Advertisement

- United States

- /

- Diversified Financial

- /

- NasdaqGM:PAYO

Payoneer (PAYO): Assessing Valuation Following Strategic Stripe Partnership for Asia Pacific Online Merchants

Simply Wall St

Reviewed by Simply Wall St

Payoneer Global (NASDAQ:PAYO) just announced a new partnership with Stripe, and it is already generating plenty of buzz among investors interested in fintech disruptors. This collaboration expands Payoneer’s Online Checkout platform, launching first in Asia Pacific markets like China and Hong Kong. The aim is simple and potentially game-changing for merchants: enable small and medium-sized businesses to offer a much wider array of payment methods, including Buy Now Pay Later services and digital wallets such as Apple Pay and Google Pay. For anyone keeping an eye on global ecommerce, this fits right in with Payoneer’s goal to make borderless digital selling simpler and more competitive.

This move builds on Payoneer’s recent string of service expansions, including last week’s launch of blockchain-enabled treasury transfers through Citi. It is the kind of momentum that gets talked about. Despite a share price that’s only nudged up 5% over the past month, long-term investors have experienced a flat return this year and a 10% gain over the last three years. While the core business is growing, especially outside the US, market enthusiasm has remained measured.

So after a year of muted returns and back-to-back partnership announcements, are we looking at a value opportunity that the market is missing, or is Payoneer’s growth story already priced in?

Most Popular Narrative: 28.6% Undervalued

According to community narrative, Payoneer Global is trading well below its calculated fair value. This points to strong market potential if projected growth materializes.

Strategic partnerships and integrations, notably the expansion with Stripe and Mastercard, are enhancing Payoneer's product offering. These developments are extending its checkout and card capabilities, and boosting customer engagement and transaction volumes. As a result, this should drive top-line revenue growth and repeat business over the long term.

Want to know what is powering that undervalued rating? One part is a set of fast-moving global trends, and the narrative suggests rising profit potential paired with a premium price target. Curious what mix of future earnings, growth, and profitability justifies such a bullish outlook? The underlying assumptions might surprise you.

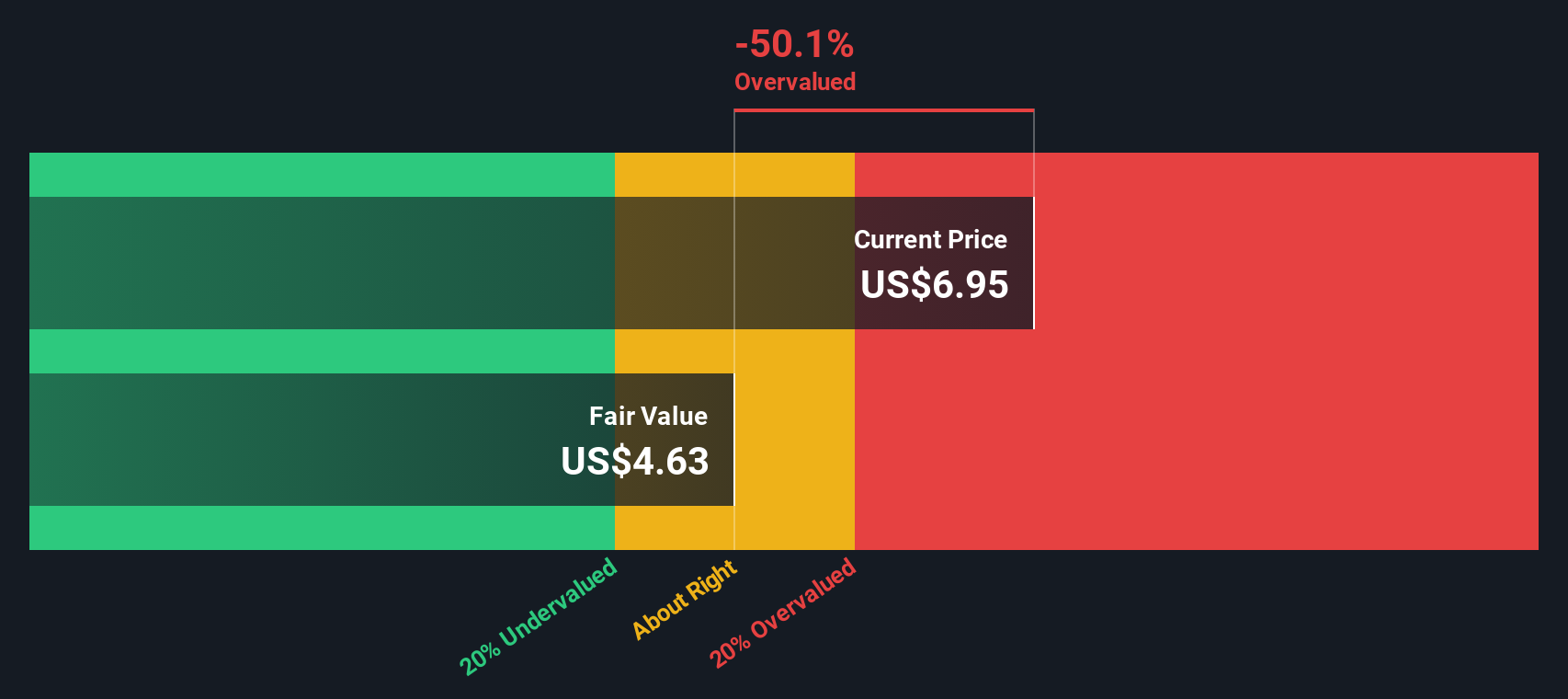

Result: Fair Value of $9.81 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, competition from emerging fintech rivals and Payoneer’s heavy reliance on large e-commerce partners could still challenge its growth and profit assumptions.

Find out about the key risks to this Payoneer Global narrative.Another View: SWS DCF Model Sees It Differently

While analysts expect Payoneer Global could climb based on future earnings, our DCF model presents a more cautious picture and suggests shares may actually be overvalued at today’s price. Will this pricing gap persist?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Payoneer Global for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Payoneer Global Narrative

If you see the story differently or want to dig into the numbers on your own terms, you can craft a personalized view quickly. All it takes is a few minutes to do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Payoneer Global.

Looking for more investment ideas?

Why limit yourself to just one opportunity? Get ahead of the curve by targeting themes and trends that are shaping the future. Don’t miss the chance to find companies primed for growth, hidden value, or transformation. This is your moment to act smarter than the crowd.

- Spot income potential as you check out dividend stocks with yields > 3% that combine robust yields with steady financials, offering a strong foundation for portfolio growth.

- Capture the upside in health innovation when you review healthcare AI stocks setting new standards in patient care with breakthroughs in artificial intelligence.

- Ride the momentum of AI-driven change by seeking out AI penny stocks positioned at the forefront of automation and next-generation software solutions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:PAYO

Flawless balance sheet with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Gaxos.ai: Early-Stage AI Innovator in Gaming & Health

Fair Value US$2.21|6.3% undervalued

JO

Community Contributor

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value US$500.00|0.9% overvalued

PI

Community Contributor

Amazon's Future Rises as Stock Price Falls: A Long-Term Investment Vision

Fair Value US$234.75|2.9% undervalued

ZW

Community Contributor