With the business potentially at an important milestone, we thought we'd take a closer look at EQT Corporation's (NYSE:EQT) future prospects. EQT Corporation operates as a natural gas production company in the United States. The US$8.2b market-cap company posted a loss in its most recent financial year of US$967m and a latest trailing-twelve-month loss of US$2.9b leading to an even wider gap between loss and breakeven. Many investors are wondering about the rate at which EQT will turn a profit, with the big question being “when will the company breakeven?” Below we will provide a high-level summary of the industry analysts’ expectations for the company.

Check out our latest analysis for EQT

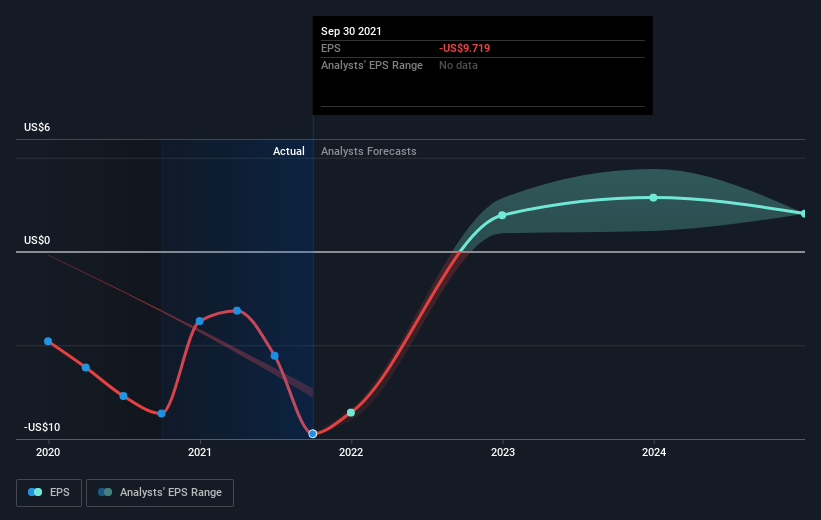

According to the 15 industry analysts covering EQT, the consensus is that breakeven is near. They expect the company to post a final loss in 2021, before turning a profit of US$757m in 2022. Therefore, the company is expected to breakeven roughly 12 months from now or less. How fast will the company have to grow to reach the consensus forecasts that anticipate breakeven by 2022? Working backwards from analyst estimates, it turns out that they expect the company to grow 56% year-on-year, on average, which is extremely buoyant. If this rate turns out to be too aggressive, the company may become profitable much later than analysts predict.

We're not going to go through company-specific developments for EQT given that this is a high-level summary, however, keep in mind that by and large an energy business has lumpy cash flows which are contingent on the natural resource and stage at which the company is operating. So, a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

One thing we would like to bring into light with EQT is its relatively high level of debt. Generally, the rule of thumb is debt shouldn’t exceed 40% of your equity, which in EQT's case is 75%. Note that a higher debt obligation increases the risk around investing in the loss-making company.

Next Steps:

This article is not intended to be a comprehensive analysis on EQT, so if you are interested in understanding the company at a deeper level, take a look at EQT's company page on Simply Wall St. We've also put together a list of relevant aspects you should further research:

- Valuation: What is EQT worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether EQT is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on EQT’s board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if EQT might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:EQT

EQT

Engages in the production, gathering, and transmission of natural gas.

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)