Advertisement

- United States

- /

- Hospitality

- /

- NYSE:YUM

Yum! Brands (YUM): Assessing Valuation After Bylaw Updates and New Taco Bell Brazil Growth Plans

Simply Wall St

Reviewed by Simply Wall St

Yum! Brands (YUM) has introduced a new set of amendments to its bylaws, concentrating on governance and shareholder meeting procedures. In addition, the company announced plans to accelerate Taco Bell’s growth in Brazil under direct management.

See our latest analysis for Yum! Brands.

These governance and operational shifts for Yum! Brands have come alongside notable gains, with a 14.7% year-to-date share price return and a robust 12.4% total shareholder return over the past year. This signals renewed confidence in the company’s trajectory. Recent dividend affirmations and growth plans for Taco Bell in Brazil suggest momentum is building as investors reassess both risk and long-term potential.

If management’s new growth strategy has sparked your interest, now is the perfect opportunity to broaden your perspective and discover fast growing stocks with high insider ownership

With Yum! Brands’ stock not far off analysts’ targets and recent gains reflecting renewed optimism, investors must weigh whether further upside remains. Is there still a buying opportunity, or is the market already anticipating future growth?

Most Popular Narrative: 7.5% Undervalued

With Yum! Brands closing at $153.21, the most widely followed narrative argues that the stock’s fair value stands higher, setting up a debate over whether the current price offers a true bargain. Over the past months, modest gains have reignited interest in Yum!’s growth story. The following perspective highlights one influential factor underpinning this view.

The rapid acceleration and global rollout of Yum!'s Byte digital platform, including AI-driven marketing, operational automation, and proprietary ordering and delivery solutions, positions the company to capture higher transaction volumes, expand check sizes, and enhance customer loyalty. This could drive both top-line revenue growth and improve net margins over the long term.

Curious what else shapes this high fair value? There is a bold forecast that hinges on surprising momentum in margins, digital expansion, and future profit multiples. Want the full script behind analysts’ pricing logic? Find out which bold assumptions drive the story when you read the entire narrative.

Result: Fair Value of $165.56 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, weaker Pizza Hut performance or rising operational costs could challenge current optimism and introduce volatility into Yum! Brands’ outlook in the near term.

Find out about the key risks to this Yum! Brands narrative.

Another View: Multiples Tell a Different Story

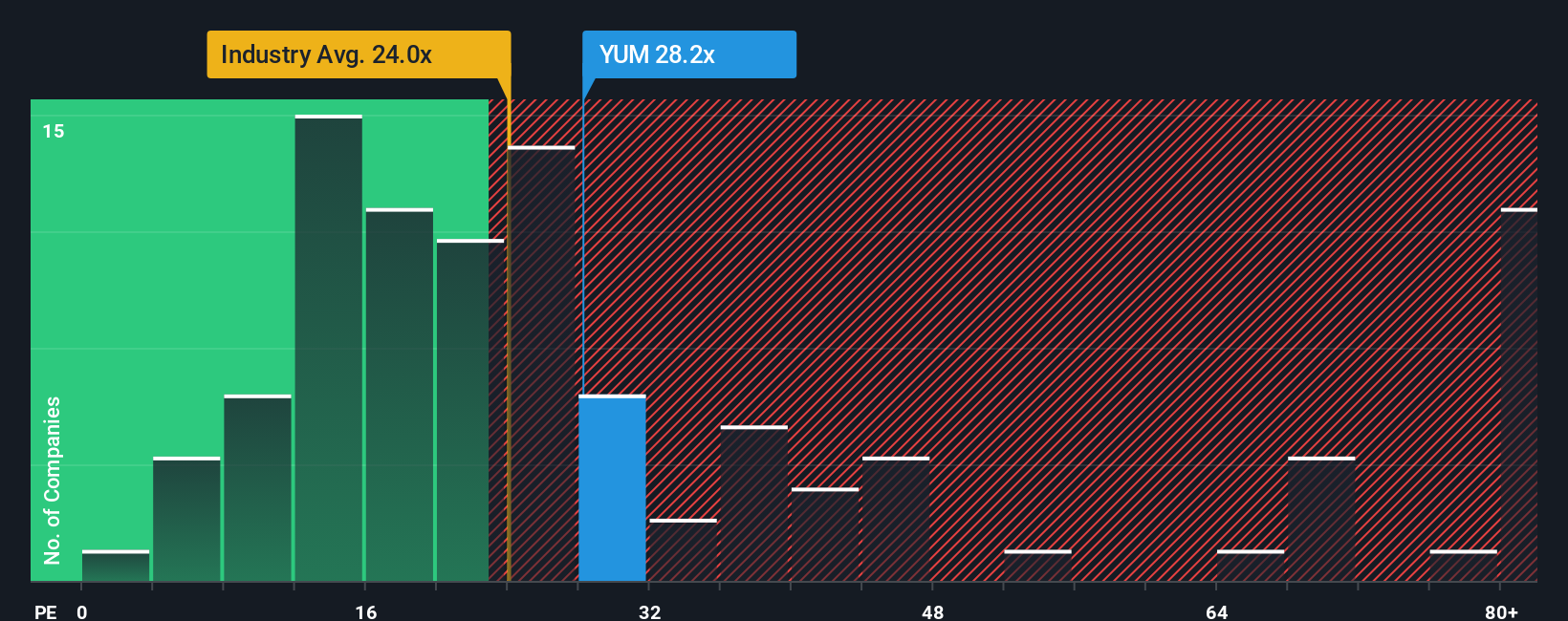

Looking at Yum! Brands through the lens of current price-to-earnings ratios offers a different conclusion than the high fair value narrative. The stock trades at 29.4 times earnings, which is higher than both its industry average (21.4x) and the fair ratio (26.3x) our models suggest. This gap could signal overvaluation compared to peers and raise cautions for those considering possible future upside. There is a question of whether market expectations are too optimistic or if earnings growth may justify the premium.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Yum! Brands Narrative

If you see things differently or want to dig deeper into the numbers yourself, you can easily build your own narrative in just a few minutes. Do it your way

A great starting point for your Yum! Brands research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Don’t let the best opportunities pass you by. The right screeners can spotlight game-changing trends, emerging growth, and high-yield income. Start your next search now.

- Uncover breakthrough healthcare companies shaping medicine’s future with these 30 healthcare AI stocks, featuring innovative stocks at the forefront of AI-powered diagnostics and treatment.

- Maximize potential returns by targeting strong cash flow with these 920 undervalued stocks based on cash flows, connecting you to undervalued stocks where the numbers support the upside.

- Capture consistent passive income streams by locking in attractive yields through these 15 dividend stocks with yields > 3%, highlighting companies built for resilient payouts above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:YUM

Yum! Brands

Develops, operates, and franchises quick service restaurants worldwide.

Average dividend payer with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

930 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative