- United States

- /

- Energy Services

- /

- NasdaqCM:DTI

Drilling Tools International Corporation's (NASDAQ:DTI) 27% Cheaper Price Remains In Tune With Revenues

The Drilling Tools International Corporation (NASDAQ:DTI) share price has fared very poorly over the last month, falling by a substantial 27%. The drop over the last 30 days has capped off a tough year for shareholders, with the share price down 26% in that time.

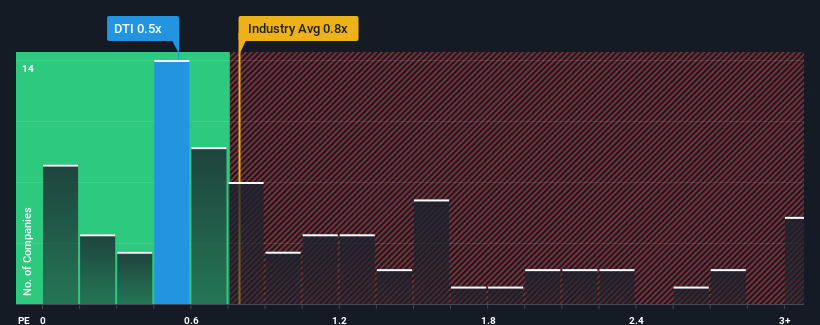

Even after such a large drop in price, it's still not a stretch to say that Drilling Tools International's price-to-sales (or "P/S") ratio of 0.5x right now seems quite "middle-of-the-road" compared to the Energy Services industry in the United States, where the median P/S ratio is around 0.8x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Check out our latest analysis for Drilling Tools International

How Has Drilling Tools International Performed Recently?

Drilling Tools International could be doing better as it's been growing revenue less than most other companies lately. It might be that many expect the uninspiring revenue performance to strengthen positively, which has kept the P/S ratio from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

Keen to find out how analysts think Drilling Tools International's future stacks up against the industry? In that case, our free report is a great place to start.Is There Some Revenue Growth Forecasted For Drilling Tools International?

The only time you'd be comfortable seeing a P/S like Drilling Tools International's is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered virtually the same number to the company's top line as the year before. Although pleasingly revenue has lifted 100% in aggregate from three years ago, notwithstanding the last 12 months. Therefore, it's fair to say the revenue growth recently has been great for the company, but investors will want to ask why it has slowed to such an extent.

Turning to the outlook, the next three years should generate growth of 6.0% each year as estimated by the three analysts watching the company. That's shaping up to be similar to the 4.7% each year growth forecast for the broader industry.

In light of this, it's understandable that Drilling Tools International's P/S sits in line with the majority of other companies. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Key Takeaway

With its share price dropping off a cliff, the P/S for Drilling Tools International looks to be in line with the rest of the Energy Services industry. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've seen that Drilling Tools International maintains an adequate P/S seeing as its revenue growth figures match the rest of the industry. Right now shareholders are comfortable with the P/S as they are quite confident future revenue won't throw up any surprises. If all things remain constant, the possibility of a drastic share price movement remains fairly remote.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 3 warning signs with Drilling Tools International, and understanding them should be part of your investment process.

If you're unsure about the strength of Drilling Tools International's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:DTI

Drilling Tools International

Provides oilfield equipment and services to oil and natural gas sectors in North America, Europe, and the Middle East.

Undervalued slight.

Similar Companies

Market Insights

Community Narratives