- United States

- /

- Hospitality

- /

- NYSE:NCLH

Norwegian Cruise Line Holdings Ltd.'s (NYSE:NCLH) Shares Climb 34% But Its Business Is Yet to Catch Up

Norwegian Cruise Line Holdings Ltd. (NYSE:NCLH) shares have had a really impressive month, gaining 34% after a shaky period beforehand. The last 30 days bring the annual gain to a very sharp 62%.

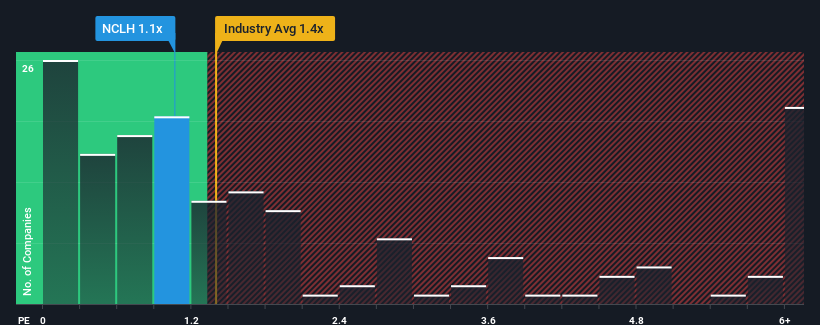

Although its price has surged higher, there still wouldn't be many who think Norwegian Cruise Line Holdings' price-to-sales (or "P/S") ratio of 1.1x is worth a mention when the median P/S in the United States' Hospitality industry is similar at about 1.4x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

View our latest analysis for Norwegian Cruise Line Holdings

How Has Norwegian Cruise Line Holdings Performed Recently?

Norwegian Cruise Line Holdings certainly has been doing a good job lately as it's been growing revenue more than most other companies. One possibility is that the P/S ratio is moderate because investors think this strong revenue performance might be about to tail off. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

Keen to find out how analysts think Norwegian Cruise Line Holdings' future stacks up against the industry? In that case, our free report is a great place to start.How Is Norwegian Cruise Line Holdings' Revenue Growth Trending?

Norwegian Cruise Line Holdings' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Retrospectively, the last year delivered an exceptional 77% gain to the company's top line. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, thanks in part to the last 12 months of revenue growth. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 8.6% per annum as estimated by the analysts watching the company. That's shaping up to be materially lower than the 11% per year growth forecast for the broader industry.

With this in mind, we find it intriguing that Norwegian Cruise Line Holdings' P/S is closely matching its industry peers. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Key Takeaway

Its shares have lifted substantially and now Norwegian Cruise Line Holdings' P/S is back within range of the industry median. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

When you consider that Norwegian Cruise Line Holdings' revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Having said that, be aware Norwegian Cruise Line Holdings is showing 1 warning sign in our investment analysis, you should know about.

If these risks are making you reconsider your opinion on Norwegian Cruise Line Holdings, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Norwegian Cruise Line Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:NCLH

Norwegian Cruise Line Holdings

Operates as a cruise company in North America, Europe, the Asia-Pacific, and internationally.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Community Narratives