Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:OMCL

It Looks Like Omnicell, Inc.'s (NASDAQ:OMCL) CEO May Expect Their Salary To Be Put Under The Microscope

Key Insights

- Omnicell's Annual General Meeting to take place on 21st of May

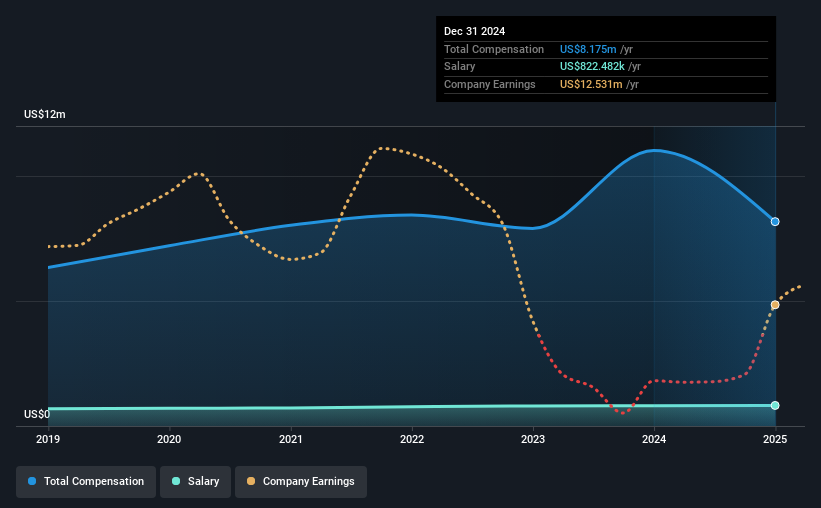

- CEO Randy Lipps' total compensation includes salary of US$822.5k

- The overall pay is comparable to the industry average

- Omnicell's EPS declined by 35% over the past three years while total shareholder loss over the past three years was 75%

Shareholders will probably not be too impressed with the underwhelming results at Omnicell, Inc. (NASDAQ:OMCL) recently. Shareholders will be interested in what the board will have to say about turning performance around at the next AGM on 21st of May. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. We present the case why we think CEO compensation is out of sync with company performance.

View our latest analysis for Omnicell

How Does Total Compensation For Randy Lipps Compare With Other Companies In The Industry?

At the time of writing, our data shows that Omnicell, Inc. has a market capitalization of US$1.3b, and reported total annual CEO compensation of US$8.2m for the year to December 2024. Notably, that's a decrease of 26% over the year before. We think total compensation is more important but our data shows that the CEO salary is lower, at US$822k.

For comparison, other companies in the American Medical Equipment industry with market capitalizations ranging between US$1.0b and US$3.2b had a median total CEO compensation of US$6.5m. From this we gather that Randy Lipps is paid around the median for CEOs in the industry. What's more, Randy Lipps holds US$12m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | US$822k | US$813k | 10% |

| Other | US$7.4m | US$10m | 90% |

| Total Compensation | US$8.2m | US$11m | 100% |

On an industry level, around 25% of total compensation represents salary and 75% is other remuneration. In Omnicell's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

Omnicell, Inc.'s Growth

Omnicell, Inc. has reduced its earnings per share by 35% a year over the last three years. In the last year, its revenue is up 3.0%.

Few shareholders would be pleased to read that EPS have declined. The modest increase in revenue in the last year isn't enough to make us overlook the disappointing change in EPS. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Omnicell, Inc. Been A Good Investment?

With a total shareholder return of -75% over three years, Omnicell, Inc. shareholders would by and large be disappointed. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

Not only have shareholders not seen a favorable return on their investment, but the business hasn't performed well either. Few shareholders would be willing to award the CEO with a pay raise. At the upcoming AGM, they can question the management's plans and strategies to turn performance around and reassess their investment thesis in regards to the company.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. We did our research and spotted 1 warning sign for Omnicell that investors should look into moving forward.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:OMCL

Omnicell

Provides medication management solutions and adherence tools for healthcare systems and pharmacies the United States and internationally.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor