Advertisement

- United States

- /

- Hospitality

- /

- NYSE:SIX

Six Flags Entertainment Corporation (NYSE:SIX) Analysts Are More Bearish Than They Used To Be

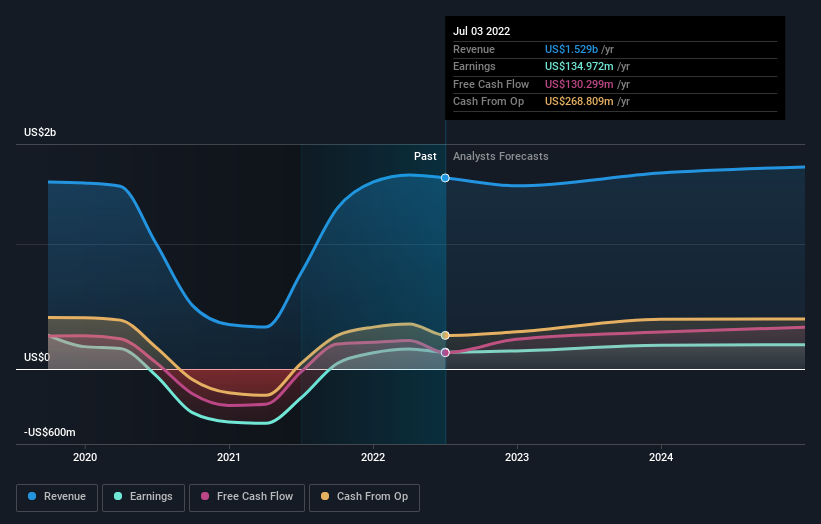

One thing we could say about the analysts on Six Flags Entertainment Corporation (NYSE:SIX) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon. At US$25.97, shares are up 6.4% in the past 7 days. It will be interesting to see if this downgrade motivates investors to start selling their holdings.

Following the latest downgrade, the current consensus, from the 13 analysts covering Six Flags Entertainment, is for revenues of US$1.5b in 2022, which would reflect a small 4.1% reduction in Six Flags Entertainment's sales over the past 12 months. Statutory earnings per share are presumed to rise 9.8% to US$1.78. Before this latest update, the analysts had been forecasting revenues of US$1.6b and earnings per share (EPS) of US$2.59 in 2022. Indeed, we can see that the analysts are a lot more bearish about Six Flags Entertainment's prospects, administering a substantial drop in revenue estimates and slashing their EPS estimates to boot.

See our latest analysis for Six Flags Entertainment

It'll come as no surprise then, to learn that the analysts have cut their price target 26% to US$31.27. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Six Flags Entertainment at US$46.00 per share, while the most bearish prices it at US$20.00. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. One more thing stood out to us about these estimates, and it's the idea that Six Flags Entertainment's decline is expected to accelerate, with revenues forecast to fall at an annualised rate of 8.0% to the end of 2022. This tops off a historical decline of 5.6% a year over the past five years. Compare this against analyst estimates for companies in the broader industry, which suggest that revenues (in aggregate) are expected to grow 13% annually. So it's pretty clear that, while it does have declining revenues, the analysts also expect Six Flags Entertainment to suffer worse than the wider industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for Six Flags Entertainment. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. Given the scope of the downgrades, it would not be a surprise to see the market become more wary of the business.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple Six Flags Entertainment analysts - going out to 2024, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:SIX

Six Flags Entertainment

Owns and operates regional theme and waterparks under the Six Flags name.

Moderate growth potential and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.9% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|21.3% undervalued

TI

Community Contributor