Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:CVI

Results: CVR Energy, Inc. Exceeded Expectations And The Consensus Lifted This Year's Outlook

CVR Energy, Inc. (NYSE:CVI) shareholders are probably feeling a little disappointed, since its shares fell 7.0% to US$25.48 in the week after its latest second-quarter results. It was overall a positive result, with revenues beating expectations by 9.5% to hit US$2.0b. CVR Energy also reported a statutory profit of US$0.21, which was a nice improvement from the loss that the analysts were predicting. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

View our latest analysis for CVR Energy

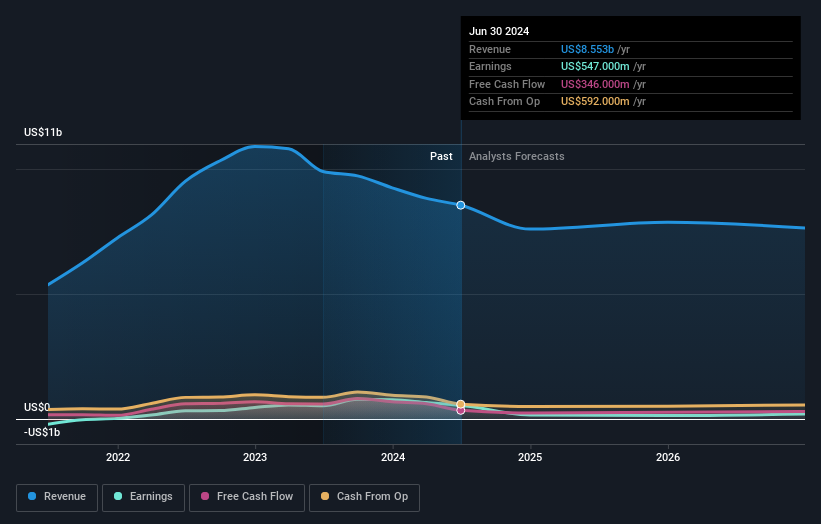

After the latest results, the consensus from CVR Energy's six analysts is for revenues of US$7.60b in 2024, which would reflect a definite 11% decline in revenue compared to the last year of performance. Statutory earnings per share are forecast to nosedive 70% to US$1.62 in the same period. In the lead-up to this report, the analysts had been modelling revenues of US$7.76b and earnings per share (EPS) of US$0.92 in 2024. While revenue forecasts have been revised downwards, the analysts look to have become more optimistic on the company's cost base, given the considerable lift to to the earnings per share numbers.

There's been no real change to the average price target of US$27.13, with the lower revenue and higher earnings forecasts not expected to meaningfully impact the company's valuation over a longer timeframe. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values CVR Energy at US$33.75 per share, while the most bearish prices it at US$25.00. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await CVR Energy shareholders.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. We would highlight that revenue is expected to reverse, with a forecast 21% annualised decline to the end of 2024. That is a notable change from historical growth of 14% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 2.5% annually for the foreseeable future. It's pretty clear that CVR Energy's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around CVR Energy's earnings potential next year. On the negative side, they also downgraded their revenue estimates, and forecasts imply they will perform worse than the wider industry. Still, earnings per share are more important to value creation for shareholders. The consensus price target held steady at US$27.13, with the latest estimates not enough to have an impact on their price targets.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for CVR Energy going out to 2026, and you can see them free on our platform here..

You should always think about risks though. Case in point, we've spotted 3 warning signs for CVR Energy you should be aware of, and 1 of them is a bit unpleasant.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CVI

CVR Energy

Engages in renewable fuels and petroleum refining and marketing, and nitrogen fertilizer manufacturing activities in the United States.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor