Advertisement

- United States

- /

- Consumer Finance

- /

- NasdaqGS:ECPG

Shareholders Will Most Likely Find Encore Capital Group, Inc.'s (NASDAQ:ECPG) CEO Compensation Acceptable

CEO Ashish Masih has done a decent job of delivering relatively good performance at Encore Capital Group, Inc. (NASDAQ:ECPG) recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 11 June 2021. We present our case of why we think CEO compensation looks fair.

See our latest analysis for Encore Capital Group

How Does Total Compensation For Ashish Masih Compare With Other Companies In The Industry?

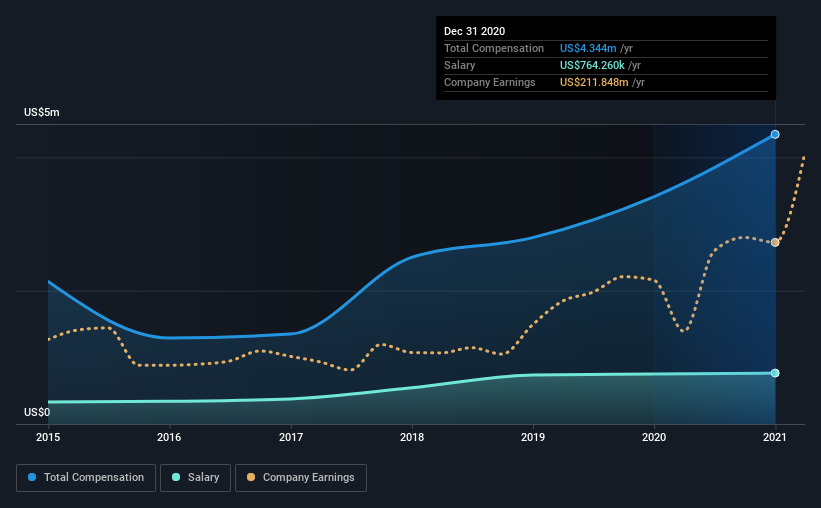

Our data indicates that Encore Capital Group, Inc. has a market capitalization of US$1.5b, and total annual CEO compensation was reported as US$4.3m for the year to December 2020. That's a notable increase of 27% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at US$764k.

For comparison, other companies in the same industry with market capitalizations ranging between US$1.0b and US$3.2b had a median total CEO compensation of US$5.9m. From this we gather that Ashish Masih is paid around the median for CEOs in the industry. Furthermore, Ashish Masih directly owns US$7.1m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | US$764k | US$750k | 18% |

| Other | US$3.6m | US$2.7m | 82% |

| Total Compensation | US$4.3m | US$3.4m | 100% |

Talking in terms of the industry, salary represented approximately 17% of total compensation out of all the companies we analyzed, while other remuneration made up 83% of the pie. Encore Capital Group is largely mirroring the industry average when it comes to the share a salary enjoys in overall compensation. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Encore Capital Group, Inc.'s Growth

Encore Capital Group, Inc.'s earnings per share (EPS) grew 47% per year over the last three years. Its revenue is up 21% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's a real positive to see this sort of revenue growth in a single year. That suggests a healthy and growing business. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Encore Capital Group, Inc. Been A Good Investment?

Encore Capital Group, Inc. has generated a total shareholder return of 22% over three years, so most shareholders would be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. In saying that, any proposed increase to CEO compensation will still be assessed on how reasonable it is based on performance and industry benchmarks.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. We did our research and identified 3 warning signs (and 2 which make us uncomfortable) in Encore Capital Group we think you should know about.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you decide to trade Encore Capital Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Encore Capital Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NasdaqGS:ECPG

Encore Capital Group

A specialty finance company, provides debt recovery solutions and other related services for consumers across financial assets worldwide.

Good value with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|33.8% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|26.3% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.2% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.6% undervalued

RO

Community Contributor