Advertisement

- United States

- /

- Energy Services

- /

- NYSE:WTTR

Is Select Water Solutions, Inc.'s (NYSE:WTTR) Recent Stock Performance Influenced By Its Fundamentals In Any Way?

Most readers would already be aware that Select Water Solutions' (NYSE:WTTR) stock increased significantly by 14% over the past three months. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to study its financial indicators more closely to see if they had a hand to play in the recent price move. In this article, we decided to focus on Select Water Solutions' ROE.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. Put another way, it reveals the company's success at turning shareholder investments into profits.

Check out our latest analysis for Select Water Solutions

How Is ROE Calculated?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Select Water Solutions is:

7.1% = US$65m ÷ US$919m (Based on the trailing twelve months to September 2024).

The 'return' is the yearly profit. Another way to think of that is that for every $1 worth of equity, the company was able to earn $0.07 in profit.

What Is The Relationship Between ROE And Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

A Side By Side comparison of Select Water Solutions' Earnings Growth And 7.1% ROE

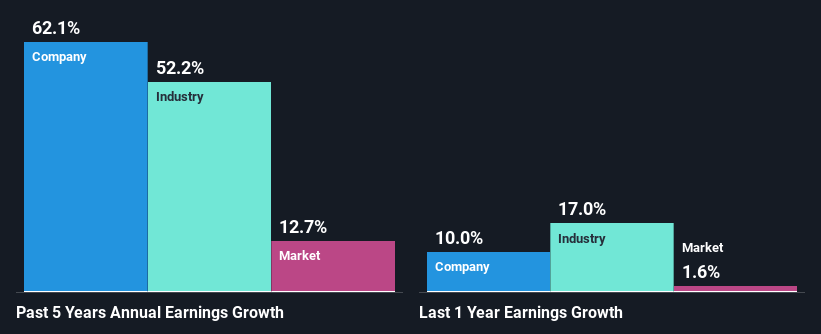

When you first look at it, Select Water Solutions' ROE doesn't look that attractive. Next, when compared to the average industry ROE of 14%, the company's ROE leaves us feeling even less enthusiastic. However, we we're pleasantly surprised to see that Select Water Solutions grew its net income at a significant rate of 62% in the last five years. Therefore, there could be other reasons behind this growth. For example, it is possible that the company's management has made some good strategic decisions, or that the company has a low payout ratio.

Next, on comparing Select Water Solutions' net income growth with the industry, we found that the company's reported growth is similar to the industry average growth rate of 53% over the last few years.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. What is WTTR worth today? The intrinsic value infographic in our free research report helps visualize whether WTTR is currently mispriced by the market.

Is Select Water Solutions Efficiently Re-investing Its Profits?

Select Water Solutions has a three-year median payout ratio of 33% (where it is retaining 67% of its income) which is not too low or not too high. So it seems that Select Water Solutions is reinvesting efficiently in a way that it sees impressive growth in its earnings (discussed above) and pays a dividend that's well covered.

While Select Water Solutions has been growing its earnings, it only recently started to pay dividends which likely means that the company decided to impress new and existing shareholders with a dividend. Our latest analyst data shows that the future payout ratio of the company is expected to drop to 16% over the next three years. Accordingly, the expected drop in the payout ratio explains the expected increase in the company's ROE to 16%, over the same period.

Summary

In total, it does look like Select Water Solutions has some positive aspects to its business. Even in spite of the low rate of return, the company has posted impressive earnings growth as a result of reinvesting heavily into its business. We also studied the latest analyst forecasts and found that the company's earnings growth is expected be similar to its current growth rate. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:WTTR

Select Water Solutions

Provides water management and chemical solutions to the energy industry in the United States.

Excellent balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor