- United States

- /

- Food

- /

- NasdaqGS:OTLY

Further Upside For Oatly Group AB (NASDAQ:OTLY) Shares Could Introduce Price Risks After 73% Bounce

Oatly Group AB (NASDAQ:OTLY) shareholders would be excited to see that the share price has had a great month, posting a 73% gain and recovering from prior weakness. But the gains over the last month weren't enough to make shareholders whole, as the share price is still down 6.4% in the last twelve months.

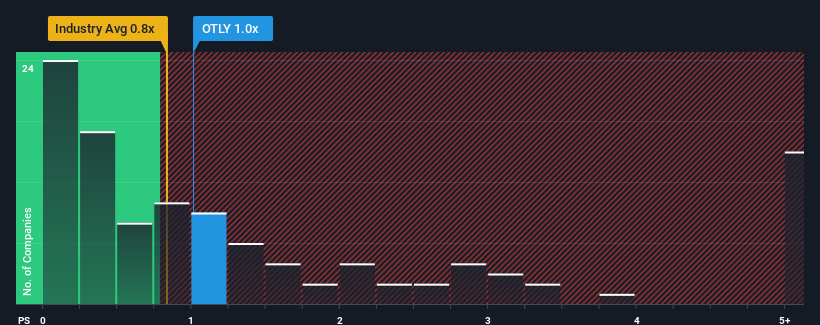

In spite of the firm bounce in price, it's still not a stretch to say that Oatly Group's price-to-sales (or "P/S") ratio of 1x right now seems quite "middle-of-the-road" compared to the Food industry in the United States, where the median P/S ratio is around 0.8x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

Check out our latest analysis for Oatly Group

What Does Oatly Group's Recent Performance Look Like?

Recent revenue growth for Oatly Group has been in line with the industry. The P/S ratio is probably moderate because investors think this modest revenue performance will continue. If this is the case, then at least existing shareholders won't be losing sleep over the current share price.

Want the full picture on analyst estimates for the company? Then our free report on Oatly Group will help you uncover what's on the horizon.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Oatly Group's to be considered reasonable.

Retrospectively, the last year delivered a decent 8.6% gain to the company's revenues. The latest three year period has also seen an excellent 84% overall rise in revenue, aided somewhat by its short-term performance. So we can start by confirming that the company has done a great job of growing revenues over that time.

Looking ahead now, revenue is anticipated to climb by 6.9% per annum during the coming three years according to the seven analysts following the company. With the industry only predicted to deliver 3.1% per annum, the company is positioned for a stronger revenue result.

With this in consideration, we find it intriguing that Oatly Group's P/S is closely matching its industry peers. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Final Word

Oatly Group appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Oatly Group currently trades on a lower than expected P/S since its forecasted revenue growth is higher than the wider industry. There could be some risks that the market is pricing in, which is preventing the P/S ratio from matching the positive outlook. This uncertainty seems to be reflected in the share price which, while stable, could be higher given the revenue forecasts.

Having said that, be aware Oatly Group is showing 3 warning signs in our investment analysis, and 1 of those is significant.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:OTLY

Oatly Group

An oatmilk company, provides a range of plant-based dairy products made from oats in Europe, the Middle East, Africa, the Americas, and Asia.

Fair value low.

Similar Companies

Market Insights

Community Narratives