Advertisement

- United States

- /

- Oil and Gas

- /

- NasdaqGM:HPK

Earnings Update: HighPeak Energy, Inc. (NASDAQ:HPK) Just Reported And Analysts Are Trimming Their Forecasts

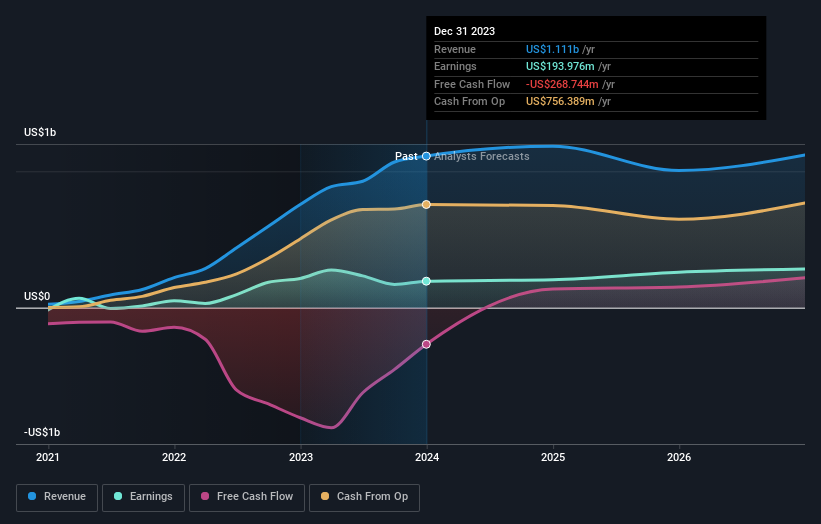

There's been a notable change in appetite for HighPeak Energy, Inc. (NASDAQ:HPK) shares in the week since its yearly report, with the stock down 13% to US$14.63. Revenues of US$1.1b were in line with forecasts, although statutory earnings per share (EPS) came in below expectations at US$1.58, missing estimates by 2.2%. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

Check out our latest analysis for HighPeak Energy

Taking into account the latest results, the most recent consensus for HighPeak Energy from three analysts is for revenues of US$1.18b in 2024. If met, it would imply a credible 6.6% increase on its revenue over the past 12 months. Per-share earnings are expected to accumulate 4.6% to US$1.58. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$1.30b and earnings per share (EPS) of US$2.21 in 2024. The analysts seem less optimistic after the recent results, reducing their revenue forecasts and making a large cut to earnings per share numbers.

Despite the cuts to forecast earnings, there was no real change to the US$22.50 price target, showing that the analysts don't think the changes have a meaningful impact on its intrinsic value. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on HighPeak Energy, with the most bullish analyst valuing it at US$31.50 and the most bearish at US$11.00 per share. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that HighPeak Energy's revenue growth is expected to slow, with the forecast 6.6% annualised growth rate until the end of 2024 being well below the historical 81% p.a. growth over the last three years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 1.8% per year. Even after the forecast slowdown in growth, it seems obvious that HighPeak Energy is also expected to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for HighPeak Energy. They also downgraded HighPeak Energy's revenue estimates, but industry data suggests that it is expected to grow faster than the wider industry. The consensus price target held steady at US$22.50, with the latest estimates not enough to have an impact on their price targets.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for HighPeak Energy going out to 2026, and you can see them free on our platform here..

You should always think about risks though. Case in point, we've spotted 4 warning signs for HighPeak Energy you should be aware of, and 2 of them are concerning.

Valuation is complex, but we're here to simplify it.

Discover if HighPeak Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:HPK

HighPeak Energy

Operates as an independent crude oil and natural gas exploration and production company.

Fair value second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.8% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|43.5% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|61.4% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor