Advertisement

- United States

- /

- Diversified Financial

- /

- NasdaqGM:NMIH

The Bull Case for NMI Holdings (NMIH) Could Change Following Strong Q2 Earnings and Margin Growth

Simply Wall St

Reviewed by Simply Wall St

- NMI Holdings, Inc. recently announced its earnings for the second quarter and first half of 2025, reporting quarterly revenue of US$173.78 million and net income of US$96.15 million, both higher than the previous year.

- An important detail is that earnings per share, both basic and diluted, increased year-on-year, highlighting ongoing operational improvements and margin growth.

- We will explore how these stronger earnings and ongoing revenue growth impact NMI Holdings' investment outlook and long-term value drivers.

Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

NMI Holdings Investment Narrative Recap

For an investor to be a shareholder in NMI Holdings, the core belief centers on the continued growth of homeownership and the expansion of the mortgage insurance market, driven by demographic demand and NMI's focus on underwriting quality and operational efficiency. The latest earnings beat reinforces the company's operational strengths and margin improvements, but does not fundamentally change the main short-term catalyst, sustained housing market activity, nor does it materially reduce the primary risk: sensitivity to regional housing downturns and credit risk concentration.

Among recent developments, the company's ongoing share repurchase program stands out as directly relevant. The buyback activity, with over 700,000 shares repurchased for US$25.93 million in Q1 2025 and a total of over 4.3 million shares since August 2023, demonstrates management's capital discipline and supports per-share earnings growth, factors often considered alongside quarterly earnings momentum when assessing near-term value drivers.

Yet, in contrast to operational momentum, investors should be aware of the possible impact if geographic credit exposures become more pronounced in markets that are now showing...

Read the full narrative on NMI Holdings (it's free!)

NMI Holdings' outlook anticipates $812.2 million in revenue and $410.6 million in earnings by 2028. This scenario depends on 6.1% annual revenue growth and a $32.9 million earnings increase from the current $377.7 million.

Uncover how NMI Holdings' forecasts yield a $44.14 fair value, a 15% upside to its current price.

Exploring Other Perspectives

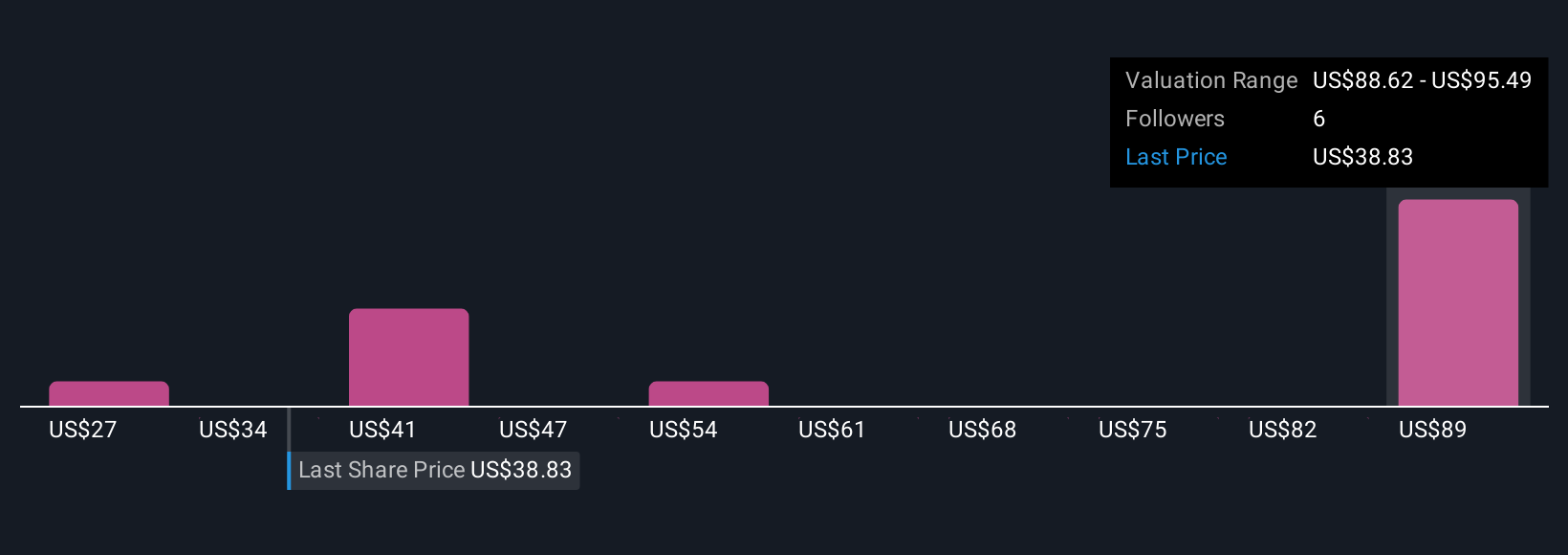

The Simply Wall St Community's fair value estimates for NMI Holdings range from US$26.80 to US$93.91 across four individual perspectives. While many focus on growth potential, recent results highlight how local housing weakness could still affect returns, so explore viewpoints that weigh these kinds of risks.

Explore 4 other fair value estimates on NMI Holdings - why the stock might be worth 30% less than the current price!

Build Your Own NMI Holdings Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your NMI Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free NMI Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate NMI Holdings' overall financial health at a glance.

Curious About Other Options?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 25 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if NMI Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:NMIH

NMI Holdings

Provides private mortgage guaranty insurance services in the United States.

Undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|28.9% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|27.0% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.9% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.5% undervalued

RO

Community Contributor