Advertisement

- United States

- /

- Hospitality

- /

- NYSE:YUM

We Think Some Shareholders May Hesitate To Increase Yum! Brands, Inc.'s (NYSE:YUM) CEO Compensation

Key Insights

- Yum! Brands to hold its Annual General Meeting on 16th of May

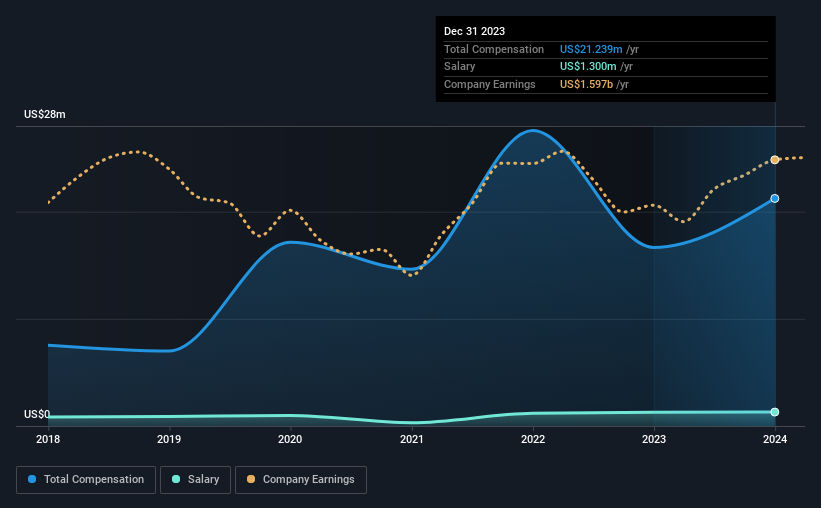

- CEO David Gibbs' total compensation includes salary of US$1.30m

- The total compensation is 38% higher than the average for the industry

- Yum! Brands' total shareholder return over the past three years was 23% while its EPS grew by 15% over the past three years

Performance at Yum! Brands, Inc. (NYSE:YUM) has been reasonably good and CEO David Gibbs has done a decent job of steering the company in the right direction. As shareholders go into the upcoming AGM on 16th of May, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

See our latest analysis for Yum! Brands

How Does Total Compensation For David Gibbs Compare With Other Companies In The Industry?

At the time of writing, our data shows that Yum! Brands, Inc. has a market capitalization of US$39b, and reported total annual CEO compensation of US$21m for the year to December 2023. That's a notable increase of 27% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at US$1.3m.

In comparison with other companies in the American Hospitality industry with market capitalizations over US$8.0b, the reported median total CEO compensation was US$15m. Accordingly, our analysis reveals that Yum! Brands, Inc. pays David Gibbs north of the industry median. What's more, David Gibbs holds US$33m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$1.3m | US$1.3m | 6% |

| Other | US$20m | US$15m | 94% |

| Total Compensation | US$21m | US$17m | 100% |

On an industry level, roughly 18% of total compensation represents salary and 82% is other remuneration. Yum! Brands pays a modest slice of remuneration through salary, as compared to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Yum! Brands, Inc.'s Growth

Over the past three years, Yum! Brands, Inc. has seen its earnings per share (EPS) grow by 15% per year. In the last year, its revenue is up 1.3%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's nice to see revenue heading northwards, as this is consistent with healthy business conditions. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Yum! Brands, Inc. Been A Good Investment?

With a total shareholder return of 23% over three years, Yum! Brands, Inc. shareholders would, in general, be reasonably content. But they probably wouldn't be so happy as to think the CEO should be paid more than is normal, for companies around this size.

To Conclude...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

CEO pay is simply one of the many factors that need to be considered while examining business performance. In our study, we found 3 warning signs for Yum! Brands you should be aware of, and 2 of them shouldn't be ignored.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:YUM

Yum! Brands

Develops, operates, and franchises quick service restaurants worldwide.

Average dividend payer slight.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|34.2% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|19.8% undervalued

MI

Community Contributor