Advertisement

- United States

- /

- Healthtech

- /

- NasdaqGM:CCLD

The Market Doesn't Like What It Sees From CareCloud, Inc.'s (NASDAQ:CCLD) Revenues Yet As Shares Tumble 27%

CareCloud, Inc. (NASDAQ:CCLD) shareholders that were waiting for something to happen have been dealt a blow with a 27% share price drop in the last month. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 65% loss during that time.

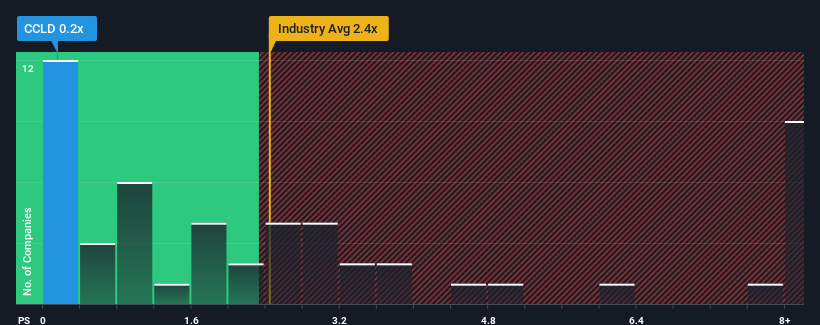

Since its price has dipped substantially, considering about half the companies operating in the United States' Healthcare Services industry have price-to-sales ratios (or "P/S") above 2.4x, you may consider CareCloud as an great investment opportunity with its 0.2x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

Check out our latest analysis for CareCloud

How CareCloud Has Been Performing

CareCloud could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. The P/S ratio is probably low because investors think this poor revenue performance isn't going to get any better. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on CareCloud.Is There Any Revenue Growth Forecasted For CareCloud?

CareCloud's P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 16%. This has soured the latest three-year period, which nevertheless managed to deliver a decent 11% overall rise in revenue. So we can start by confirming that the company has generally done a good job of growing revenue over that time, even though it had some hiccups along the way.

Turning to the outlook, the next year should generate growth of 5.4% as estimated by the four analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 13%, which is noticeably more attractive.

With this in consideration, its clear as to why CareCloud's P/S is falling short industry peers. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

CareCloud's P/S looks about as weak as its stock price lately. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As expected, our analysis of CareCloud's analyst forecasts confirms that the company's underwhelming revenue outlook is a major contributor to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 4 warning signs for CareCloud you should know about.

If these risks are making you reconsider your opinion on CareCloud, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:CCLD

CareCloud

A healthcare information technology (IT) company, provides technology-enabled business solutions, Software-as-a-Service offerings, and related business services to healthcare providers and hospitals primarily in the United States.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor