- United States

- /

- Healthcare Services

- /

- NasdaqCM:NEO

NeoGenomics (NASDAQ:NEO) investors are sitting on a loss of 69% if they invested three years ago

While it may not be enough for some shareholders, we think it is good to see the NeoGenomics, Inc. (NASDAQ:NEO) share price up 17% in a single quarter. But that doesn't change the fact that the returns over the last three years have been disappointing. Regrettably, the share price slid 69% in that period. So it's good to see it climbing back up. While many would remain nervous, there could be further gains if the business can put its best foot forward.

It's worthwhile assessing if the company's economics have been moving in lockstep with these underwhelming shareholder returns, or if there is some disparity between the two. So let's do just that.

View our latest analysis for NeoGenomics

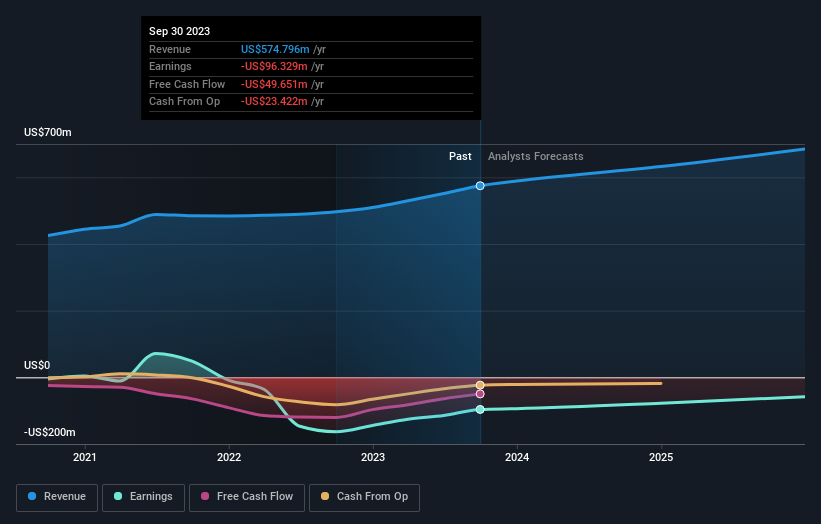

NeoGenomics isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

Over three years, NeoGenomics grew revenue at 8.1% per year. That's a fairly respectable growth rate. So some shareholders would be frustrated with the compound loss of 19% per year. The market must have had really high expectations to be disappointed with this progress. So this is one stock that might be worth investigating further, or even adding to your watchlist.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

NeoGenomics is well known by investors, and plenty of clever analysts have tried to predict the future profit levels. You can see what analysts are predicting for NeoGenomics in this interactive graph of future profit estimates.

A Different Perspective

It's good to see that NeoGenomics has rewarded shareholders with a total shareholder return of 45% in the last twelve months. There's no doubt those recent returns are much better than the TSR loss of 0.2% per year over five years. We generally put more weight on the long term performance over the short term, but the recent improvement could hint at a (positive) inflection point within the business. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. To that end, you should be aware of the 1 warning sign we've spotted with NeoGenomics .

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Valuation is complex, but we're here to simplify it.

Discover if NeoGenomics might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:NEO

NeoGenomics

Operates a network of cancer-focused testing laboratories in the United States and the United Kingdom.

Adequate balance sheet and slightly overvalued.