Advertisement

- United States

- /

- Consumer Finance

- /

- NasdaqGS:OMCC

Shareholders May Be More Conservative With Nicholas Financial, Inc.'s (NASDAQ:NICK) CEO Compensation For Now

Under the guidance of CEO Doug Marohn, Nicholas Financial, Inc. (NASDAQ:NICK) has performed reasonably well recently. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 02 September 2021. However, some shareholders will still be cautious of paying the CEO excessively.

See our latest analysis for Nicholas Financial

Comparing Nicholas Financial, Inc.'s CEO Compensation With the industry

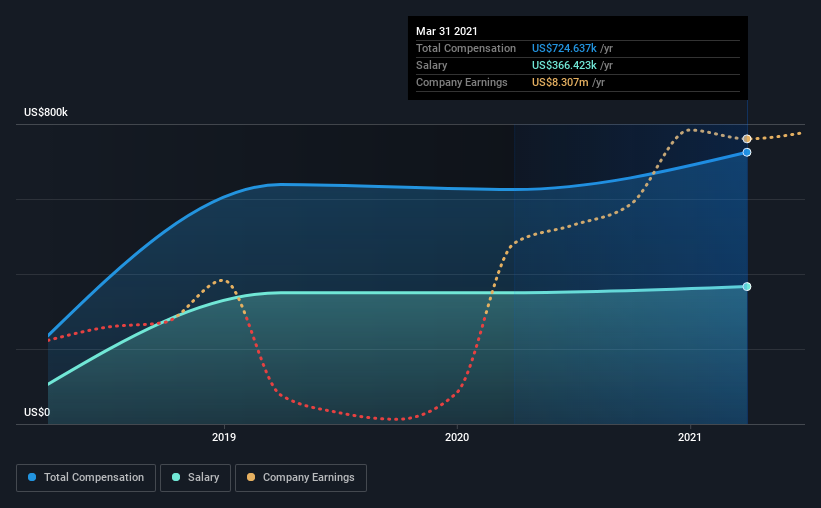

Our data indicates that Nicholas Financial, Inc. has a market capitalization of US$91m, and total annual CEO compensation was reported as US$725k for the year to March 2021. We note that's an increase of 16% above last year. In particular, the salary of US$366.4k, makes up a fairly large portion of the total compensation being paid to the CEO.

On comparing similar-sized companies in the industry with market capitalizations below US$200m, we found that the median total CEO compensation was US$60k. This suggests that Doug Marohn is paid more than the median for the industry. Moreover, Doug Marohn also holds US$1.0m worth of Nicholas Financial stock directly under their own name.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | US$366k | US$350k | 51% |

| Other | US$358k | US$275k | 49% |

| Total Compensation | US$725k | US$625k | 100% |

On an industry level, around 17% of total compensation represents salary and 83% is other remuneration. It's interesting to note that Nicholas Financial pays out a greater portion of remuneration through salary, compared to the industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

Nicholas Financial, Inc.'s Growth

Over the past three years, Nicholas Financial, Inc. has seen its earnings per share (EPS) grow by 89% per year. Its revenue is up 23% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. This sort of respectable year-on-year revenue growth is often seen at a healthy, growing business. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Nicholas Financial, Inc. Been A Good Investment?

Nicholas Financial, Inc. has generated a total shareholder return of 5.4% over three years, so most shareholders wouldn't be too disappointed. Although, there's always room to improve. In light of that, investors might probably want to see an improvement on their returns before they feel generous about increasing the CEO remuneration.

To Conclude...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. However, if the board proposes to increase the compensation, some shareholders might have questions given that the CEO is already being paid higher than the industry.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 3 warning signs for Nicholas Financial (2 don't sit too well with us!) that you should be aware of before investing here.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

If you’re looking to trade Nicholas Financial, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGS:OMCC

Old Market Capital

Provides broadband internet, voice over internet protocol, and video services in Northwest and Northcentral Ohio.

Excellent balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor