- United States

- /

- Food

- /

- NYSE:HSY

Hershey (NYSE:HSY) Unveils Reese's PB&J Big Cups Available Nationwide

Reviewed by Simply Wall St

In the past week, Hershey (NYSE:HSY) launched the Reese's PB&J Big Cups nationwide, potentially boosting consumer interest with its limited-time offer. This product launch coincided with a tumultuous overall market, which declined by 3% as investors braced for President Trump's possible new tariffs impacting economic trends. Despite these broader market challenges, Hershey's share price increased by 2.66%, possibly reflecting positive investor sentiment around the new product and its potential impact on sales. While macroeconomic factors, such as tariff uncertainties, weighed heavily on many stocks, Hershey's performance seemed unscathed by the broader market's volatility.

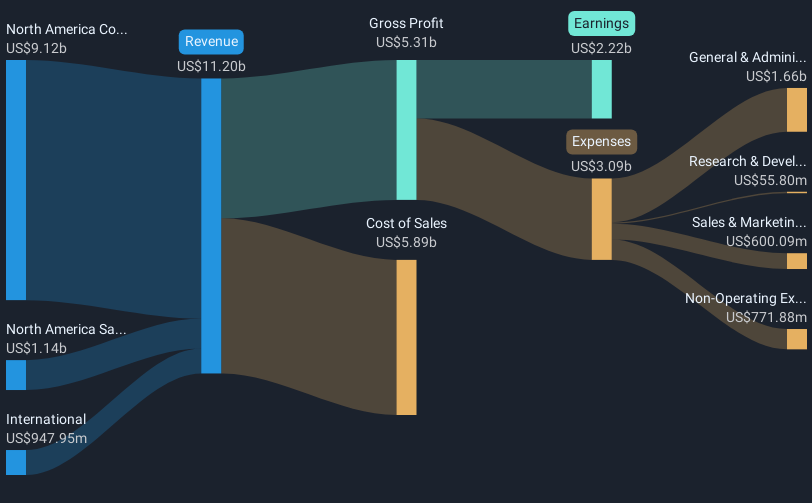

Over the last five years, Hershey's total shareholder return, including share price and dividends, increased by 34.45%. Key factors influencing this performance include strong earnings results, like the Q4 2024 sales surge to US$2.89 billion and an impressive net income rise to US$796.59 million. The company's high dividend reliability, marked by its 380th consecutive payment, showcases steady shareholder value commitment. Significant product developments, such as the limited-time Reese's PB&J Big Cups and new Easter lines, likely enhanced consumer interest, supporting sales growth. Additionally, corporate transitions, especially with fresh executive appointments in key growth roles, have been crucial in aligning Hershey’s strategies with evolving market demands.

Despite outperforming the broader US food industry over one year, Hershey's performance was more muted versus the overall market growth of 7.5%. However, the company's robust previous earnings growth of 19.3% year over year illustrates its strong market positioning, despite high cocoa costs and expanded consumer demand for healthier options possibly posing challenges ahead.

Our valuation report here indicates Hershey may be undervalued.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Hershey, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Hershey might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HSY

Hershey

Engages in the manufacture and sale of confectionery products and pantry items in the United States and internationally.

Solid track record established dividend payer.

Similar Companies

Market Insights

Community Narratives