- United States

- /

- Oil and Gas

- /

- NYSE:INSW

Is It Too Late To Consider International Seaways After Its 350% Five Year Surge?

Reviewed by Bailey Pemberton

- If you are wondering whether International Seaways is still a smart buy after its big multiyear run, or if most of the upside is already priced in, this article will walk through whether the current share price looks compelling or stretched.

- Even after a recent pullback of 5.0% over the last week and 10.1% over the past month, the stock is still up 33.9% year to date and 49.0% over the last year, with a 350.1% gain over five years that naturally raises questions about future returns and risk.

- Those moves sit against a backdrop of tight global tanker capacity, elevated crude and product trade flows, and shipping markets that continue to benefit from reshaped trade routes, especially as Russian oil and refined products are redirected and longer haul voyages support strong day rates. In addition, industry wide commentary has highlighted robust charter markets and disciplined fleet growth, giving investors a structural story to match the recent price action.

- Right now, International Seaways scores a 4 out of 6 on our valuation checks. You can explore this in more detail via our valuation score. Next we will unpack what different valuation approaches say about that number, before closing with a more practical way to think about what this stock may be worth.

Approach 1: International Seaways Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting its future cash flows and discounting them back to today using a required rate of return. For International Seaways, the model starts with last twelve month Free Cash Flow of about $143 Million and then projects how that cash flow might evolve over time.

Analysts directly forecast Free Cash Flow of roughly $277 Million in 2026, and Simply Wall St extrapolates beyond that, with projected annual FCF staying in a similar $250 Million to $285 Million range over the following decade. These future cash flows are then discounted to reflect risk and the time value of money, using a 2 Stage Free Cash Flow to Equity framework.

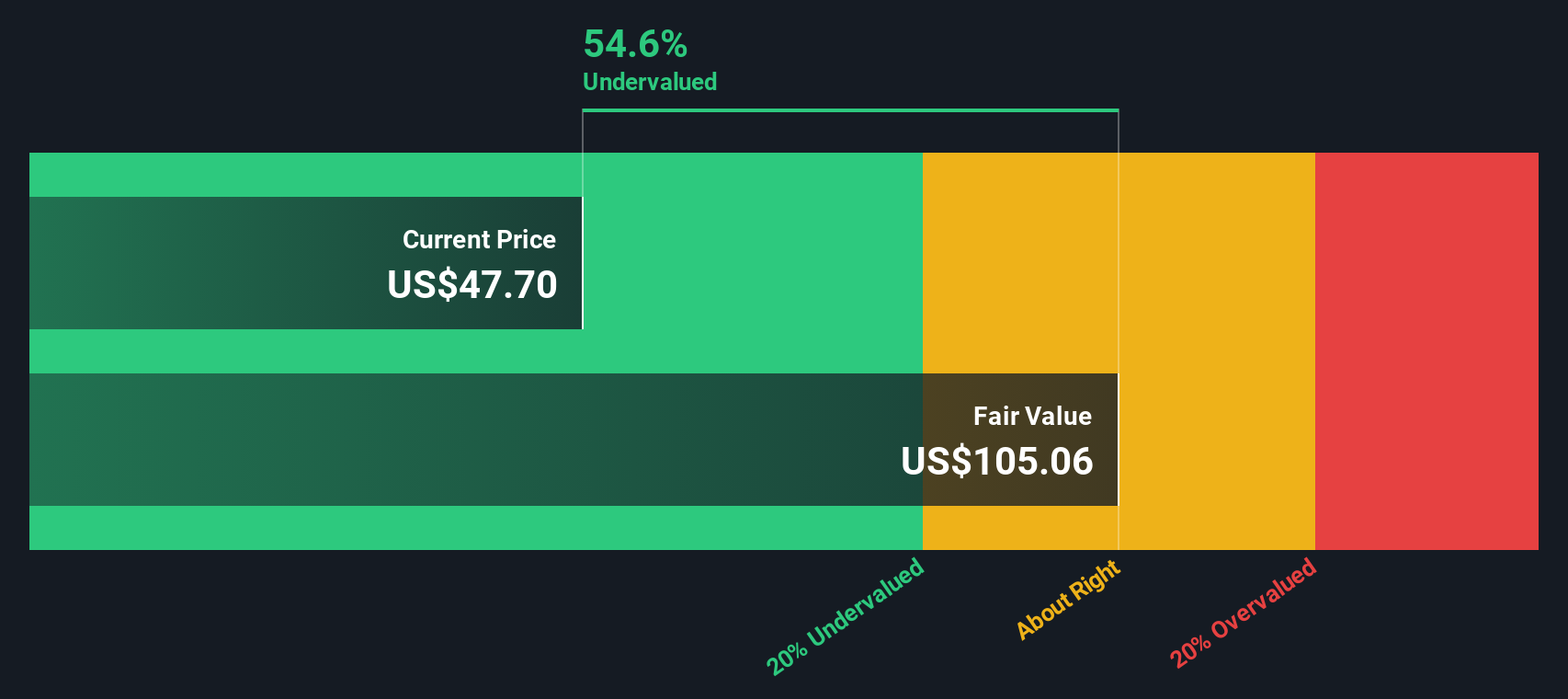

On this basis, the DCF model arrives at an estimated intrinsic value of about $120.19 per share. That implies the stock is trading at roughly a 59.6% discount to this estimated fair value, which indicates the market may be pricing in much weaker long term cash flows or higher risk than the model assumes.

Result: UNDERVALUED (based on this DCF model)

Our Discounted Cash Flow (DCF) analysis suggests International Seaways is undervalued by 59.6%. Track this in your watchlist or portfolio, or discover 908 more undervalued stocks based on cash flows.

Approach 2: International Seaways Price vs Earnings

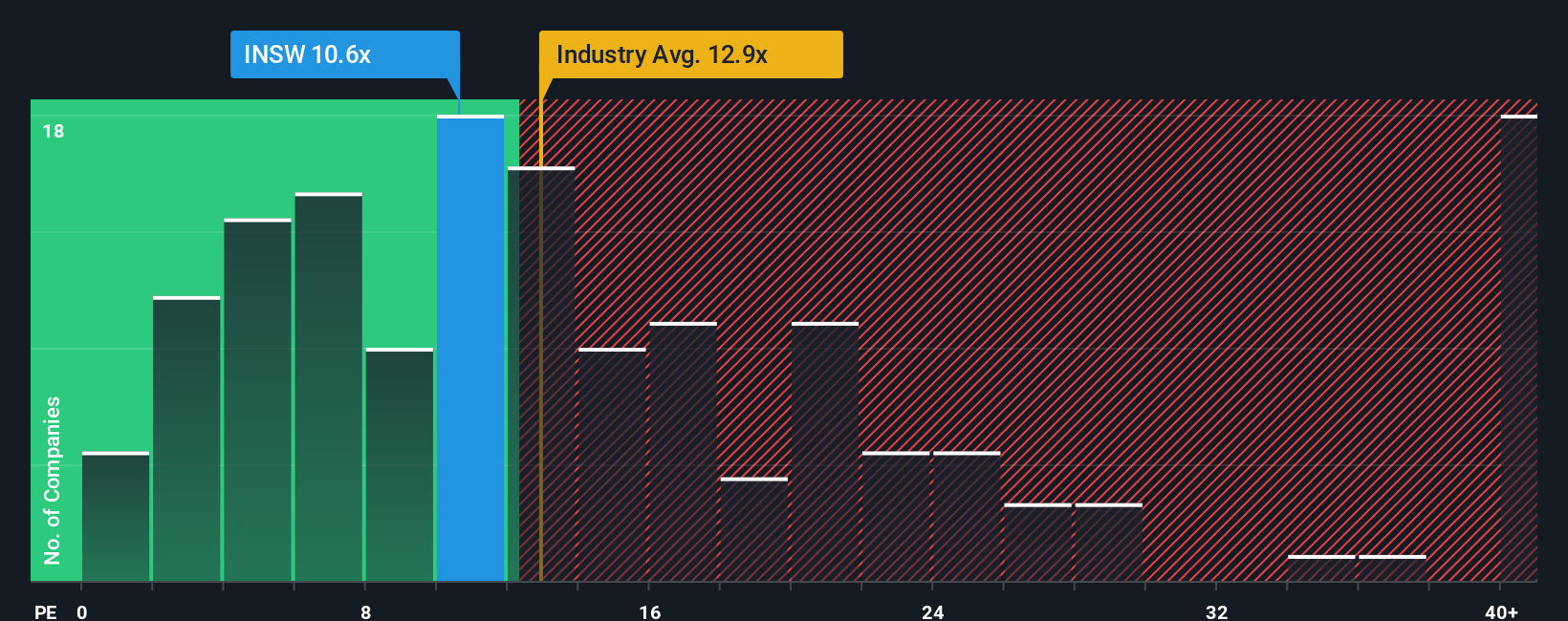

For profitable companies like International Seaways, the Price to Earnings (PE) ratio is a practical way to judge valuation because it links what investors pay today to the profits the business is generating right now. In broad terms, faster and more reliable earnings growth, as well as lower perceived risk, usually justify a higher PE ratio, while cyclical or riskier earnings tend to warrant a lower one.

International Seaways currently trades on a PE of about 11.0x. That is slightly above the tanker peer average of roughly 9.8x, but below the wider Oil and Gas industry average of around 13.3x. This comparison suggests the stock is not obviously expensive within its broader sector. To refine this view, Simply Wall St uses a proprietary Fair Ratio of 13.0x, which estimates the PE the company should trade on after adjusting for its earnings growth outlook, profitability, risk profile, industry positioning and market capitalization.

This Fair Ratio is more informative than a simple peer or industry comparison because it explicitly incorporates company specific fundamentals rather than assuming all firms deserve similar multiples. Since the Fair Ratio of 13.0x is higher than the current 11.0x, the PE based lens points to International Seaways being undervalued on earnings.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1445 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your International Seaways Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple framework on Simply Wall St's Community page where you connect your view of a company’s story to your own forecast for its future revenue, earnings and margins. This then links to a Fair Value that you can compare with today’s share price to help decide whether to buy, hold or sell. That Fair Value automatically updates as new news or earnings arrive so your view never goes stale. For International Seaways, for example, one investor might build a bullish narrative around tightening vessel supply, modern fleet upgrades and resilient dividend support that justifies a Fair Value closer to the high analyst target of about $64. Another may stress long term decarbonization risks, volatile spot exposure and regulatory costs and land nearer the low target around $47. Narratives makes these differing perspectives transparent, quantified and easy to track over time.

Do you think there's more to the story for International Seaways? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:INSW

International Seaways

Owns and operates a fleet of oceangoing vessels for the transportation of crude oil and petroleum products in the international flag trade.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)