care Health (NASDAQ:OPCH). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Option Care Health with the means to add long-term value to shareholders.

View our latest analysis for Option Care Health

How Fast Is Option Care Health Growing Its Earnings Per Share?

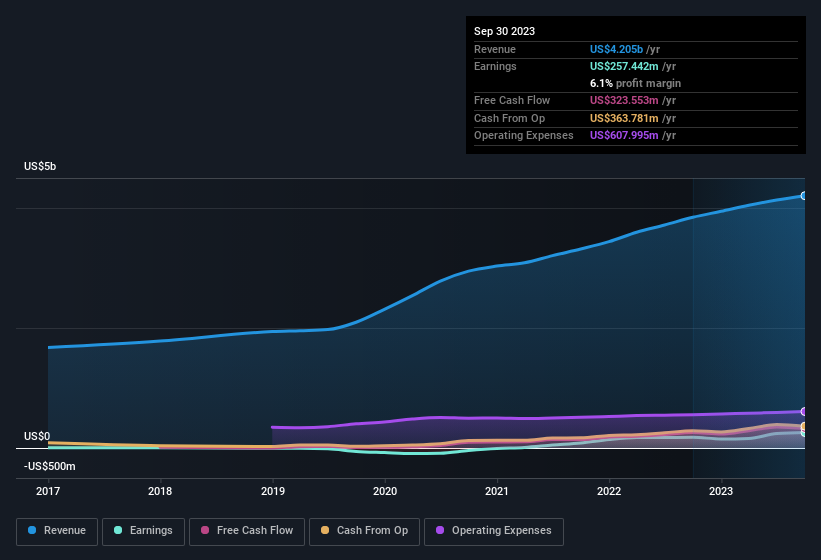

Over the last three years, Option Care Health has grown earnings per share (EPS) at as impressive rate from a relatively low point, resulting in a three year percentage growth rate that isn't particularly indicative of expected future performance. So it would be better to isolate the growth rate over the last year for our analysis. To the delight of shareholders, Option Care Health's EPS soared from US$0.99 to US$1.45, over the last year. That's a commendable gain of 47%.

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. While we note Option Care Health achieved similar EBIT margins to last year, revenue grew by a solid 9.4% to US$4.2b. That's encouraging news for the company!

In the chart below, you can see how the company has grown earnings and revenue, over time. To see the actual numbers, click on the chart.

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for Option Care Health's future profits.

Are Option Care Health Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

The US$49k worth of shares that insiders sold during the last 12 months pales in comparison to the US$2.1m they spent on acquiring shares in the company. This adds to the interest in Option Care Health because it suggests that those who understand the company best, are optimistic. It is also worth noting that it was Independent Non Executive Chairman of the Board Harry M. Kraemer who made the biggest single purchase, worth US$1.9m, paying US$34.63 per share.

On top of the insider buying, it's good to see that Option Care Health insiders have a valuable investment in the business. To be specific, they have US$22m worth of shares. That's a lot of money, and no small incentive to work hard. Even though that's only about 0.4% of the company, it's enough money to indicate alignment between the leaders of the business and ordinary shareholders.

While insiders already own a significant amount of shares, and they have been buying more, the good news for ordinary shareholders does not stop there. That's because Option Care Health's CEO, John Rademacher, is paid at a relatively modest level when compared to other CEOs for companies of this size. For companies with market capitalisations between US$4.0b and US$12b, like Option Care Health, the median CEO pay is around US$8.2m.

The Option Care Health CEO received US$6.8m in compensation for the year ending December 2022. That comes in below the average for similar sized companies and seems pretty reasonable. While the level of CEO compensation shouldn't be the biggest factor in how the company is viewed, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. It can also be a sign of good governance, more generally.

Does Option Care Health Deserve A Spot On Your Watchlist?

For growth investors, Option Care Health's raw rate of earnings growth is a beacon in the night. Furthermore, company insiders have been adding to their significant stake in the company. So it's fair to say that this stock may well deserve a spot on your watchlist. Even so, be aware that Option Care Health is showing 3 warning signs in our investment analysis , and 1 of those is a bit unpleasant...

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Option Care Health, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you're looking to trade Option Care Health, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:OPCH

Option Care Health

Offers home and alternate site infusion services in the United States.

Excellent balance sheet and fair value.