- United States

- /

- Consumer Finance

- /

- NYSE:ALLY

Is It Too Late To Consider Ally After Its 106% Three Year Surge?

Reviewed by Bailey Pemberton

- Wondering if Ally Financial at around $44 a share is still a value play after its big run, or if most of the upside is already priced in, you are not alone.

- The stock has climbed 18.4% over the last month, 24.8% year to date, and an impressive 106.8% over three years, which naturally raises questions about how much of the future has been pulled forward.

- Recent headlines have focused on Ally sharpening its digital banking strategy and doubling down on auto and consumer lending, while also highlighting initiatives in deposits and credit risk management. Together, these themes help explain why investors have been re-rating the stock as a more resilient, tech enabled lender rather than just a cyclical auto finance name.

- Despite that optimism, Ally scores just 1/6 on our undervaluation checks. In this article, we will walk through what different valuation approaches are really saying about the stock, and then finish with a more intuitive way to think about fair value that many investors overlook.

Ally Financial scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Ally Financial Excess Returns Analysis

The Excess Returns model looks at how much profit Ally generates above the return that investors require on its equity, then capitalizes those excess profits into an intrinsic value per share.

For Ally, the starting point is a Book Value of $41.56 per share and a Stable EPS of $4.79 per share, based on weighted future Return on Equity estimates from 10 analysts. The average Return on Equity is 10.55%, while the Cost of Equity is estimated at $5.21 per share, leading to an Excess Return of $-0.42 per share. In other words, Ally is not expected to consistently earn more than its cost of capital on each dollar of equity.

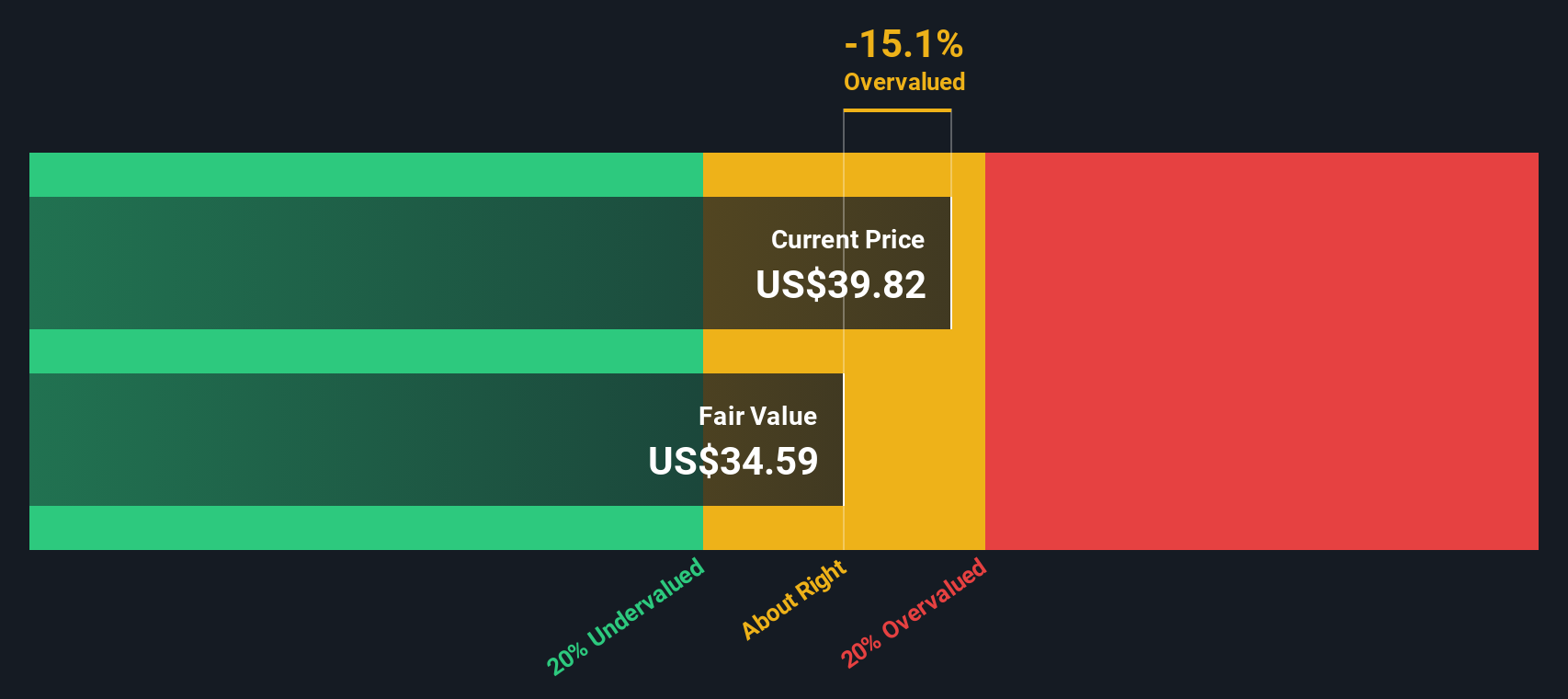

Analysts also see Stable Book Value edging up to $45.39 per share over time. However, because projected returns do not clear the required hurdle rate, the model produces an intrinsic value of about $40.27 per share. This implies the stock is roughly 10.8% overvalued versus the current price around $44.

Result: OVERVALUED

Our Excess Returns analysis suggests Ally Financial may be overvalued by 10.8%. Discover 911 undervalued stocks or create your own screener to find better value opportunities.

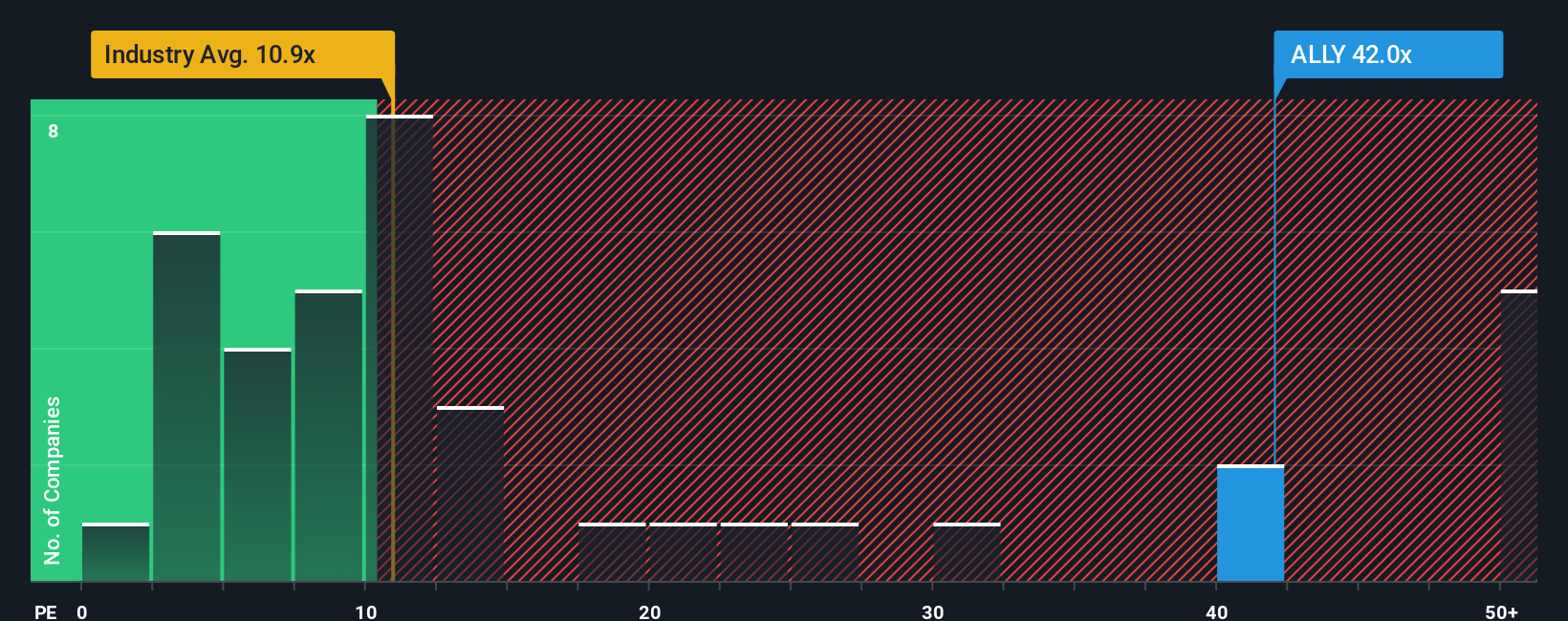

Approach 2: Ally Financial Price vs Earnings

For a profitable lender like Ally, the price to earnings ratio is a practical way to gauge what the market is willing to pay for each dollar of current earnings. It naturally reflects expectations for future growth and how risky investors perceive those earnings to be, so faster growth and lower risk usually justify a higher multiple, while slower growth or higher risk call for a lower one.

Ally currently trades on a PE of about 26.2x, which is well above the Consumer Finance industry average of roughly 9.7x and also ahead of its peer group average of around 45.8x. To go a step further, Simply Wall St calculates a Fair Ratio of 20.6x, which is the PE you might expect given Ally’s specific mix of earnings growth, margins, industry, market cap and risk profile.

This Fair Ratio is more informative than a simple industry or peer comparison because it is tailored to Ally’s fundamentals rather than assuming all consumer finance stocks deserve the same multiple. With the current PE sitting meaningfully above the Fair Ratio, the numbers point to the shares being somewhat expensive on an earnings basis.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1463 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Ally Financial Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework on Simply Wall St’s Community page where you connect your story about Ally Financial to a set of future revenue, earnings, and margin assumptions. You then link those to a forecast and fair value, and track in real time how your buy or sell decision changes as news or earnings arrive and as other investors’ views range from a cautious $39 per share outlook that bakes in slower growth and higher credit risk, to a more optimistic $59 view built on faster digital adoption, improving credit trends, and stronger long term profitability.

Do you think there's more to the story for Ally Financial? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ALLY

Ally Financial

A digital financial-services company, provides various digital financial products and services in the United States, Canada, and Bermuda.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)