- United States

- /

- Oil and Gas

- /

- NasdaqGS:CHRD

If EPS Growth Is Important To You, Chord Energy (NASDAQ:CHRD) Presents An Opportunity

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Chord Energy (NASDAQ:CHRD). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Chord Energy with the means to add long-term value to shareholders.

View our latest analysis for Chord Energy

How Fast Is Chord Energy Growing Its Earnings Per Share?

Strong earnings per share (EPS) results are an indicator of a company achieving solid profits, which investors look upon favourably and so the share price tends to reflect great EPS performance. So for many budding investors, improving EPS is considered a good sign. It's an outstanding feat for Chord Energy to have grown EPS from US$12.86 to US$42.03 in just one year. While it's difficult to sustain growth at that level, it bodes well for the company's outlook for the future. Could this be a sign that the business has reached an inflection point?

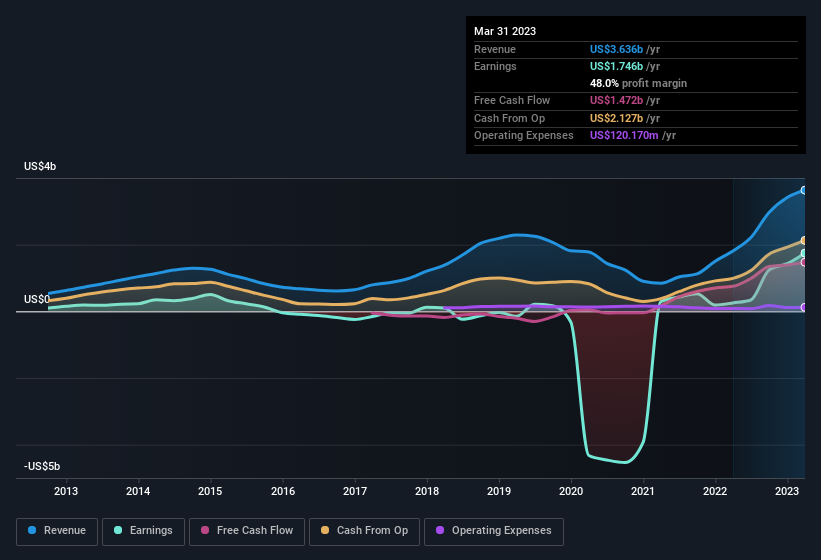

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. The good news is that Chord Energy is growing revenues, and EBIT margins improved by 53.9 percentage points to 54%, over the last year. Ticking those two boxes is a good sign of growth, in our book.

The chart below shows how the company's bottom and top lines have progressed over time. For finer detail, click on the image.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Chord Energy's forecast profits?

Are Chord Energy Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Chord Energy top brass are certainly in sync, not having sold any shares, over the last year. But the real excitement comes from the US$123k that Lead Independent Director Douglas Brooks spent buying shares (at an average price of about US$123). Purchases like this clue us in to the to the faith management has in the business' future.

Along with the insider buying, another encouraging sign for Chord Energy is that insiders, as a group, have a considerable shareholding. Indeed, they have a considerable amount of wealth invested in it, currently valued at US$201m. Investors will appreciate management having this amount of skin in the game as it shows their commitment to the company's future.

Shareholders have more to smile about than just insiders adding more shares to their already sizeable holdings. That's because on our analysis the CEO, Danny Brown, is paid less than the median for similar sized companies. The median total compensation for CEOs of companies similar in size to Chord Energy, with market caps between US$4.0b and US$12b, is around US$8.0m.

The CEO of Chord Energy only received US$1.9m in total compensation for the year ending December 2022. That's clearly well below average, so at a glance that arrangement seems generous to shareholders and points to a modest remuneration culture. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. It can also be a sign of good governance, more generally.

Is Chord Energy Worth Keeping An Eye On?

Chord Energy's earnings have taken off in quite an impressive fashion. To sweeten the deal, insiders have significant skin in the game with one even acquiring more. This quick rundown suggests that the business may be of good quality, and also at an inflection point, so maybe Chord Energy deserves timely attention. Even so, be aware that Chord Energy is showing 2 warning signs in our investment analysis , and 1 of those shouldn't be ignored...

The good news is that Chord Energy is not the only growth stock with insider buying. Here's a list of them... with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:CHRD

Chord Energy

Operates as an independent exploration and production company in the United States.

Undervalued with adequate balance sheet and pays a dividend.