- United States

- /

- Medical Equipment

- /

- NasdaqGS:OMCL

Taking Stock of Omnicell (OMCL) After Titan XT Launch: What the New Platform Means for Valuation

Reviewed by Simply Wall St

Omnicell (OMCL) just rolled out Titan XT, an enterprise grade automated dispensing platform tightly integrated with its OmniSphere cloud, and investors are already asking what this means for growth and the stock.

See our latest analysis for Omnicell.

The launch of Titan XT lands after a strong run in the shares, with a 30 day share price return of roughly 25 percent and a 90 day gain of about 36 percent. This comes even though the 1 year total shareholder return remains slightly negative, which suggests momentum is building as investors reassess Omnicell’s longer term prospects.

If this kind of product driven story appeals to you, it could be a good moment to see what other healthcare names are setting up interestingly via healthcare stocks.

Yet with the shares still trading at a modest discount to analyst targets after years of underperformance, investors now have to decide whether Omnicell is finally mispriced on the upside or if the market is only beginning to factor in Titan driven growth.

Most Popular Narrative: 7.3% Undervalued

With Omnicell last closing at $43.86 versus a narrative fair value near $47.33, the prevailing view leans modestly optimistic on upside potential.

The analysts have a consensus price target of $44.0 for Omnicell based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $55.0, and the most bearish reporting a price target of just $34.0.

Want to know what kind of steady growth, margin lift, and premium earnings multiple could justify that valuation gap? The real story sits in those long range projections and how they compound over time. Curious which assumptions have to hold for that upside to stick? Dive in to unpack the full narrative behind these numbers.

Result: Fair Value of $47.33 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside still hinges on navigating tariff driven cost pressures and potential slowdowns in hospital capital spending, which could crimp Omnicell’s growth trajectory.

Find out about the key risks to this Omnicell narrative.

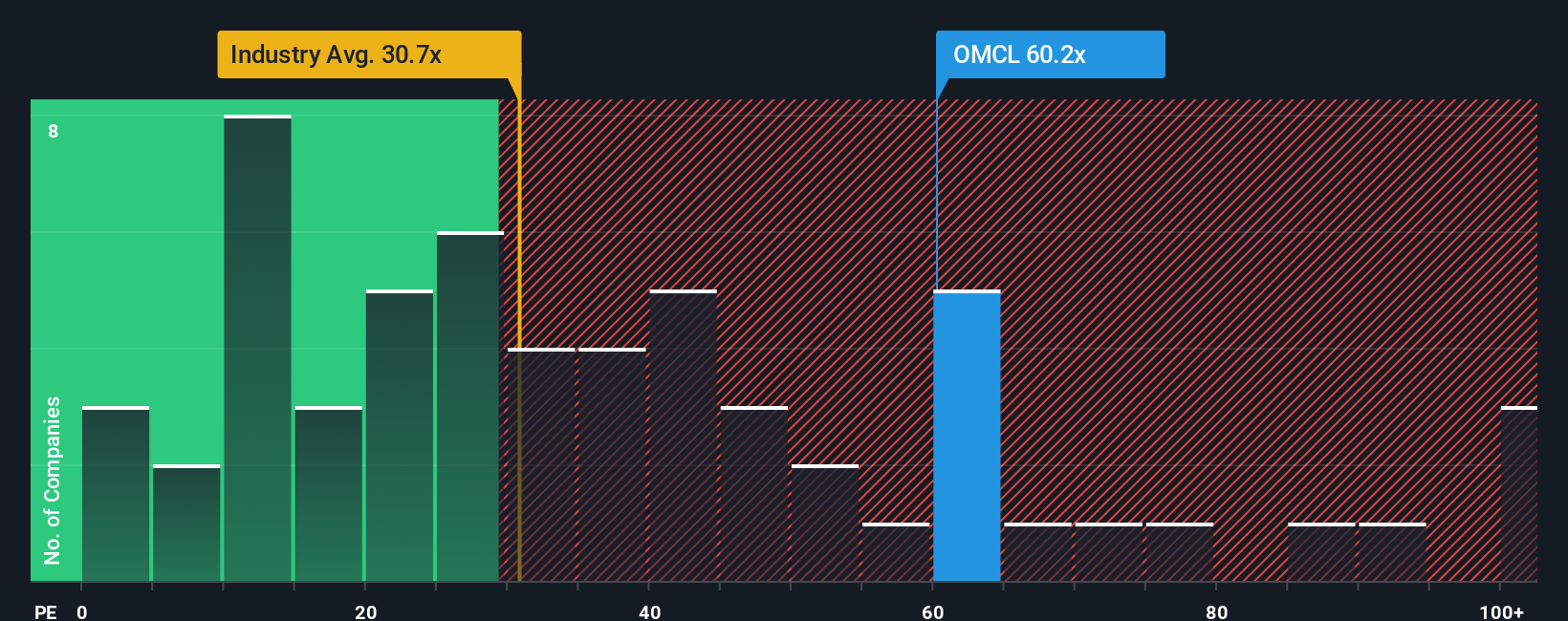

Another Angle on Valuation

On earnings, the picture looks very different. Omnicell trades on a steep 98.8x price to earnings ratio, versus about 30.4x for the US medical equipment industry and a fair ratio of 34.6x. This points to meaningful valuation risk if sentiment cools or growth underdelivers.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Omnicell Narrative

If these conclusions do not fully align with your view, or you prefer hands on research, you can build a custom narrative in just minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Omnicell.

Ready for your next investing move?

Before you move on, seize the chance to uncover fresh stock ideas in minutes using targeted screeners on Simply Wall St that many investors overlook.

- Capture potential mispricings by running through these 908 undervalued stocks based on cash flows that currently trade below what their cash flows suggest they are worth.

- Ride long term innovation trends by scanning these 26 AI penny stocks that are building real businesses around artificial intelligence.

- Strengthen your income stream by checking these 13 dividend stocks with yields > 3% that could help support portfolio yield without sacrificing quality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:OMCL

Omnicell

Provides medication management solutions and adherence tools for healthcare systems and pharmacies the United States and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)