Advertisement

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, the ROCE of California Resources (NYSE:CRC) looks great, so lets see what the trend can tell us.

Return On Capital Employed (ROCE): What Is It?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for California Resources, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

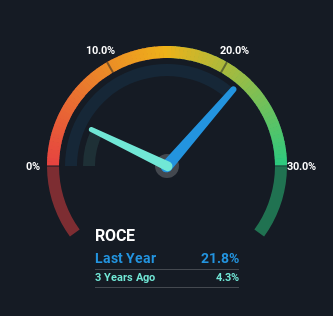

0.22 = US$711m ÷ (US$4.0b - US$694m) (Based on the trailing twelve months to September 2023).

So, California Resources has an ROCE of 22%. That's a fantastic return and not only that, it outpaces the average of 16% earned by companies in a similar industry.

See our latest analysis for California Resources

In the above chart we have measured California Resources' prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering California Resources here for free.

The Trend Of ROCE

We're pretty happy with how the ROCE has been trending at California Resources. We found that the returns on capital employed over the last five years have risen by 193%. The company is now earning US$0.2 per dollar of capital employed. Interestingly, the business may be becoming more efficient because it's applying 47% less capital than it was five years ago. A business that's shrinking its asset base like this isn't usually typical of a soon to be multi-bagger company.

Our Take On California Resources' ROCE

In summary, it's great to see that California Resources has been able to turn things around and earn higher returns on lower amounts of capital. And with the stock having performed exceptionally well over the last three years, these patterns are being accounted for by investors. Therefore, we think it would be worth your time to check if these trends are going to continue.

California Resources does have some risks, we noticed 3 warning signs (and 1 which can't be ignored) we think you should know about.

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:CRC

California Resources

Operates as an independent energy and carbon management company in the United States.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor